RARE LN

WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF - USD Acc

Published 24 June 2026

The global race to secure critical minerals is now reshaping trade flows, industrial policy and supply chains. A recent UN Trade and Development (UNCTAD) Global Trade Update describes how demand for the minerals essential to the energy transition and advanced technologies such as lithium, cobalt, nickel, copper and rare earth elements, is transforming global commerce. Especially as governments and manufacturers pivot away from traditional commodity-trade patterns toward supply-chain resilience and reduced dependence on a narrow set of suppliers. China remains the dominant player across many of these value chains, particularly in processing and refining, while Australia, Indonesia, Chile and several African nations are expanding their presence in both raw materials and higher-value segments. UNCTAD also cautions that supply-chain concentration and geopolitical tension have been amplified by export controls, subsidies and other strategic measures could create new vulnerabilities for global trade.

That theme dominated this year's Geneva Dry commodities-shipping conference, where panellists pointed to copper as one of the clearest long-term demand stories, underpinned by electrification, electric vehicles (EVs) and industrial growth, set against chronic under-investment in new supply. Several producers are now building strategic inventories of key minor-bulk commodities as a hedge against disruption. The investment implication is the same one driving this rebalance: these materials increasingly function as policy instruments and supply-security assets, not just commodities and the companies that mine, refine and process them sit at the centre of the story.

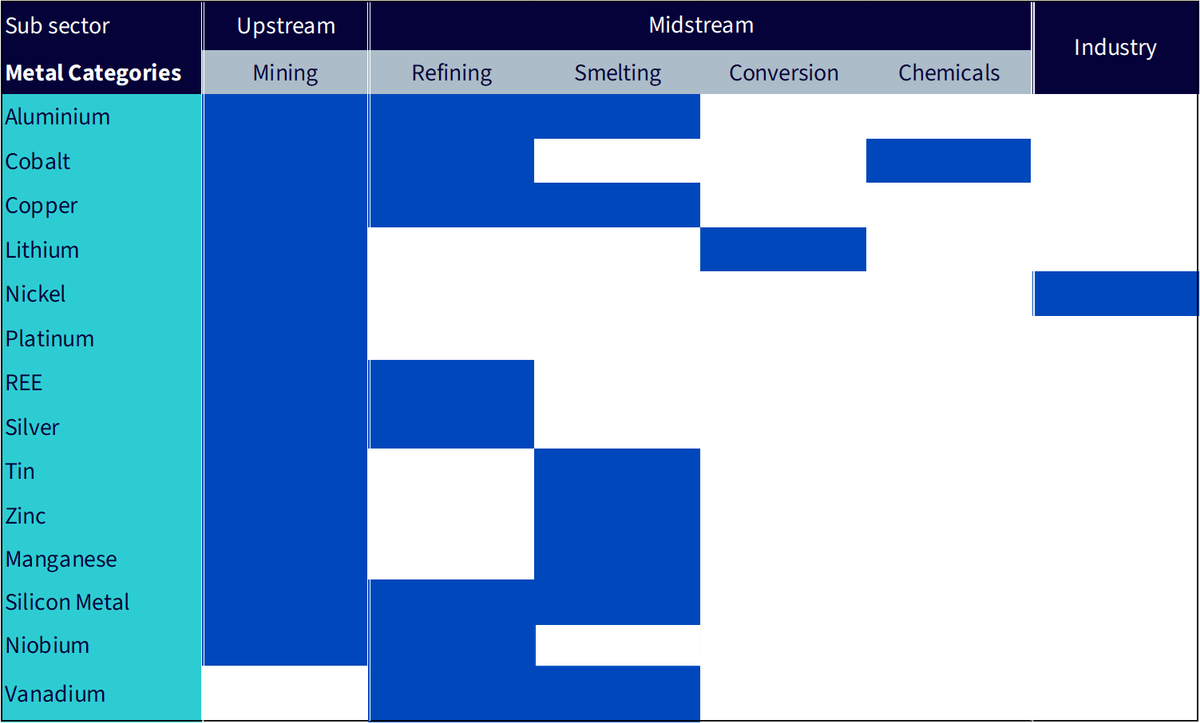

Against this backdrop, the WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF (Ticker: RARE) provides diversified equity exposure to the Energy Transition Metals Value Chain (ETMVC). The latest rebalance of the underlying index (WTMRAREN) on 22 May drove a notable expansion of the metal categories from 10 to 14.

Source: Wood Mackenzie, WisdomTree as of 22 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

The Index now spans 14 metal categories, with four new additions: manganese, silicon metal, niobium, and vanadium, each reflecting a distinct and structurally important role in the energy transition and advanced industrial economy.

Together, these categories now account for roughly 5.5% of the Index, with the bulk of the heavy lifting from the rebalance happening within the established metal categories.

