QGRW LN

WisdomTree US Quality Growth UCITS ETF - USD Acc

Published 3 September 2025

Director, Quantitative Research

Director, Research

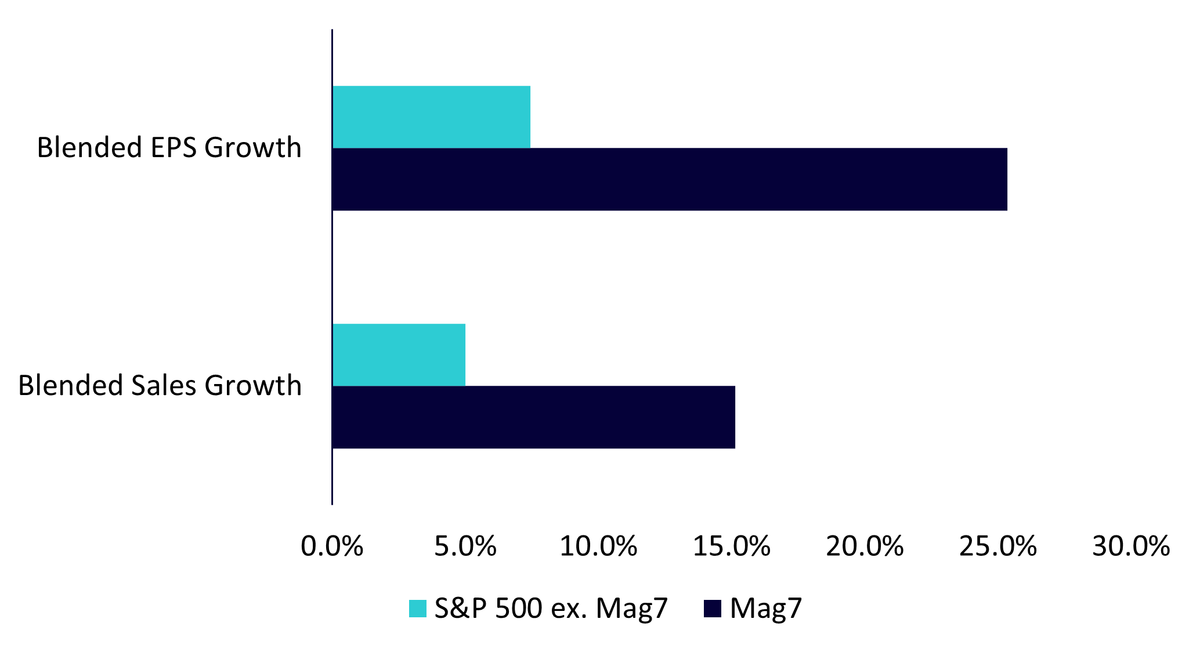

‘Magnificent 7’ leadership reaffirmed in Q2 2025 results

The Q2 2025 earnings season reaffirmed the market dominance of the Magnificent 7 (Mag7)1. Collectively, the group delivered blended sales growth of +15.13% year-on-year, outpacing the rest of the S&P 500 (493 companies) by more than 10% as of 15 Aug 2025. From the April market lows, an index tracking these seven stocks advanced +44.46% as of 19 August 2025, a stark reflection of their continued leadership.

The 2-4 April 2025 sell-off, triggered by new White House tariffs, caused the S&P 500 and Nasdaq to drop -10% to -12%, erasing USD 6.6 trillion in market cap within three days. A partial rollback of tariffs quickly stabilised markets, and by the end of April, the Zweig Breadth Thrust signalled recovery.

By May–June, the rally broadened significantly:

While the Mag7’s valuations have soared, they remain supported by:

Importantly, the Mag7’s price/earnings-to-growth (PEG) ratio suggests valuations are justified. Bridgewater analysis shows that 14% annual earnings per share growth (EPS) growth over the next decade would be sufficient to sustain their equity premium relative to bonds, a level below their historic ~20% pace, but still robust enough to support current multiples.

