RARE LN

WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF - USD Acc

Published 3 November 2025

China and the United States (US) are trading punch for punch on tariffs, yet the upper hand sits where supply chains are most concentrated. In rare earths, China’s grip on processing and magnet production gives Beijing leverage that carries straight into the negotiating room. Markets have noticed. Mining equities tied to strategic metals and rare earths increasingly trade as policy insurance, reflecting a deliberate rewiring of supply routes as governments seek resilience and bargaining power.

Beijing has set out a two-year pattern of rolling restrictions. It began with licensing for gallium and germanium in August 2023, then extended to graphite. Controls on antimony were added in September 20241. The list widened again in early 2025 to include tungsten, indium, bismuth, tellurium and molybdenum followed by new curbs in April on several rare earths, including key heavy elements used to harden magnets at elevated temperatures.

In the latest turn of events, Beijing has signalled a further tightening of rare earth export licensing, a move calibrated to the tariff negotiations rather than market fundamentals. The message is clear: China is prepared to use downstream choke points in separation, alloys and magnets to influence the trade agenda, keeping Western manufacturers on the back foot.

Announcement date | Elements newly covered | Count |

|---|---|---|

Aug-23 | Gallium; Germanium | 2 |

Oct-23 | Graphite | 1 |

Sep-24 | Antimony | 1 |

Feb-25 | Tungsten; Indium; Bismuth; Tellurium; Molybdenum | 5 |

Apr-25 | Samarium; Scandium; Dysprosium; Terbium; Gadolinium; Lutetium; Yttrium | 7 |

Dec-25 | Holmium; Erbium; Thulium; Europium; Ytterbium | 5 |

Source: Chinese Ministry of Commerce, Chinese Customs data as of 22 October 2025. Historical performance is not an indication of future performance and any investments may go down in value.

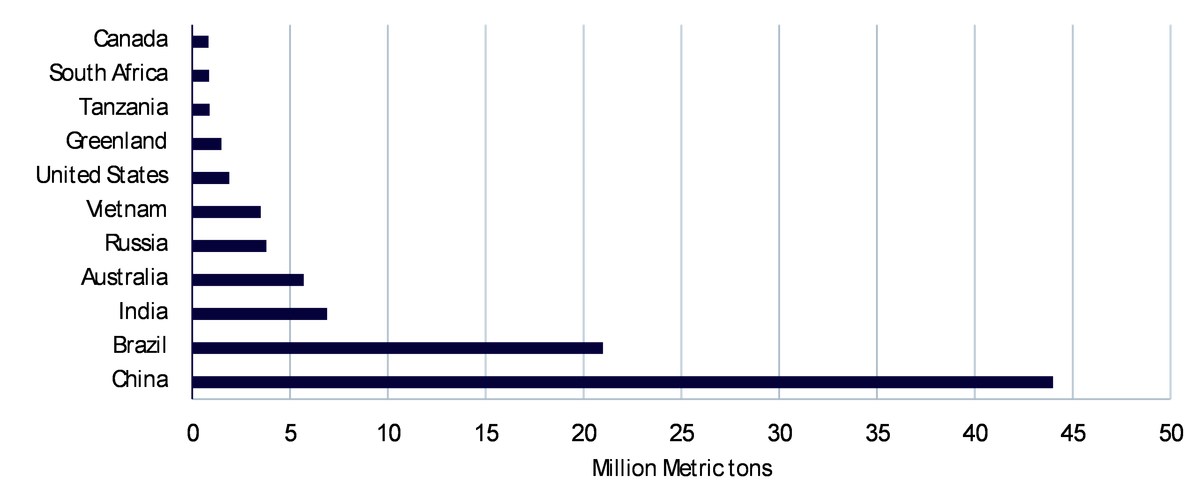

Heavy rare earths are the bottleneck

It is often said that rare earths are not rare. That is only half correct. Light rare earths such as neodymium are found in many geologies around the world. Heavy rare earths are not. Large-scale mining is currently concentrated in China and Myanmar, with processing primarily taking place in China. That makes the temperature-resilience additives in high-end motors the true chokepoint. Even with new allied projects coming, it will remain difficult for several years to source high-performance magnets that are fully independent of Chinese heavy rare earths.

Figure 2: Global rare earth reserves

Source: US Geological Survey as of January 2025. Note: Data for Myanmar, Madagascar, Malaysia and Nigeria are not available. Historical performance is not an indication of future performance and any investments may go down in value.

