WENU LN

WisdomTree Strategic Metals UCITS ETF - USD Acc

Published 26 February 2026

For decades, energy security meant oil and gas. Oil shocks reshaped foreign policy. The Organization of the Petroleum Exporting Countries (OPEC) influenced global power balances. Gas pipelines defined diplomatic relationships. Control of hydrocarbons meant geopolitical leverage.

That framework is evolving.

The global shift towards electrification, including electric vehicles (EVs), renewable power generation, battery storage, grid expansion and digital infrastructure, is not reducing energy dependency. It is changing the nature of that dependency.

We are moving from a hydrocarbon-based system to a materials-intensive one and the strategic question is no longer simply: Who controls oil?

It is increasingly: Who controls the inputs into the new energy system?

Electrification requires significantly more metals than fossil fuel systems:

The term ‘energy transition’ is better described as an ‘energy addition.’ Legacy systems remain, while electrified systems are layered on top, increasing total materials demand.

Certain metals are therefore no longer just industrial inputs. They are becoming strategic assets.

Strategic metals tend to share three characteristics:

Production is often concentrated in a few jurisdictions:

Concentration increases exposure to geopolitical and regulatory risk.

Mining diversification does not guarantee refining diversification. China dominates midstream processing across many battery materials and rare earth elements. Processing control often translates into pricing power.

New supply takes years to develop due to permitting, environmental scrutiny and capital intensity. In the short to medium term, supply is relatively inelastic.

Energy security is therefore increasingly about critical material supply chain security, measured in tonnes per year rather than barrels per day.

That recognition is beginning to shape policy.

Strategic reserves were historically associated with oil. The US Strategic Petroleum Reserve (SPR) was established after the 1970s oil shocks to buffer against supply disruptions. Today, major economies are applying similar logic to metals.

Across the United States, China and the European Union (EU), policymakers are either implementing or exploring strategic reserves of critical materials. This represents a structural shift: governments are becoming active participants in metal markets for security purposes.

The United States has launched a critical minerals initiative, often referred to as Project Vault, with approximately $12 billion in financing.

The objective is to build strategic inventories of materials essential to EVs, defence systems, semiconductor manufacturing and grid infrastructure.

The programme blends public financing with private participation, enabling companies to secure access to materials under predefined terms.

The strategic goals are clear:

This marks a move toward more direct state involvement in materials security.

China has long maintained strategic commodity reserves and has signalled expanded stockpiling of industrial metals, including copper.

As the world’s largest consumer of many base and battery metals, China’s stockpile decisions can materially influence global balances.

Strategic inventories allow China to:

While the US approach is primarily defensive, China’s strategy also supports the consolidation of industrial advantage.

The EU is further along in implementation but is increasingly focused on coordinated stockpiling under the Critical Raw Materials Act.

Policy discussions include:

Given Europe’s reliance on imports for many critical materials, stockpiling is seen as part of a broader push toward strategic autonomy.

Strategic stockpiling is most impactful when supply and demand are already balanced.

Several metals central to electrification are either in deficit or moving toward it.

When governments enter these markets as incremental buyers, the effects can be nonlinear.

Copper underpins grid expansion, renewable generation, EVs and data centres, placing it at the centre of the global electrification build-out. Yet supply growth has struggled to keep pace with rising demand, constrained by declining ore grades, lengthy permitting timelines and years of underinvestment, while visible inventories remain low relative to consumption. With limited short-term supply elasticity and new mines taking years to develop, additional demand impulses such as stockpiling can tighten a market already flirting with a structural deficit.

Silver demand from photovoltaics and electronics continues to expand, reinforcing its role in energy transition and advanced technology supply chains. At the same time, mine supply growth remains constrained and is often dependent on by-product production, limiting its responsiveness to rising demand. As a result, recurring supply-demand deficits have emerged in recent years, meaning that even incremental stockpiling could tighten available float relatively quickly.

Platinum is already in structural deficit. Supply constraints in South Africa and resilient demand from autocatalysts and hydrogen-related applications have drawn down inventories.

Platinum markets are relatively small in absolute terms, meaning even modest stockpiling volumes could have an outsized effect.

Aluminium production is highly energy-intensive. Energy volatility and decarbonisation pressures have constrained capacity growth in parts of Europe.

Many forecasts suggest aluminium could move into deficit later this decade, potentially around 2028.

However, aggressive stockpiling could pull forward that timeline by removing material from the tradable system before new supply is commissioned. Markets price marginal shifts, not base-case projections.

