RARE LN

WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF - USD Acc

Published 15 August 2025

Associate Director, Quantitative Research

Chinese battery giant Contemporary Amperex Technology Co. Ltd. (Ticker: CATL) surprised the markets in early August when it halted operations at one of its major lithium mines in Jiangxi province. The mine’s output accounts for an estimated 3% of global lithium supply.1

Bloomberg reported on Sunday, August 10, that the company had “failed to extend a key mining permit.” By the end of the following Tuesday, the Chinese spot price for battery-grade lithium carbonate, a critical raw material used in the production of lithium-ion batteries, had jumped 8.5%. Over the same period, shares of global lithium miners and producers, as measured by the Stoxx Global Lithium Miners and Producers Index, rose 9.2%.2

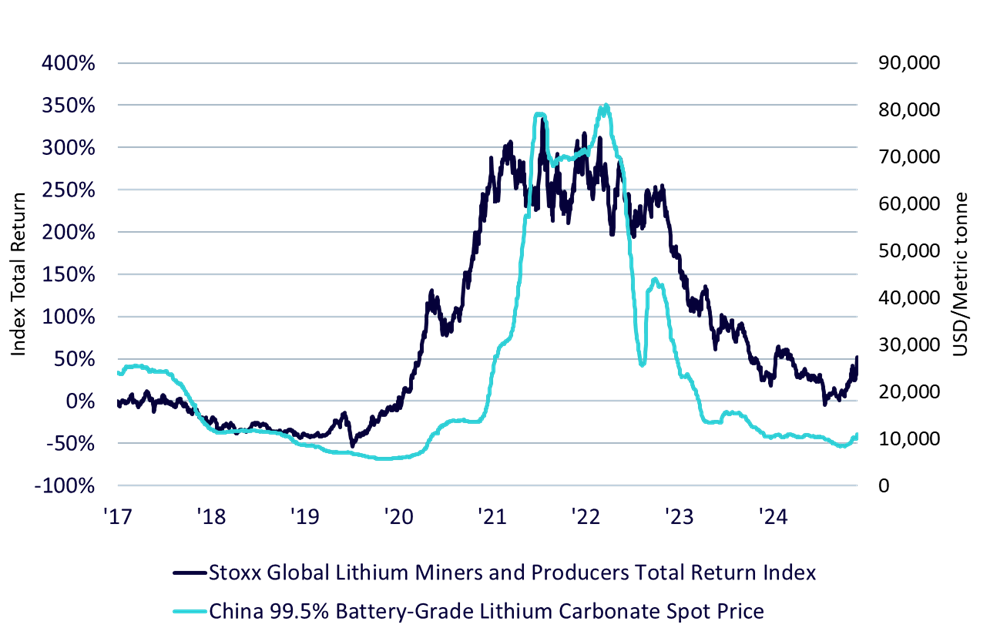

Source: Bloomberg. Data from 18/09/2017 to 12/08/2025. Common history starts from 31/01/2008, which is the earliest available date for the timeseries. Index returns are in US dollars. Historical performance is not an indication of future performance and any investments may go down in value.

To put events into perspective, we look back to July 2020: Lithium prices for battery-grade lithium carbonate had fallen to just $5600 per metric tonne, a level caused by global oversupply and too low for lithium producers to generate profits.

About the same time, global investor focus began shifting towards the energy transition. Clean energy, green transportation, and battery technologies became one of the hottest investment themes of 2020 and 2021, with belief in the potential mass adoption of electric cars manifesting in Tesla’s surging share price and global EV sales growth projections. Investors quickly realized that the key to achieving such growth was the lithium-ion battery production and thus access to lithium.

Two years and a breathtaking price rally later, the Chinese lithium carbonate spot price reached $80,000 metric tonnes, 14 times its 2020 low. In parallel, shareholders of lithium miners and producers saw their investments more than triple (Figure 1).

