QGRW LN

WisdomTree US Quality Growth UCITS ETF - USD Acc

Published 4 December 2024

Director, Quantitative Research

Over the years, Quality as an investing factor has developed a reputation for providing the most consistent performance gains versus the market. Veteran investors, like Warren Buffett, have relied on return on equity as one of the factors to evaluate investments and empirical research by academics, such as Fama and French, also suggests that profitability is one of the key factors behind superior investment returns.

When looking at the returns of High-Quality US stocks versus their Low-Quality1 counterparts, we see a distinct separation in performance, with high quality stocks not only outperforming by close to 4% annualised (12.0% vs 8.1%) over more than 60 years, but also doing so with a much lower volatility of 15.2% versus 17.8% annualised from June 1963 to Aug 2024.

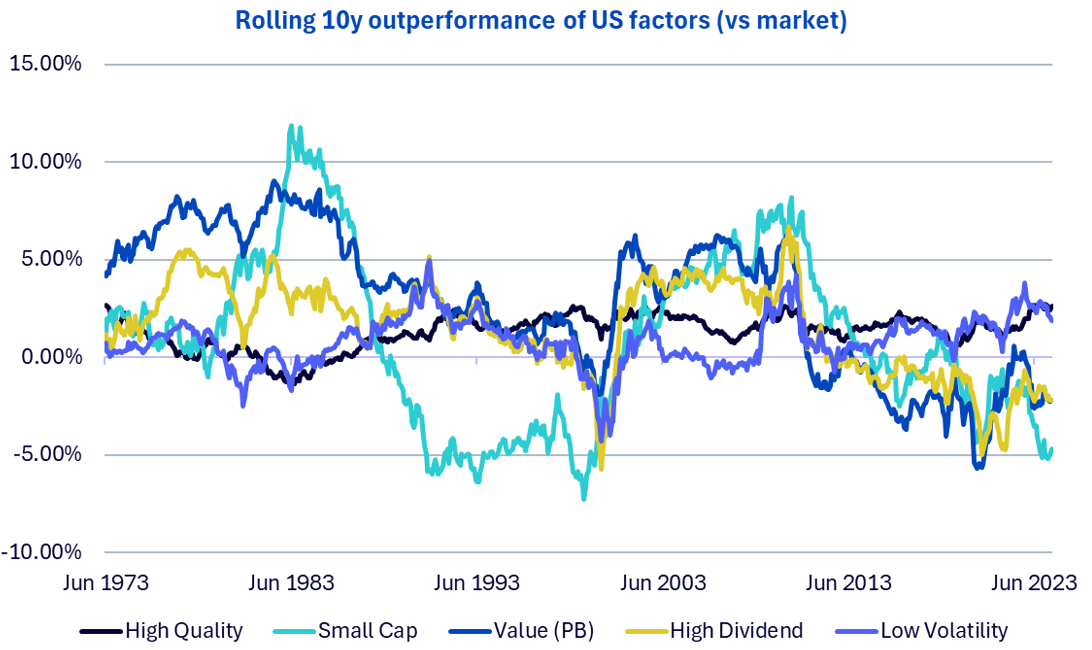

When compared to other factors Quality has also exhibited the most resilience by outperforming much more often than all the other factors over 10 year rolling periods, making it an all-weather factor crucial for core portfolio allocations.

High Quality | Small cap | Value | High Dividend | Low Volatility | |

|---|---|---|---|---|---|

Percentage of outperforming periods | 90% | 58% | 73% | 71% | 77% |

Best outperformance | 2.7% | 11.9% | 9.1% | 6.7% | 5.0% |

Worst underperformance | -1.4% | -7.3% | -5.7% | -5.7% | -4.3% |

Sources: WisdomTree, Ken French, data as of 31 May 2024 and represents the latest date of available data. Value: High 30% Book to Price portfolio. Size: Low 30% portfolio. Quality: High 30% portfolio. Low Vol: Low 20% portfolio. High Div: High 30 portfolio. "&" Market: all CRSP firms incorporated in the U.S. and listed on the NYSE, AMEX or NASDAQ. Historical performance is not an indication of future performance and any investments may go down in value.

Taking this into consideration, WisdomTree has developed two unique strategies, with Quality as the underlying factor, that provide differentiated exposures to the US market.