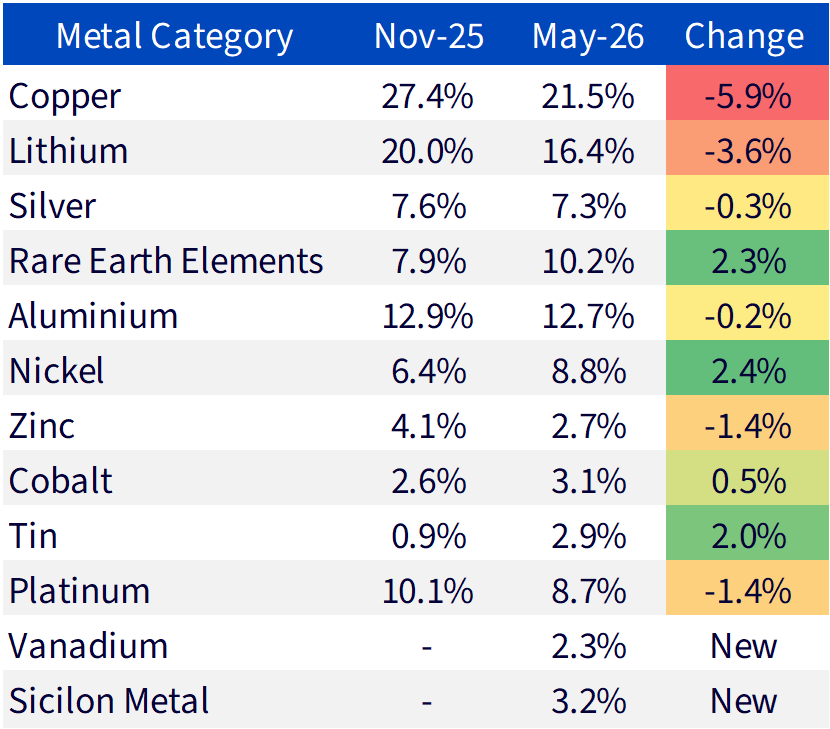

Within those established categories, the most notable shift is a trimming of the index's two largest positions, copper and lithium, in favour of rare earths, nickel and tin, alongside the new categories. Copper remains the single largest category but its weight fell by nearly six points, while lithium was cut as some of late-2025's lithium-equity momentum unwound. Rare earths rose meaningfully, consistent with the strategic premium the market continues to place on supply-chain security, and nickel gained on the back of processing and battery-chain exposure.

Source: FactSet, WisdomTree, Wood Mackenzie as of 22 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

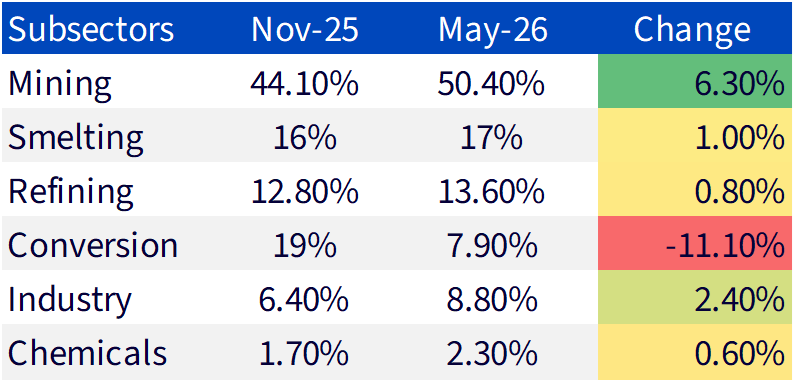

Where the November rebalance rotated into conversion, this rebalance partially reverses that, with mining and smelting gaining at conversion's expense. This reflects the rare earth and nickel weighting increases (both mining-heavy) and a market that, amid supply disruptions, is again rewarding control of physical upstream and processing capacity, even as copper's weight was trimmed. The sharp drop in conversion weight (down nearly 11 points) is largely a function of the lithium trim, as lithium converters were a major conversion-subsector contributor in the prior portfolio.

Source: FactSet, WisdomTree, Wood Mackenzie as of 22 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

