Platinum's turn to shine in 2019

Published 3 July 2019

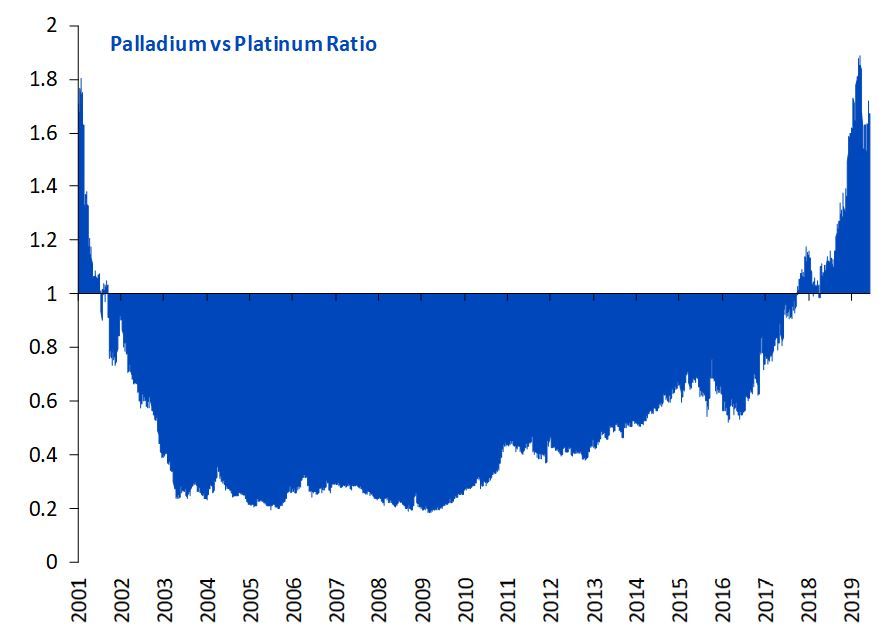

Palladium has staged a strong performance rising 140% over the last 3 years (from 6 June 2016 to 6 June 2019) in comparison to its sister metal platinum whose performance has languished over the same period rising only 35% owing primarily to the dieselgate scandal sparked by Volkswagen in 2016. While the two precious metals tend to be closely related as they derive a large part of their use (about 40% for platinum and 75% for palladium) from the auto industry, their recent performances have diverged considerably. After attaining an all-time high of US$1599.6 per troy ounce on 20 March this year, palladium’s price appreciation has begun to unwind. We believe palladium’s current price correction was long overdue and is not yet over as there is more downside to come. However, in the case of platinum, prices are starting to recover, and fundamentals point to higher upside in 2019. The palladium to platinum ratio (shown in the chart below) hit a record high on 18 March at 1.888 and since then the ratio has begun to unwind as platinum prices recover and palladium prices decline.

Figure 1: Palladium versus platinum ratio begins to unwind in 2019

Source: Bloomberg, WisdomTree, data available as of close 31 May 2019. Historical performance is not an indication of future performance and any investments may go down in value

Stringent emissions regulation bodes well for platinum demand

The global auto industry has been witnessing a slow down after reaching record growth in 2018. According to the China Association of Automobile Manufacturers, since the start of 2019 car sales in China have declined almost 15% over the prior year. According to the European Automobile Manufacturers Association (ACEA) demand for new cars in the European Union decreased by 2.6% amounting to 5.3 million units registered in total from January to April 2019. In the US, new vehicle sales from January through April fell 3% however they posted an unexpected increase in May 2019.

Figure 2: Global auto sales growth

Source: Bloomberg, WisdomTree, data available as of close 31 January 2011 to 31 May 2019. Historical performance is not an indication of future performance and any investments may go down in value

