WGLD LN

WisdomTree Core Physical Gold

Published 4 September 2025

When we published “Finding Antivenoms in the Year of the Snake” in March 2025, we identified trade and geopolitics as the decisive pressure points for commodity markets. That view has been vindicated. Conflicts in Eastern Europe and the Middle East remain unresolved, while April’s “Liberation Day” tariffs unleashed one of the most significant shocks to global trade in over a century. Yet despite this turbulence, commodities have not wilted. Quite the opposite: they have shown remarkable resilience.

So far in 2025, precious and industrial metals have led the charge, while energy markets, though volatile, have avoided outright collapse. Beneath the surface lies a deeper story – a weakening US dollar, disrupted supply chains, and long-term structural demand shifts extending far beyond today’s headlines.

Gold has once again assumed its classic role as a safe-haven asset. After peaking at $3,500 per ounce in April, prices have consolidated in a tight range, supported by geopolitical risks, fiscal imbalances, and concerns about central bank independence.

We view this consolidation as a “loading the spring” phase – a period of stability that often precedes a major breakout. Our forecast calls for gold to reach $3,850 per ounce by Q2 2026.

The reasons are straightforward:

In short, gold is more than just a defensive trade, it is becoming the clearest expression of systemic unease.

Metals are the backbone of three major themes shaping the global economy:

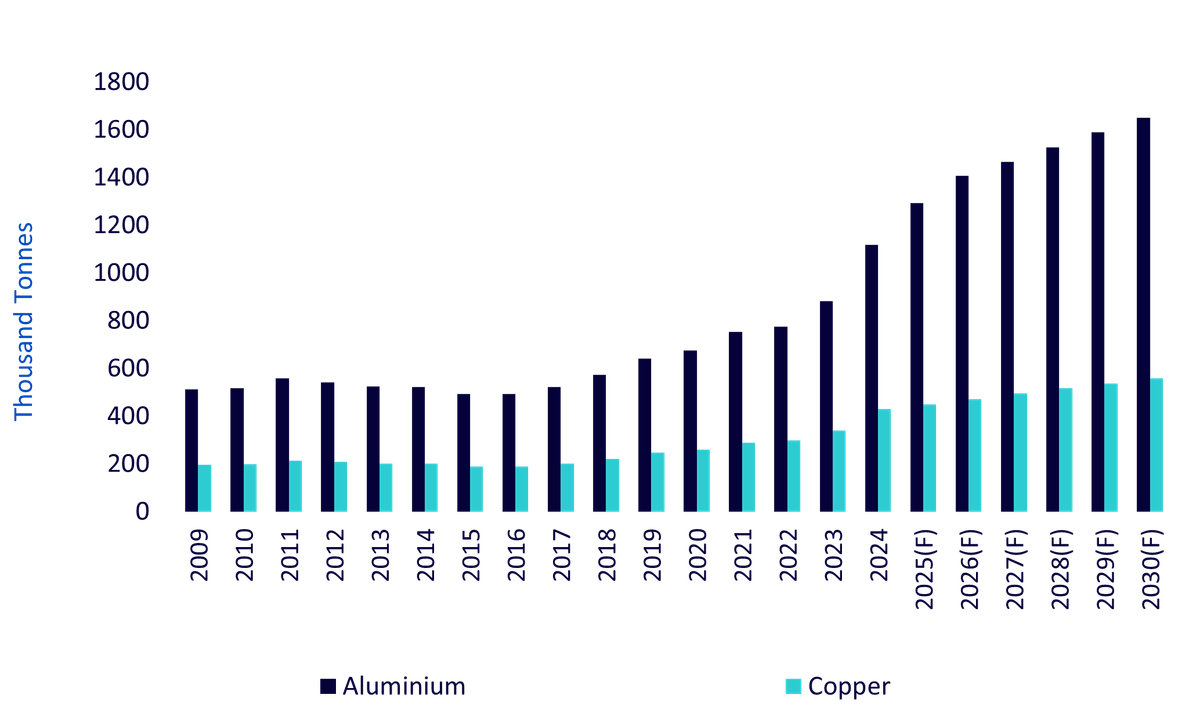

Source: Bank of America, From mine to missile: the metals behind modern defence, 15 July 2025. Historical performance is not an indication of future performance, and any investments may go down in value.