A policy pivot in Washington and Canberra

The latest US-Australia pact is designed to accelerate an allied alternative. President Donald Trump and Prime Minister Anthony Albanese have agreed to co-invest in a pipeline of Australian mines and processing projects with direct relevance to electric vehicles, semiconductors and defence2. Canberra has signalled about US$8.5bn of projects that are ready to move.

The Department of Defense (DoD) will help fund a 100-ton per year gallium refinery in Western Australia. The US Export-Import Bank has issued preliminary letters of interest for more than US$2.2bn tied to critical mineral developments3. In parallel, the DoD is exploring equity-style participation and multi-year contracts with floor price features across projects in the US, Canada and Australia as discussed here.

Australia’s role just grew

Australia holds the world’s fourth-largest reserves of rare earths and is already home to the only scaled, non-Chinese producer of separated rare earths. The new pact codifies what the market has anticipated for months. Australian producers are strategic partners in a long campaign to diversify away from Chinese midstream. The near-term focus is not only ore. It is separation circuits, heavy rare earth capability and magnet-adjacent metals such as gallium and tungsten. For capital markets, that means a clearer project pipeline, stronger financing signals and tighter alignment with allied industrial policy. The package includes a letter of interest from the US Export-Import Bank exceeding US$2.2 billion and Pentagon support for a 100-ton-per-year gallium refinery in Western Australia.

Capturing the supply chain rebuild with WisdomTree

For investors, these developments change the role that rare earths and strategic metals can play. The sector isn’t simply a cyclical bet on global growth. It is a structural allocation to supply security, industrial policy and technological adoption. Electric vehicles, industrial automation, air conditioning, robotics, and offshore wind all contribute to magnet demand, while data centres and grid build–out increase the call for strategic metals and rare earths.

A focused gateway to strategic metals

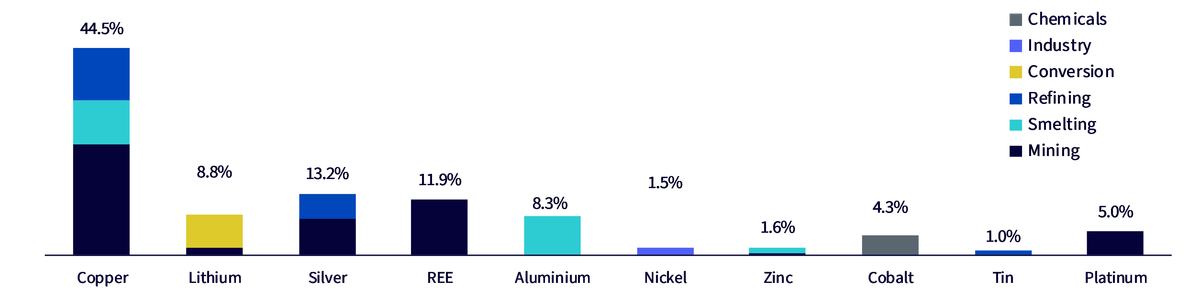

The WisdomTree Strategic Metals and Rare Earths Miners UCITS exchange-traded fund (ETF) (Ticker: RARE) is poised to benefit from the global resource realignment. The strategy is aligned with where bottlenecks and policy support are migrating. The WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF (Ticker: RARE) seeks to track the price and yield performance of the WisdomTree Energy Transition Metals and Rare Earth Miners Index (Ticker: WTMRAREN).

WTMRAREN is designed to identify globally listed companies from developed and emerging markets involved in the Energy Transition Metals Value Chain (ETMVC). Companies are mapped into 10 metal categories - aluminium, cobalt, copper, lithium, nickel, platinum, silver, tin, zinc and rare earth elements (REE). These are across six mining subsectors, such as mining, refining, smelting, chemicals, conversions and industry.