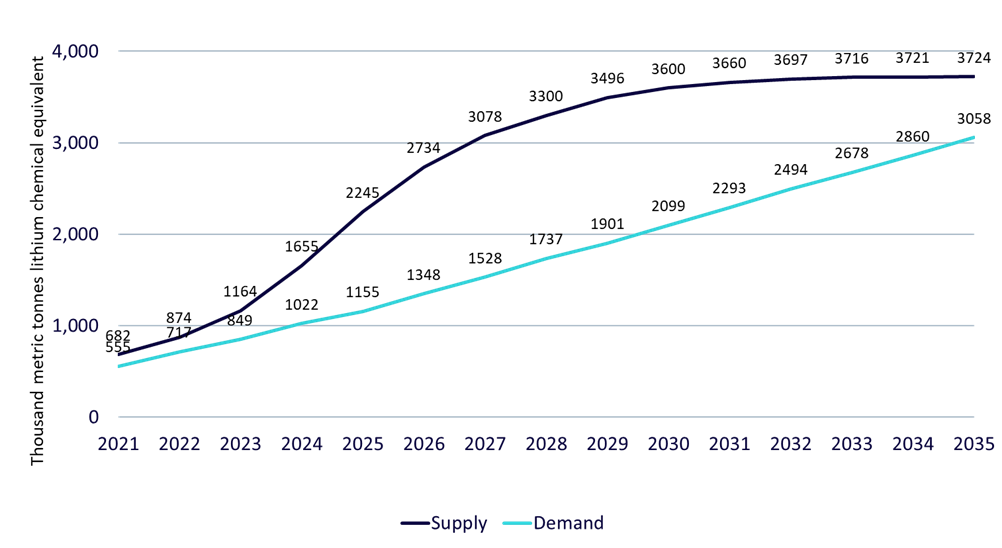

A key challenge of the lithium market is its price-inelastic supply, meaning production is difficult to scale quickly to meet rising demand. In 2020, experts estimated that it takes about 5 years to develop a new lithium mine.3 Nevertheless, the newly lucrative price environment motivated miners and producers to accelerate the expansion of their capacity, leading to an almost doubling of refined lithium supply from 2022 to 2024 (Figure 2).

Source: Bloomberg as of 31 March 2025. The units for lithium are thousand metric tons of lithium chemical equivalent and include lithium carbonate and lithium hydroxide. Historical performance is not an indication of future performance and any investments may go down in value.

Once this new capacity came online, it began to squeeze margins, as lithium prices fell below $9,000 per metric tonne in 2025, levels last seen in 2020. According to energy transition expert Wood Mackenzie4 and data from Bloomberg (Figure 2), the global lithium surplus is expected to peak only toward the end of the decade. Coupled with slower-than-expected EV sales growth in the U.S.5, there was little to suggest a reversal in the downward trend of lithium prices.

In early July, the term “anti-involution” began appearing in investment banks’ analysts’ notes and research reports, describing an emerging trend in China’s industrial policy.6

Loosely translated, “anti-involution” refers to efforts to combat overcapacity and intense price competition.

Lithium mining serves as a good example, with China accounting for 12% of global mining output and 53% of refined lithium carbonate and hydroxide.7 Margins for lithium producers have been thin, and looming trade barriers could drive competition further toward the domestic market, adding pressure on local players.