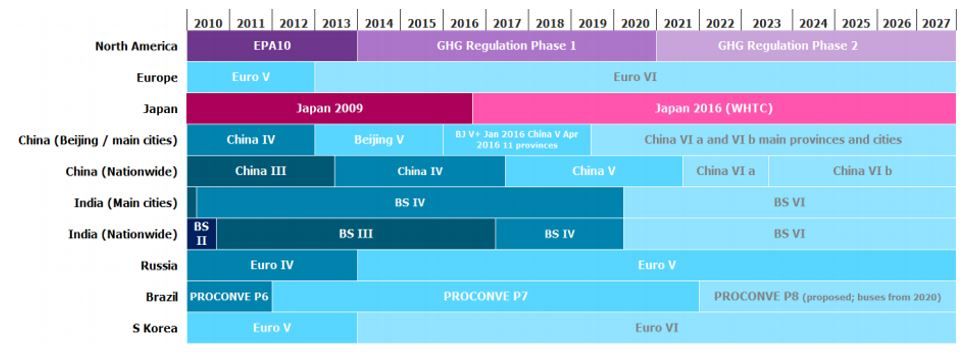

While the auto industry endures a slowdown, stricter legislation globally which will be rolled out over the 2019-2021 period is likely to support demand for platinum and palladium. Gasoline powered catalytic convertors utilise platinum or palladium in combination with rhodium. Diesel powered catalytic convertors have a much higher platinum loading. We expect the implementation of stricter heavy-duty emission limits in China and India to augment demand for platinum in comparison to palladium.

Figure 3: Emissions Legislation for Heavy Duty Vehicles

Source: Johnson Matthey, WisdomTree as of 31 May 2019

Please Note: BSVI – Bharat Stage VI in India; EuroVI – Euro 6 Regulation; China VI – China VI legislation

In China, heavy duty vehicles adopting Platinum group Metal (PGM) catalysts are expected to rise sharply in line with their governments “Blue Sky protection” plan which has seen the early rollout of China VI legislation. From July 2019, all trucks sold in several cities and Chinese provinces must be equipped with advanced aftertreatment systems. Consumption of platinum in Electric Vehicles (EVs) powered by fuel cells (FCEVs) is also expected to rise in lockstep with the Chinese government’s New Energy Vehicle (NEV) programme that is aimed at promoting EVs. Similarly, in India home to the world’s second largest market for light duty diesel cars existing aftertreatment systems have almost zero to low platinum loadings due to light duty emissions legislation. However, this is set to change as the market transitions from BSIV (equivalent to EuroIV) to BSVI (equivalent to Euro VI) standard from April 2020 which should bolster demand for platinum owing to higher catalyst fitment rates. Platinum loadings on European diesel cars are expected to continue to fall in 2019. As European automakers seek to comply with Euro6d-TEMP regulations, there has been a wider use of non-PGM selective catalytic reduction (SCR) for NOx conversion, in place of platinum containing lean NOx traps (LNTs). We expect the consumption of platinum in China and India to more than offset the fall in platinum usage in Europe in the auto industry.

Investment demand to outpace other sources of platinum demand

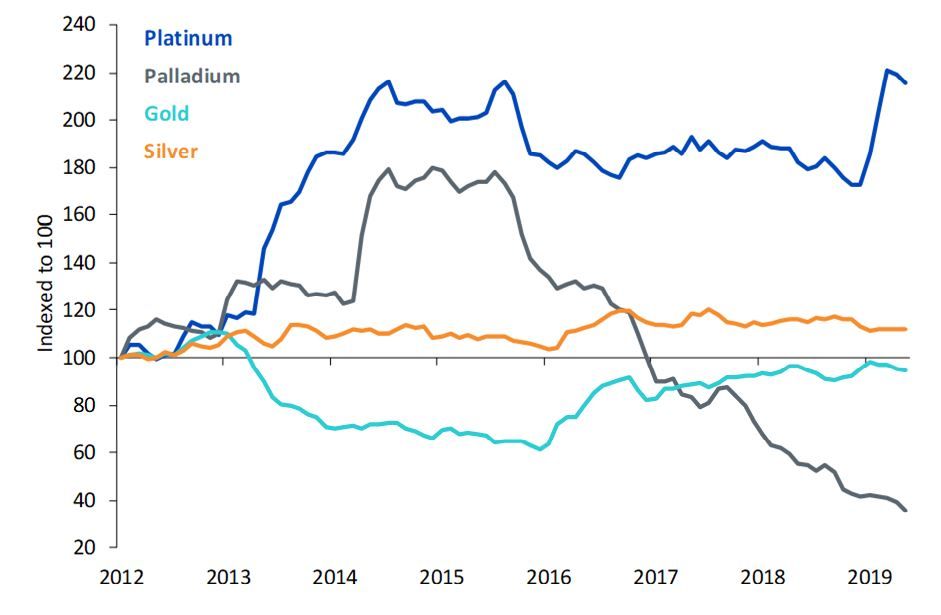

Jewellery demand which accounts for nearly 30% of platinum’s use is expected to remain weak in its primary market – China. However, India’s consumption of platinum in jewellery is set to expand albeit from a small base. Strong demand from industrial applications (that account for 18% of platinum use) is also expected due to structural factors with glass, petroleum and chemical companies adding capacity to meet the demand for products such as fibreglass, plastics and silicones. From an investment standpoint, demand for platinum Exchange Traded Funds (ETFs) have garnered considerable momentum (evident from the chart below) since the start of 2019 and we expect the demand to continue towards the end of 2019. In contrast, palladium ETFs have witnessed considerable outflows. Since the start of the second quarter, ETF investors have sold 85,000 ounces of palladium and as much as 100,000 ounces since the start of the year.