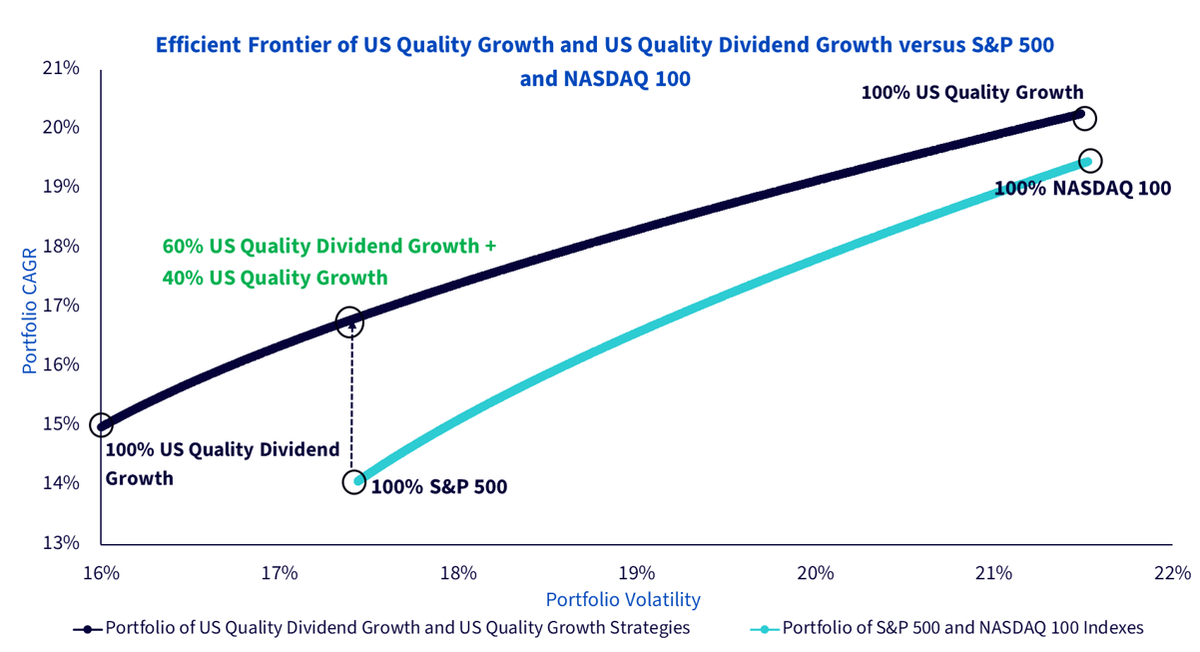

We performed an efficient frontier analysis that demonstrates the superior risk-return profile of the two strategies.

For all levels of volatility, portfolio variations of the WisdomTree US Quality Dividend Growth Index (DGRW) and WisdomTree US Quality Growth Index (QGRW) have historically generated better potential returns than portfolios of S&P 500 and NASDAQ 100.

Source: WisdomTree, FactSet, Bloomberg. Based on backtested data from 30 April 2013 to 30 Sep 2024. Historical performance is not an indication of future performance and any investments may go down in value.

DGRW and QGRW can serve as a balanced approach for investors seeking downside protection and potential growth. DGRW focuses on dividend-paying stocks with a history of profitability, which tend to perform well during economic uncertainty or downturns. On the other hand, QGRW provides exposure to growth stocks, including high-quality tech and innovation-focused companies, offering more potential upside during bull markets.

This combination is likely to create a diversified portfolio that could withstand various market conditions. By blending DGRW’s focus on steady dividend payers with QGRW’s growth exposure, investors could potentially balance their portfolios to manage risk while still capturing possible growth opportunities.

Source

1 Based on Kenneth French data library data. Stocks selected are above the median market cap among all the US listed stocks, with ‘High-Quality’ representing the top 30% by operating profitability and ‘Low-Quality’ representing the bottom 30% by operating profitability.

Director, Quantitative Research

Ayush Babel is the Director of Quantitative Research in WisdomTree's multi-asset quantitative research and index teams. In this role, he focuses on developing innovative quantitative strategies across various asset classes while supporting WisdomTree's diverse range of products. His expertise spans factor exploration, portfolio construction and optimization, quantitative investment research, and product development.

With over a decade of experience in the financial services industry, Ayush has held investment research roles at J.P. Morgan and Franklin Templeton. At these institutions, he was responsible for developing and managing equity and fixed income smart beta products, as well as cross-asset risk premia solutions for global institutional and retail clients. His experience covers a broad spectrum of asset classes and investment styles.

Ayush holds a bachelor's in Engineering Physics and a master’s degree in Nanoscience from the Indian Institute of Technology, Bombay.