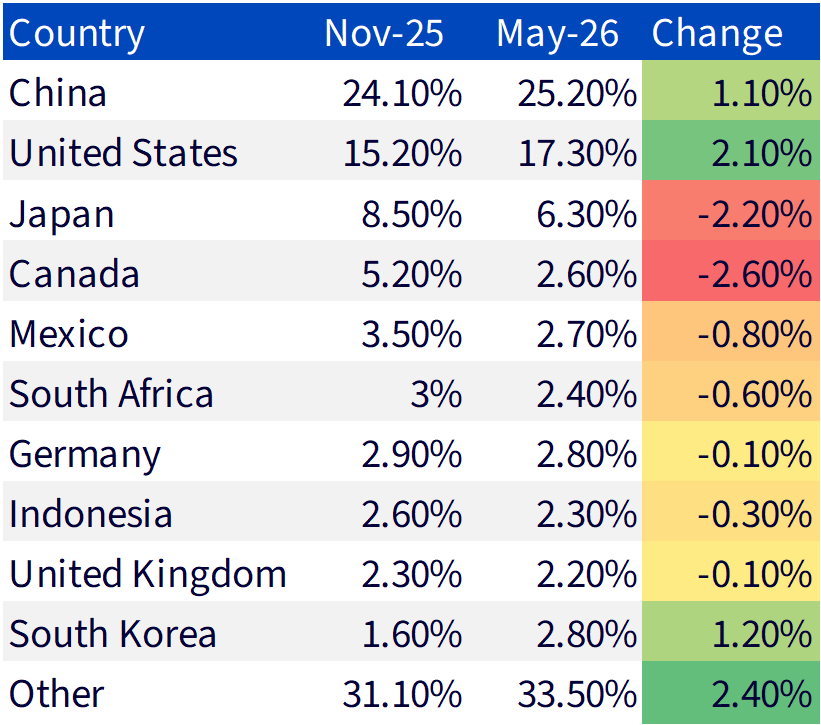

The breakdown of weights by geographic revenue moved meaningfully. The United States was the standout gainer (+2.1 points), consistent with the index's tilt toward US-aligned supply-chain development, while China edged higher to remain comfortably the largest country exposure, reflecting the addition of Pangang (vanadium) and Tongwei (silicon) and the continued importance of Chinese refining and processing capacity. South Korea rose (+1.2 points) on the back of nickel and cathode names.

Source: FactSet, WisdomTree, Wood Mackenzie as of 22 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

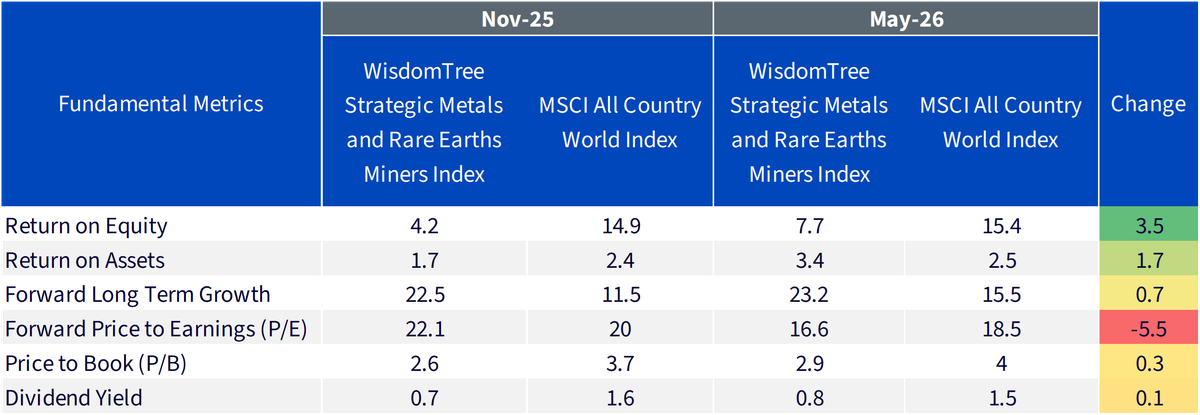

The valuation picture has improved following the rebalance. The Index now combines above-market forward growth with improving profitability and a forward earnings multiple that has de-rated since the Iran war. Forward long-term growth of 23.2% is roughly 1.5x the MSCI All Country World Index's 15.5%, while return on equity has nearly doubled (from 4.2% to 7.7%) and return on assets (3.4%) now sits above the benchmark. Crucially, the index's forward P/E fell from 22.1x to 16.6x, moving from a slight premium to the benchmark at the November rebalance to a discount today (16.6x versus 18.5x for the ACWI).

Source: FactSet, WisdomTree, Wood Mackenzie as of 22 May 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

The expansion of the WisdomTree Strategic Metals and Rare Earths Miners Index from 10 to 14 metal categories reflects the evolving material demands of the energy transition.

The early framing of the critical minerals story was dominated by lithium, cobalt, and nickel (the core battery metals) and by rare earth elements essential for permanent magnets in EV motors and wind turbines. The transition will also require vast quantities of copper for electrification infrastructure, manganese for green steel and advanced battery technologies, silicon for solar energy systems, and vanadium for grid-scale energy storage, which is essential to supporting high levels of renewable power generation.

At the same time, the geopolitical backdrop has become materially more complex, with energy security moving back to the centre of the strategic metals story. The ongoing conflict in the Middle East has exposed how quickly an energy-supply shock can ripple through the critical-materials complex. Elevated fuel prices are accelerating the adoption of electric vehicles, boosting demand for magnet rare earths and battery metals, while military stockpiling and defence spending are increasing demand for heavy rare earth elements.

Against that backdrop, an index that tracks not just the commodity prices but the companies extracting, processing, and refining these materials across the value chain offers investors a structurally relevant expression of the critical materials theme.

Investments in mining and metals-related companies can be volatile and may be affected by commodity price movements, geopolitical developments, regulatory changes, environmental requirements and operational risks. The Fund has a concentrated thematic exposure and may experience greater volatility than broader equity markets. Investments in emerging markets and smaller companies may involve additional risks. The value of investments may go down as well as up and investors may not get back the amount originally invested.

1 Wood Mackenzie as of 30 April 2026

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.