DGSE LN

WisdomTree Emerging Markets SmallCap Dividend UCITS ETF

Published 7 March 2025

After two years of remarkable equity returns—especially in the US—the global market landscape is now set for a period of both opportunity and caution. In 2024, US equities outperformed those in Europe, Japan, and emerging markets (EM)1, largely due to a surge following the US elections and expectations of a Trump-led administration that promised renewed economic vigour.

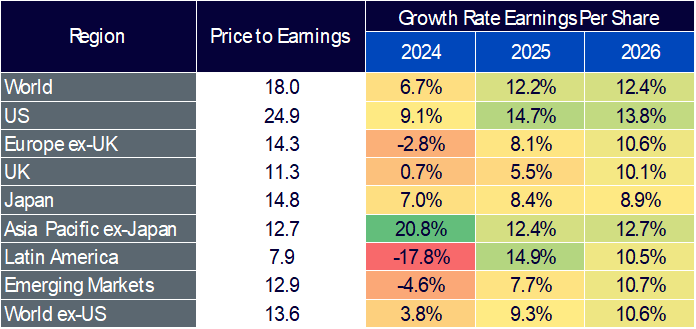

Source: FactSet, MSCI, WisdomTree as of 10 January 2025. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

Multiple expansion and the US premium

The US economy remains a global standout, benefiting from expected earnings-per-share (EPS) growth of 14.7% in 20252. Yet, much of this anticipated growth is already priced into the market. The performance of the US, largely driven by a narrow segment of high-performing stocks, has contributed to an increasingly concentrated S&P 500 index—a trend mirrored in the broader MSCI All Country World Index. Equal-weight strategies, which offer exposure to the often-overlooked ‘forgotten 493’ stocks, can help mitigate concentration risk while uncovering attractively priced opportunities.

For investors, regional equity valuations offer contrasting prospects. While the US market has become overextended, regions like EM, Europe, and Japan remain relatively attractively valued. Diversification, though it offered limited protection in 2024, is more essential than ever in 2025 to manage risk and capture opportunities across regions when future returns cannot rely solely on valuation expansion.

Fundamentals: the long-term driver

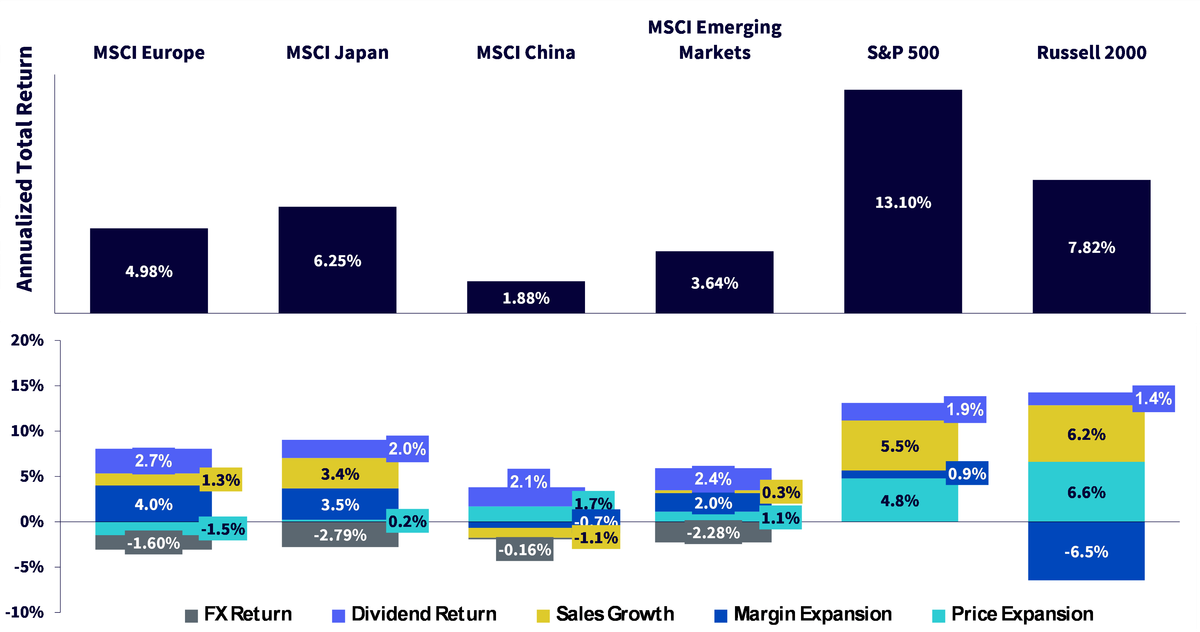

Over the past decade, the strength of fundamentals—consistent sales growth and margin expansion—has underpinned long-term equity returns. For instance, US large-cap and Japanese equities have reaped the benefits of robust fundamentals. However, US large caps face a potential ceiling in price expansion due to already high valuations, while US small caps have been held back by weaker margin improvements. Similarly, Chinese equities have lagged because of modest sales and margin growth alongside unfavourable currency impacts. On the other hand, European equities have enjoyed higher dividend yields and margin expansion, though political uncertainties have dampened price momentum.