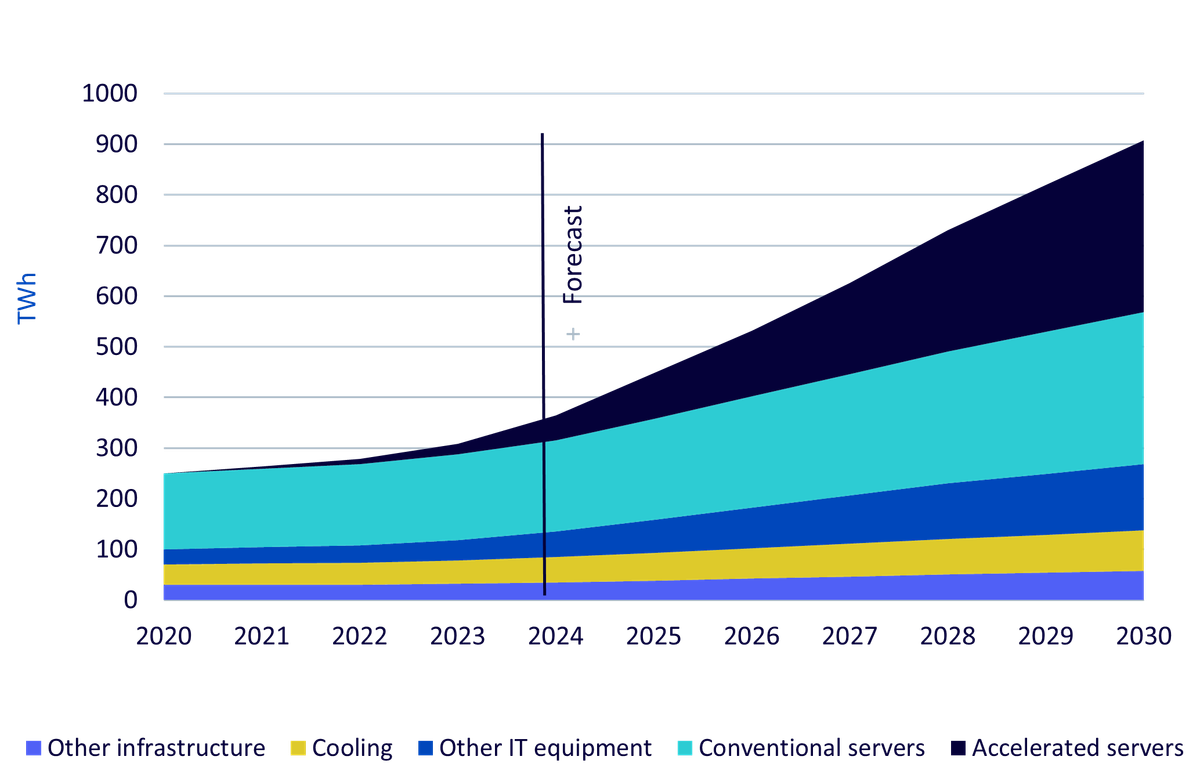

Source: WisdomTree, International Energy Agency, Energy demand from AI, 2025. Historical performance is not an indication of future performance, and any investments may go down in value.

The near-term noise of tariffs should not distract from these longer-term supply constraints. Exploration spending has stalled, and aluminium smelting faces acute challenges due to its energy intensity and rising competition for grid resources. The result: a persistent supply-side squeeze that will underpin prices over the medium term.

If metals have been resilient, energy has been volatile. Brent crude surged nearly 20% in June before dropping by 11% in two weeks. This turbulence is not an anomaly; it has become the defining feature of oil markets in 2025.

The key driver has been the Organisation of the Petroleum Exporting Countries and partner countries (OPEC+), which has accelerated the unwinding of its voluntary production cuts. By September 2025, a full year ahead of schedule, the group is expected to remove 2.2 million barrels per day of supply. Motivations vary, from Saudi Arabia’s frustration with quota cheating, to geopolitical bargaining with Washington, to efforts to claw back market share from US shale and Brazilian production.

Even so, the outlook remains capped. With China’s demand stagnating and electrification advancing, Brent crude will likely remain range-bound at $60–$70 per barrel. Short-term spikes will occur, but they are unlikely to be sustained.