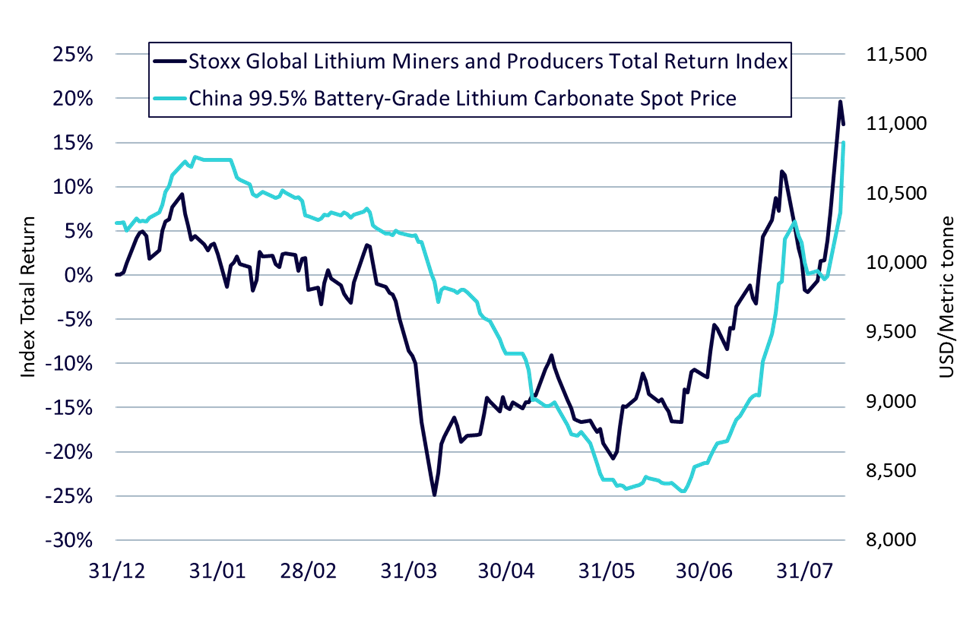

Source: Bloomberg. Data from 31/12/2024 to 12/08/2025. Index returns are in US dollars. Historical performance is not an indication of future performance and any investments may go down in value.

In July, news emerged that Chinese lithium miners were facing increased regulatory scrutiny, raising concerns that mining rights might be used as a tool to control supply.8 The announcement of CATL’s mine shutdown due to missing operating permits confirmed market participants’ thesis on the anti-involution of China’s mining industry, triggering a sharp rally in both lithium spot prices and global mining stocks (Figure 3).

With the anti-involution theme seemingly taking hold in the lithium market, it’s not the only commodity where China’s industry policy can alter supply and demand dynamics. For example, rare earth miners may face similar supply-side scrutiny, as China accounts for nearly 70% of global rare earth mining and almost 90% of global processing.9

The lithium market has been characterized by dramatic price swings, shifting from oversupply to tightness and back to oversupply. Lithium miners’ bottom lines may find a glimmer of hope if China’s emerging anti-involution policy succeeds in curbing oversupply and halting the deflationary trend in lithium prices.

The recent shutdown of CATL’s mine may be a first serious indication of China’s commitment to follow through. If sustained, such measures could help stabilize prices, restore margins, and potentially reshape the competitive landscape for both domestic and global lithium producers. However, with EV demand growth slowing in key markets and new mining capacity still in the pipeline, the road to balance will likely continue to be volatile.

1 Bloomberg as of 10 August 2025

2 Source: Bloomberg. Returns in US dollars from 8 August 2025 to 12 August 2025. Historical performance is not an indication of future performance and any investments may go down in value.

3 Financial Times as of 3 December 2020

4 Wood Mackenzie as of 13 May 2025

5 Bloomberg as of 10 July 2025

6 Bloomberg as of 13 July 2025

7 Bloomberg as of 31 March 2025

8 Bloomberg as of 28 July 2025

9 The Oxford Institute For Energy Studies as of July 2023

Associate Director, Quantitative Research

Tobias Lazar is an Associate Director in WisdomTree’s Quantitative Research Team, where he focuses on developing innovative exchange-traded products across various asset classes and supporting WisdomTree’s diverse range of offerings. Before joining WisdomTree, he worked in the index research and development teams at Nasdaq and Solactive, where he was responsible for developing equity and alternative risk premia indices. Tobias holds an MSc in Financial Engineering from the University of Birmingham, UK, a BSc in Mathematics from the University of Cologne, and is a Chartered Alternative Investment Analyst (CAIA).