Figure 2: Equity return attribution (trailing over 10-years)

Source: FactSet, WisdomTree as of 31 December 2024. Historical performance is not an indication of future performance, and any investments may go down in value.

Resilience of emerging market small caps

While Trump’s policies have generally supported US assets through a higher dollar and rising yields, these same factors have created headwinds for emerging market exporters. Amid rising protectionism, EM equities managed a modest 5% increase in 20243. However, within this region, small-cap stocks have shown resilience. With a focus on domestic revenues, these companies are less exposed to international trade disruptions and currency fluctuations—a stark contrast to their larger peers. Historical data reinforces this point: during President Trump’s first term (2017-2021), EM small caps outpaced large caps by delivering gains of 54% versus 42%4. Furthermore, their lower correlation with US dollar fluctuations makes them a strong defensive play, particularly when combined with dividend yields that offer additional insulation in higher-rate environments.

Germany’s DAX: a beacon amid macroeconomic challenges

Germany provides a prime case study for how robust market performance can occur even when macroeconomic conditions are less than ideal. In 2024, the DAX outperformed the broader European equity index by returning 18.8% compared to 13.5%5. Key drivers behind this strong performance include tailwinds from artificial intelligence (AI), cloud computing, and the electrification trend, as well as supportive financials. Despite lagging consumer cyclicals—driven by the automotive sector’s challenges and tepid economic growth—the diversified revenue base of German companies (with over 80% of revenue generated internationally) has helped offset these challenges6.

So far in 2025, the under-pricing of tariff risks, has given European exporters a distinctive edge in domestic markets. By not fully pricing in the potential impact of US tariffs on European goods, European exporters maintained competitive pricing and expanded market share. The underperformance of the Euro versus the dollar has made European exporters that much cheaper. This under-pricing has been a critical factor behind the stellar performance of many export-oriented sectors, as it helps offset cost pressures and drive revenue growth. Exporters have been able to leverage this pricing advantage, providing an important tailwind for the performance of European equities in 2025.

Japanese equities enjoyed one of their best years since 1989 in 2024, driven by robust earnings growth and the continuation of corporate governance reforms. Despite volatility, Japan’s broad-based rally has been supported by improving fundamentals and a structural shift from industrial production to services. Reforms such as the Tokyo Stock Exchange’s initiative for companies trading below a 1x price-to-book ratio have spurred progress. Yet given that 44% of TSE's Prime Market-listed companies are trading with their P/B7 ratios below 1x, offers plenty of room for improvement from a governance perspective8.

The tourism sector has been a standout performer, with a surge in foreign visitors and spending that has significantly bolstered the economy. On the labour front, record-high wage negotiations signal potential improvements in nominal wages, though real incomes have yet to fully recover to pre-pandemic levels. As the Bank of Japan adopts a cautious approach to rate hikes—projecting only modest increases in 2025—investors are likely to favour value-oriented stocks that can benefit from a rangebound yen and share buybacks.

Conclusion: a cautiously optimistic outlook

The global equity landscape in 2025 is characterised by pronounced regional disparities and an evolving interplay between macroeconomic fundamentals and political risk. While the US market continues to deliver strong earnings growth, its concentrated nature and high valuations introduce new risks. In contrast, emerging markets—particularly the resilient small caps—and undervalued regions like Europe and Japan offer attractive opportunities for diversification. Investors are advised to adopt a balanced approach that combines growth and defensive exposures, remaining vigilant to geopolitical uncertainties and fiscal challenges, especially in a climate shaped by Trump’s protectionist policies.

For WisdomTree’s full Market Outlook, please click here.

1Bloomberg as of 31 December 2024.

2FactSet, MSCI, WisdomTree as of 10 January 2025.

3Bloomberg as of 31 December 2024.

4Bloomberg from 2 January 2017 to 30 December 2021.

5Bloomberg as of 31 December 2024.

6Deutsche Industrie – und Handelskammer.

7Price-to-book.

8Bloomberg, WisdomTree as of 31 December 2024.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.