Figure 3: Weight of stocks across critical minerals and rare earths spectrum

Source: FactSet, WisdomTree as of 30 September 2025. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

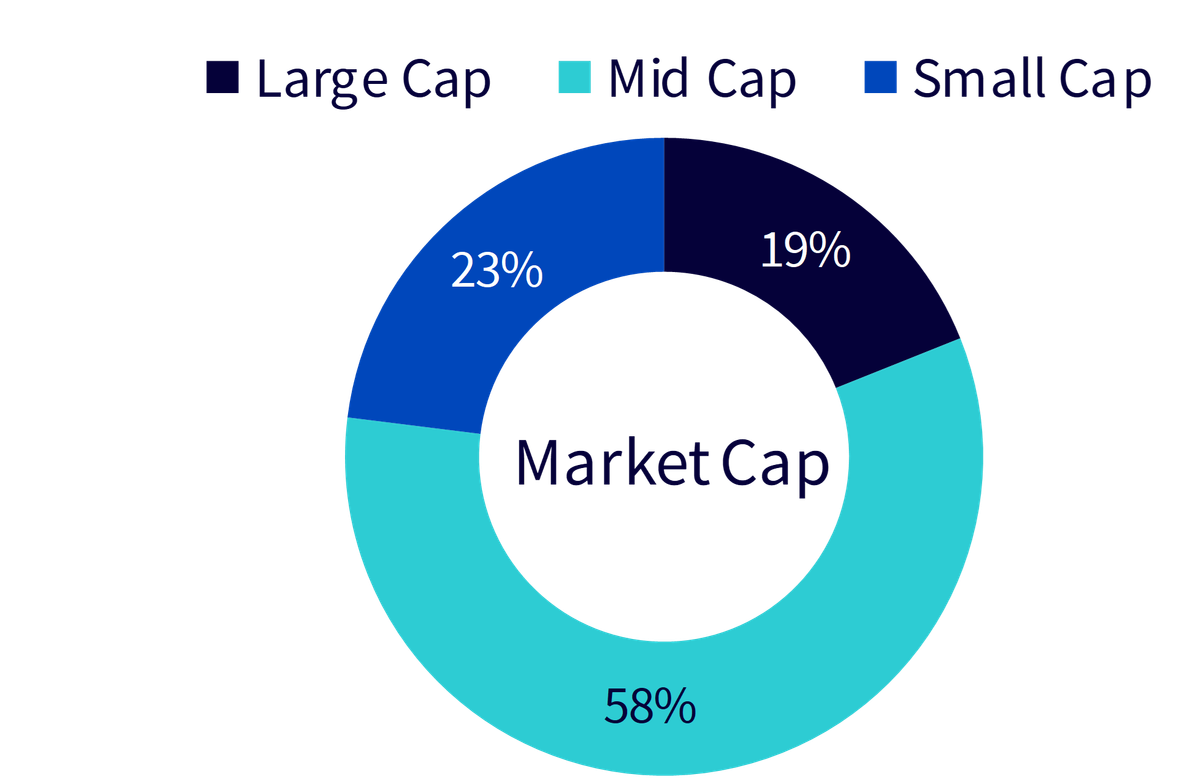

While China drives a significant share, the rest of the world, particularly the US, Australia, Canada, Europe, and select emerging markets, is accelerating REE development through projects and policy support. RARE’s global diversification ensures investors benefit from this broadened growth narrative. The WisdomTree Energy Transition Metals and Rare Earth Miners Index (Ticker: WTMRAREN) is fairly diversified across size, with its highest allocation at 58% in mid caps, 23% in small caps and 19 % in large caps4.

Figure 4: Geographical revenue breakdown – across developed and emerging markets

Source: WisdomTree, Wood Mackenzie. As of 30 September 2025. Small caps are companies with market value below or equal to 2B USD. Mid caps are companies with market value from 2B USD and up to 10B USD. Large caps are companies with market value above 10B USD. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

