Gold above US$1400, where next?

Published 26 June 2019

Gold prices are currently trading at very important technical levels. The fact that gold surpassed and stayed above US$1400/oz is an important milestone, after breaching US$1350/oz on Thursday 20 June. US$1350/oz acted as key resistance point, as gold failed to breach those levels 6 times before in September 2017, January 2018, February 2018, March 2018, April 2018 and February 2019. Having risen above another ‘round number’ is symbolically important. Gold is currently trading at highest levels since March 2013.

The last time gold traded above US$1350/oz was shortly after the UK’s referendum on EU membership in mid-2016, when speculative positioning in gold futures hit an all-time high.

Clearly something changed.

We previously expected the US Federal Reserve (Fed) to remain on hold for the year (although its ‘dot-plots’ were guiding the market for a hike in 2020). But the market forced the Fed’s hands, then the central bank indicated at its June meeting that it could cut rates in 2020 and the market is pricing in a cut at the July meeting.

US 10-year Treasury yields fell significantly below 2.0% (from 2.4% at the end of March 2019 and over 3% in October 2018). The recent surge in gold prices reflect the dovish stance of the Fed and this precipitous drop in yields.

The question is: is there still further upside? Based on our revised assumptions, we believe so.

Figure 1: WisdomTree’s gold price forecast

Source: WisdomTree Model Forecasts, Bloomberg Historical Data, data available as of 20 June 2019

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Using WisdomTree’s quantitative framework outlined in “Gold: How we value the precious metal”, we project gold prices could rise to US$1480/oz by end of Q2 2020. This is based on a relatively conservative set of assumptions:

- US Treasury yields to remain at current levels. The market has largely priced-in more cuts that the Fed itself is guiding. Fed Fund futures are indicating the market is looking for two to three rate cuts in 2019. Our forecast for gold—at 1480—just uses current levels for long-term interest rates. A further drop in rates would support even higher prices.

- US dollar basket remaining around 97. Although cutting interest rates would normally be associated with currency weakness, we believe that the Fed will not be alone in expressing a dovish bias. That is likely to avoid large appreciation or depreciation of the US dollar. Indeed, with accusations of ‘currency wars’ re-emerging, gold could be seen as the haven currency during the course of the year (especially among emerging market central banks, who appear to want to diversify their foreign currency reserves), as it has been in the past.

- Inflation to reach 2%. Although weak inflation is the driver for the Fed’s change in policy course (with CPI inflation currently at 1.8%), we believe at the headline level, inflation could rise as a result of higher oil prices. We believe weakness in demand for oil - that could result from prolonged trade tensions for example – would be countered by the Organization of the Petroleum Exporting Countries (OPEC) policy decisions. OPEC’s policy meeting has been rescheduled for 1st July, after the G20 meeting takes place on 28th/29th June, which highlights how the cartel wants to understand demand projections (which can only happen when we know where the world’s largest consumers—US and China—are heading).

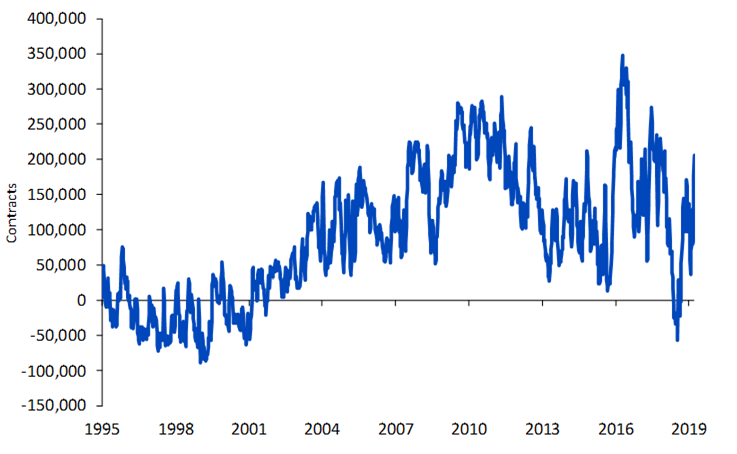

- Investor sentiment for gold may not remain as elevated as today, but with so many geopolitical concerns, there are upside risks. Speculative positioning in gold futures has risen substantially in recent weeks and surpassed our expectations. Speculative length is over 205k contracts net long—a substantial rise from 55k net short in October 2018. We don’t think it will remain this elevated on a base case basis (and we assume positioning at 120k contracts). However, we note that many risks could crystallise in the near future. Within the next week are several keys risks:

- At the G20 meeting on 28th/29th June, China and US may not see eye-to-eye and disappoint the market with further escalation in their trade war

- On June 27th, Iran is likely to announce it has breached the nuclear accord and thus risks military intervention with the US

- At the G20 meeting on 28th/29th June, China and US may not see eye-to-eye and disappoint the market with further escalation in their trade war

- On June 27th, Iran is likely to announce it has breached the nuclear accord and thus risks military intervention with the US

Figure 2: Net speculative positioning in gold futures

Source: Bloomberg, WisdomTree, data as of 20 June 2019

Historical performance is not an indication of future performance and any investments may go down in value

In conclusion, based on our quantitative model and a relatively conservative set of assumptions, we believe gold still has room to go materially higher.

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Related blogs

+ Gold: WisdomTree's price forecasts to Q1 2020

+ Gold: how we value the precious metal

+ Why the gold price rally may continue

Related products

+ ETFS Physical Swiss Gold (SGBS)

About the contributor

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.