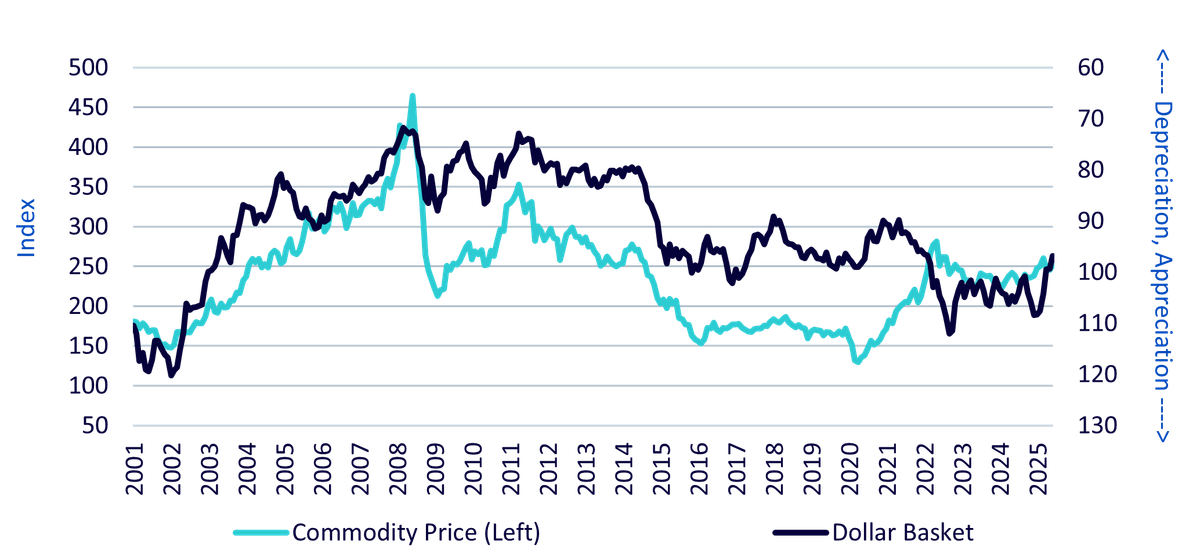

Perhaps the US dollar's reversal is the most underappreciated driver of commodity strength. After rising to 110 in January, its strongest since 2022, the dollar index has fallen to 97 by mid-year, a decline of 12%. This represents the steepest depreciation since the onset of the pandemic.

A weaker dollar boosts commodities in multiple ways:

Market consensus points to further declines into 2026. While not an official policy, Washington’s tolerance for a soft dollar reinforces the supportive backdrop for commodities.

Source: WisdomTree, Bloomberg, January 2001- June 2025. Bloomberg Commodity Index Total Return and Dollar Basket (DXY). Historical performance is not an indication of future performance, and any investments may go down in value.

Trade wars and supply chains: The serpent strikes

Tariffs remain the single largest source of disruption to global commodity flows. The April “Liberation Day” announcement marked the most aggressive escalation in US tariffs in over a century. Aluminium, steel, and semi-finished copper products were hit with 50% duties, while agriculture also faced new barriers, including a 30% tariff on Brazilian exports.

For now, energy flows have been spared, reflecting the administration’s desire to shield consumers from higher fuel costs. However, the ripple effects are felt in refined products such as diesel, where Canada-to-US flows are under scrutiny.

These policy shocks fragment supply chains, forcing producers and consumers to rewire sourcing strategies. The uncertainty has added a risk premium to metals like platinum, palladium, and silver, which markets fear could face tariffs in the future.

The bigger picture: Scarcity, security, strategy

Looking across sectors, three themes dominate:

Conclusion: Coiled potential

As we head deeper into the Year of the Snake, commodities are not just reacting to shocks; they are expressing the underlying fragilities of the global system. Gold is consolidating before another potential breakout. Industrial metals face near-term headwinds but are structurally indispensable. Oil is volatile but capped. The weakening dollar provides a broad tailwind to the entire complex.

For investors, the lesson is clear: volatility is the new normal, but so is opportunity. In a world defined by fragmentation and uncertainty, commodities remain not just a hedge but a reflection of the age itself.

For WisdomTree’s full Market Outlook, please click here.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.