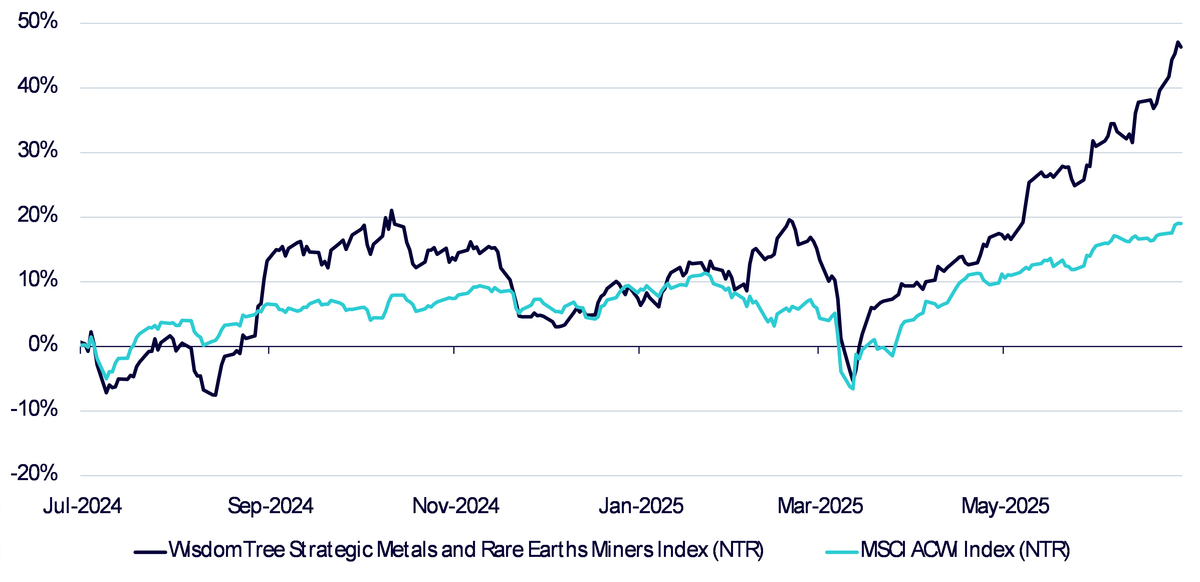

Valuation and performance edge

Notably, year-to-date (YTD), the WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF (+83.6%) has outperformed the MSCI All Country World Index (19.7%) by over 63.8%5, highlighting the strength of the theme amid shifting macroeconomic and political currents.

Figure 5: Comparison of performance over 1 year

Source: WisdomTree, Bloomberg. As of 24 October 2025. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

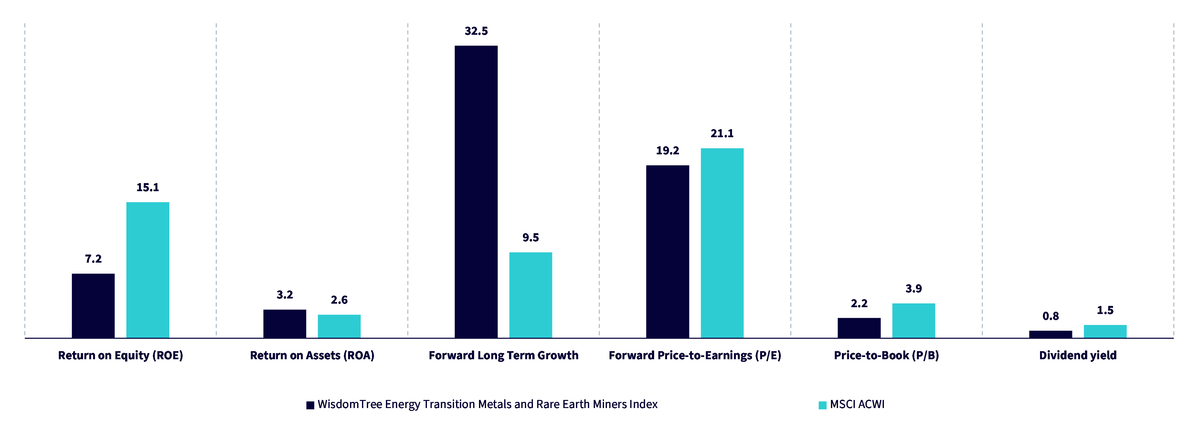

The WisdomTree Energy Transition Metals and Rare Earth Miners Index currently trades at a lower price to earnings (P/E) ratio of 19.2x, a price-to-book (P/B) ratio of 2.2x and a higher forward growth multiple of 32.5% than the MSCI All Country World Index, reflecting both relative value and earnings momentum. In addition, quality metrics such as Return on Assets (ROA) at 3.2% are also higher than the benchmark at 2.6%.

Figure 6: comparison of fundamental valuation

Source: WisdomTree, FactSet, Bloomberg. As of 30 September 2025. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Conclusion

Rare earths have transitioned from industrial inputs to strategic instruments. China’s downstream dominance means export policy can shape negotiation as surely as tariff schedules. The allied response is funded and focused on separation, heavy rare earth capability and magnets. For investors, this is a structural theme with clear policy sponsorship and a visible project pipeline. RARE provides diversified access to companies building the alternative supply chain while balancing single metal and single jurisdiction risk.

1Centre for Strategic and International Studies as of 20 August 2024

2The White House as of 20 October 2025

3Global Trade Review as of 22 October 2025

4WisdomTree, FactSet, Bloomberg as of 30 June 2025

5Bloomberg from 31 December 2024 to 17 July 2025

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.