Source: WisdomTree, FactSet. As of 15 Aug 2025. Blended growth rates include estimates for companies where latest quarterly report isn’t yet available.

Artificial Intelligence is the defining growth driver for the Magnificent 7, with each company leveraging AI in ways that reinforce its market leadership and profitability:

Crucially, AI is not just an investment theme but already yielding measurable returns:

In short, AI provides the Mag7 with a multi-dimensional growth engine, expanding revenues, protecting margins, and strengthening competitive moats. Their AI dominance cements them at the centre of long-term equity growth opportunities.

With elevated equity market capitalisations, Big Tech wields powerful “equity currency” for acquisitions. This allows them to preserve cash for organic growth and R&D and use stock valuations strategically in deal-making. In practice, this means they can issue shares at high multiples to acquire complementary technologies, talent pools, or new platforms, often at a lower effective cost than if they relied on cash. It also provides flexibility: by structuring deals with stock rather than debt, they avoid increasing leverage, maintain balance sheet strength, and still expand strategically. Importantly, equity-financed deals can align incentives with acquired management teams, as they participate in the long-term value creation of the combined entity.

The WisdomTree US Quality Growth UCITS Index currently holds all seven Mag7 stocks, not due to size, but because they meet stringent quality and growth fundamentals. The strategy selects stocks with robust profitability and strong growth metrics, and applies semi-annual rebalancing to ensure continued discipline:

This systematic, rules-based approach ensures that investors gain exposure to the quality and growth risk premia that have historically been rewarded in equity markets.

Name | Weight |

|---|---|

NVIDIA Corporation | 15.4% |

Microsoft Corporation | 14.2% |

Apple Inc. | 11.1% |

Amazon.com, Inc. | 8.9% |

Alphabet Inc. Class A | 8.1% |

Meta Platforms Inc Class A | 5.7% |

Broadcom Inc. | 4.6% |

Tesla, Inc. | 3.9% |

Eli Lilly and Company | 2.4% |

Visa Inc. Class A | 2.1% |

Source: WisdomTree, FactSet. As of 31 Jul 2025.

The Mag7 remains central to the US Quality Growth Strategy, backed by operational efficiency, leadership in megatrends, massive AI investments, and strategic M&A capacity. While valuations are elevated, they appear justified by strong fundamentals and sustained growth prospects.

For long-term investors, a rules-based, quality-focused framework of the WisdomTree US Quality Growth UCITS Index provides a disciplined way to capture Mag7 leadership while also systematically rotating into other high-quality growth opportunities, enhancing both resilience and diversification.

1Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla

WisdomTree US Quality Growth UCITS ETF - USD Acc

Director, Quantitative Research

Ayush Babel is the Director of Quantitative Research in WisdomTree's multi-asset quantitative research and index teams. In this role, he focuses on developing innovative quantitative strategies across various asset classes while supporting WisdomTree's diverse range of products. His expertise spans factor exploration, portfolio construction and optimization, quantitative investment research, and product development.

With over a decade of experience in the financial services industry, Ayush has held investment research roles at J.P. Morgan and Franklin Templeton. At these institutions, he was responsible for developing and managing equity and fixed income smart beta products, as well as cross-asset risk premia solutions for global institutional and retail clients. His experience covers a broad spectrum of asset classes and investment styles.

Ayush holds a bachelor's in Engineering Physics and a master’s degree in Nanoscience from the Indian Institute of Technology, Bombay.

Director, Research

Piergiacomo is Director of Research at Wisdomtree. He has over 20 years of experience within the financial services industry, having served as the Head of Discretionary Portfolio Management at Banca Albertini Spa in Milan before joining WisdomTree. Prior to this, he held roles at Rasbank Spa (currently AllianzBank Financial Advisors) as Head of Equity Research and Head of Equity Desk. Piergiacomo has an M.Sc. in Financial Markets Economics from Bocconi University in Milan. He is also a chartered member of the Aiaf (Italian Association of Financial Analysts).