Strategic stockpiles do not consume metal, but they reduce liquidity.

Commodity prices are set at the margin. When inventories fall relative to consumption:

Stockpiling introduces a new class of buyer motivated by security rather than price. In tight markets, this can amplify scarcity dynamics.

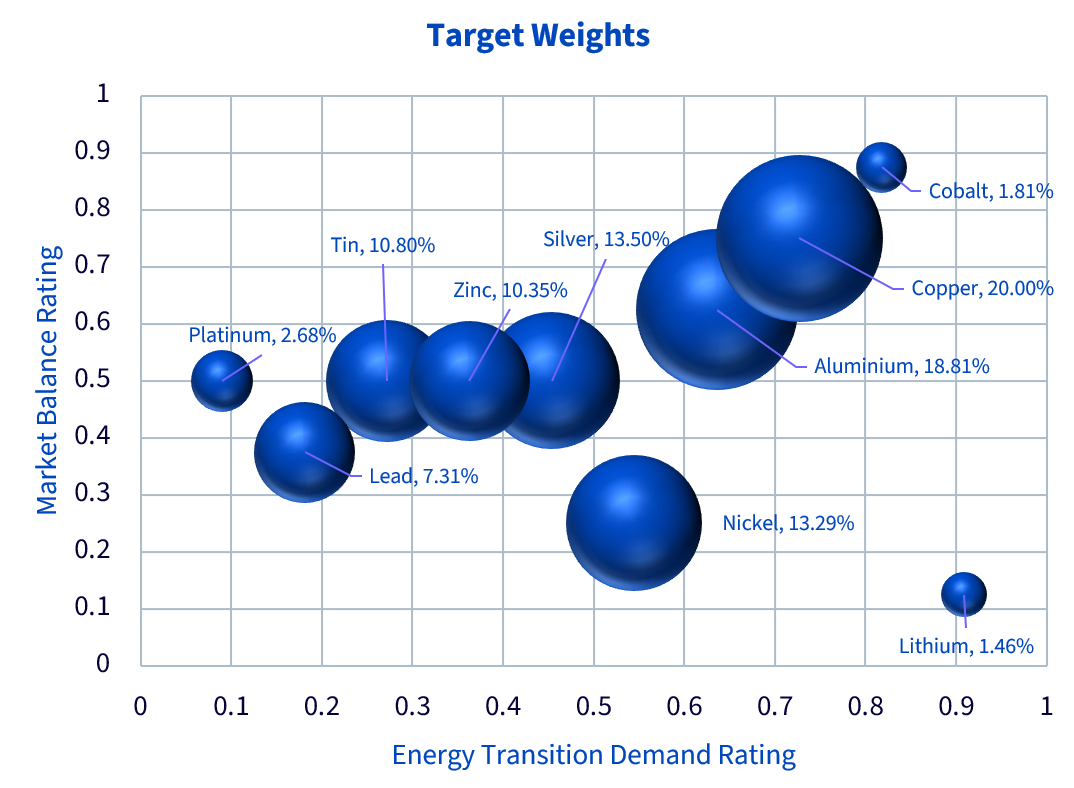

The WisdomTree Strategic Metals UCITS ETF (WENU), WisdomTree Energy Transition Metals (WENT) and WisdomTree Battery Metals UCITS ETF (WATT) are designed to provide exposure to metals positioned to benefit from electrification and tightening market balances.

Following the 12 February 2026 rebalance, weights are determined by:

Metals such as copper and aluminium, combining strong structural demand with tightening balances, receive higher weights.

By incorporating both forward-looking demand growth and current supply dynamics, the strategy seeks to capture metals where policy, electrification and supply constraints converge.

Source: WisdomTree, Wood Mackenzie, based on forecasts, February 2026. Bubble size represents the target weight. Market balance ratings not considered for precious metals and not available for tin. For the purpose of the chart construction, we set the market balance rating at the midpoint (0.5) for these metals. Cobalt and Lithium weights are capped by the methodology at 5% and 2% respectively, and in practice, they are constrained by a liquidity judgment based on market conditions. Index inception: 12 January 2024.

Energy security is evolving into materials security. Governments are responding by stockpiling critical metals. In surplus markets, the impact may be muted and in tightening markets, it may be material.

As electrification accelerates and policy-driven demand increases, understanding inventory dynamics and supply elasticity becomes increasingly important for investors. The geopolitics of the energy system are no longer defined solely by oil flows but by metal availability. And that shift is reshaping markets.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.