Figure 4: Physically backed Exchange Traded Funds (ETFs)

Source: Bloomberg, WisdomTree, data available as of close 31 May 2019. Historical performance is not an indication of future performance and any investments may go down in value

Supply deficit expected in the platinum market this year

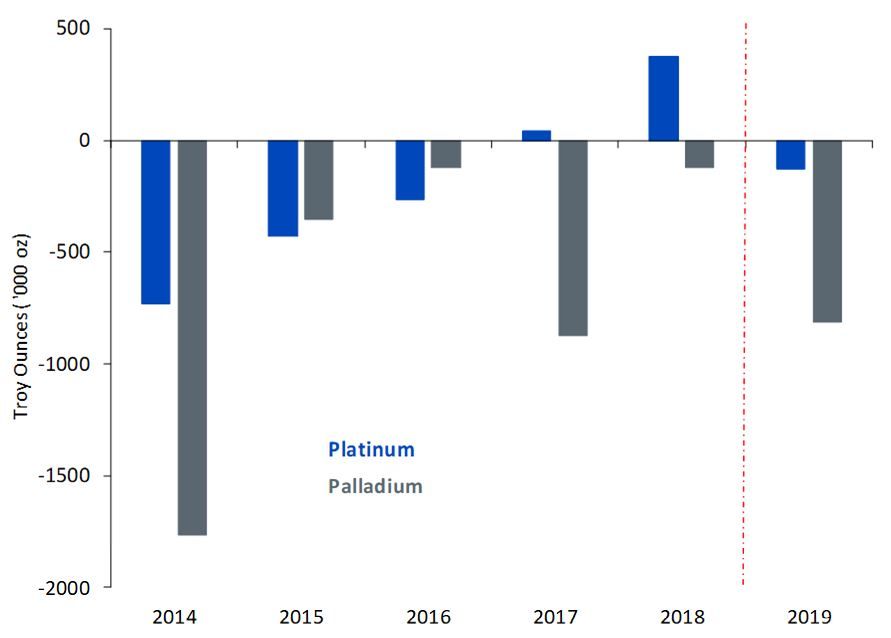

According to Johnson Matthey, the world’s largest refiner of platinum and palladium, the platinum market is expected to move into a small supply deficit of 127,000 ounces after being in a surplus over the prior two years. South Africa is responsible for producing nearly 80% of the world PGM supplies. Platinum producers in South Africa are preparing for collective wage negotiations with the unions over the summer period. Given its history, the Association of Mineworkers and Construction Union (AMCU) is known to enter the collective 3-year wage negotiations with challenging demands raising the risk of a strike that could reduce supply on the global platinum market. So far, the AMCU union has already demanded that workers should benefit from higher PGM prices. We do not expect negotiations to result in widespread strike action, but we would not rule out the risk of short-term strike action given the intense negotiations.

Figure 5: Net Balance on platinum versus palladium market

Source: Johnson Matthey, WisdomTree, data available as of close 31 May 2019. Please Note: 2019 numbers are a forecast. Historical performance is not an indication of future performance and any investments may go down in value

After staging a relatively weak performance relative to palladium over the prior three years, we expect platinum prices to benefit from rising regulatory environment in the auto industry, higher investment demand and stable demand from the industrial sector. While the palladium market is expected to remain in a supply deficit for the seventh consecutive year, we believe palladium prices have run ahead of itself and its price correction has further room. The Platinum market is expected to be in a supply deficit this year after two consecutive years of surplus, combined with a more optimistic demand outlook we expect platinum prices to recover this year.

Categories

Related articles

The IPO wave reshaping the European defence sector

What's Hot: The geopolitical turning point for Europe and Japan

MP Materials and the race to rebuild rare earth supply chains: Ryan Corbett on The Next Big Thing

Strategic metals rebalanced: expanding exposure across the energy transition value chain

What’s Hot: Oil prices begin pricing the peace

What my daughter's reaction to a BlackBerry tells us about investing in megatrends

Renewable energy is catching a second wind

European defence: strong fundamentals behind a soft market

What’s Hot: What falling oil Inventories could mean for energy markets

About the contributor

Aneeka Gupta

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.