DXJ LN

WisdomTree Japan Equity UCITS ETF - USD Hedged

Published 18 December 2024

Japanese growth has been volatile over the past year. While economic output in Q3 grew strongly by 0.3% quarter-on-quarter, two of the last five quarters saw negative growth. A shift away from industrial production towards services appears to be underway. This is evident from the progress witnessed in the auto and tourism sectors. The auto industry is expected to produce 12% fewer vehicles in 2024 than in 20191. In sharp contrast, the tourism industry has seen an average of 3 million foreign visitors a month arrive in Japan, 13% more than in 2019. Foreign tourists are spending more money per trip than then did before the pandemic.

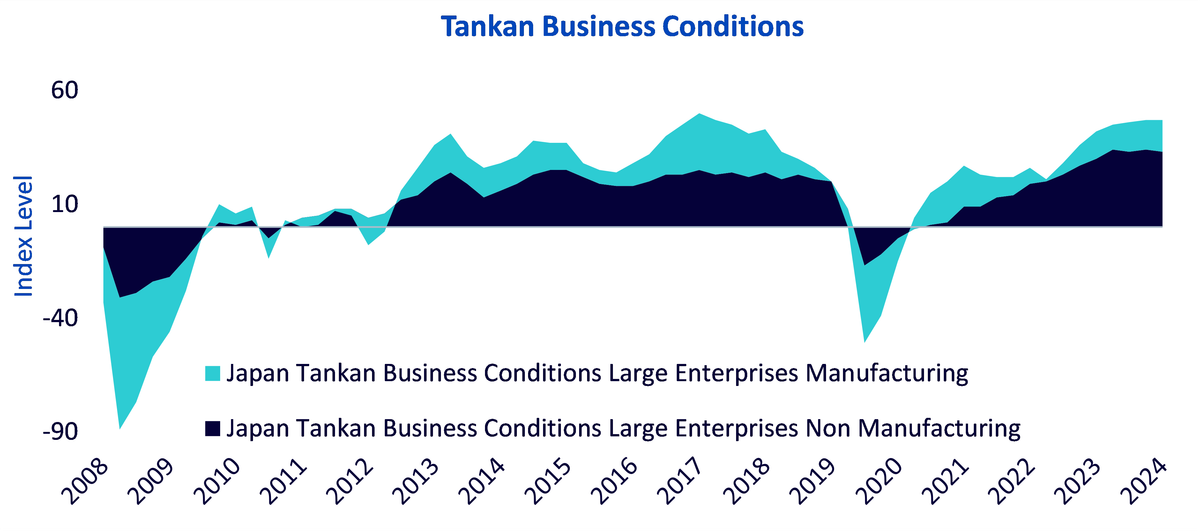

The latest Tankan survey revealed strong business sentiment, particularly in the services sector, and so we expect to see economic stabilisation in Japan next year.

Source: Bank of Japan, Tankan Survey as of 12 December 2024. Historical performance is not an indication of future performance and any investments may go down in value.

In response to rising inflation and its impact on households and businesses, the Japanese government has approved a comprehensive economic stimulus package valued at approximately ¥39 trillion (around $250 billion)2. The package is noteworthy as it includes measures proposed by the opposition – the Democratic Party for the People (DPP). One of the DPP’s main policy agendas is to lift the ceiling on tax-free income from the current level of ¥1.03mn, thereby stimulating consumption. By lifting the ceiling, the DPP hopes to encourage part-time employees to work longer hours thereby alleviating the shortage in Japan’s labour market. Part timers are also less inclined to save, so lifting the ceiling should support higher consumption

Measures include subsidies to curb rising energy costs and cash handouts to low-income households, as well as an increase in the tax-free salary threshold to boost disposable incomes. In a sign of policy continuity with his predecessor Fumio Kishida, Shigeru Ishiba wants to bring about conditions where wage gains outpace inflation and growth is investment driven.

Inflation in Japan has recovered from its high of over 4% in 20233 to just over 2% in 2024, primarily due to high goods prices. Services prices have been hovering around the 2% mark this year. Interestingly, tourism has been an important contributor to services inflation. The recreational services subcomponent posted the highest rate of inflation compared to other services over the prior year. If recreational services are excluded from the services sector, it has failed to rise above 2% and is currently only around 1% year-on-year.

This year the Shunto wage negotiations reached 5.1%, its highest level since 1991 according to Japan’s largest umbrella group for labour unions4. This increases the likelihood of nominal wages rising over the next year. Yet, as real incomes remain below pre-pandemic levels, the Bank of Japan (BOJ) wants to see wages rise in tandem with inflation. Prices in the services sector have risen no faster for labour intensive services than for services with a low wage cost component so Japan is unlikely to experience a wage price spiral.

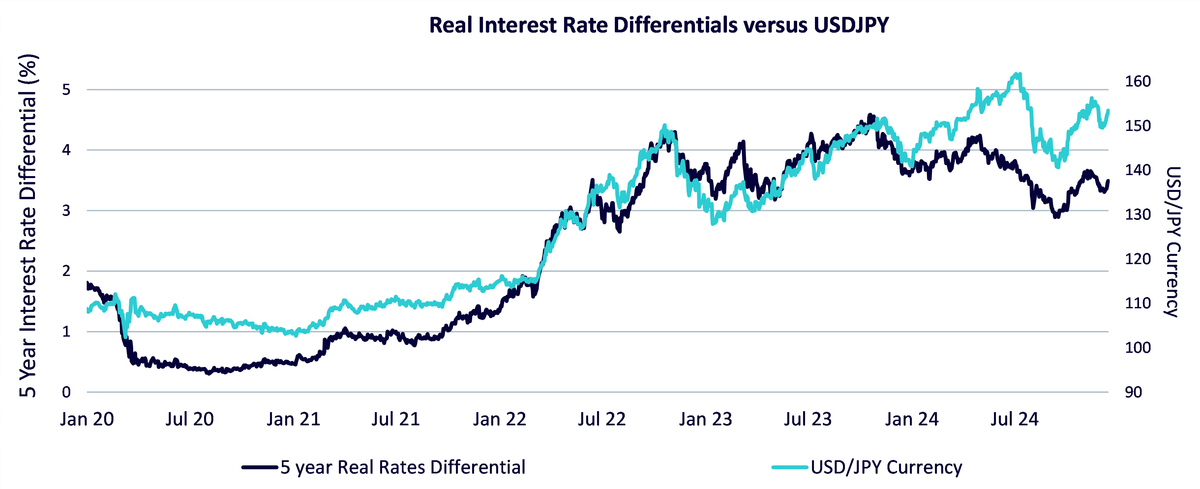

While inflation in Japan is unlikely to return to zero, it won’t justify a sustained cycle of interest rate hikes by the BOJ. The global environment following the US presidential election supports this view as the market has dialled down on expectations of further interest rate cuts in the US. Thus, a further interest rate hike by the BOJ is less likely to result in strong market reaction as witnessed in August 2024.

Source: Bloomberg, WisdomTree as of 13 December 2024. Historical performance is not an indication of future performance and any investments may go down in value.

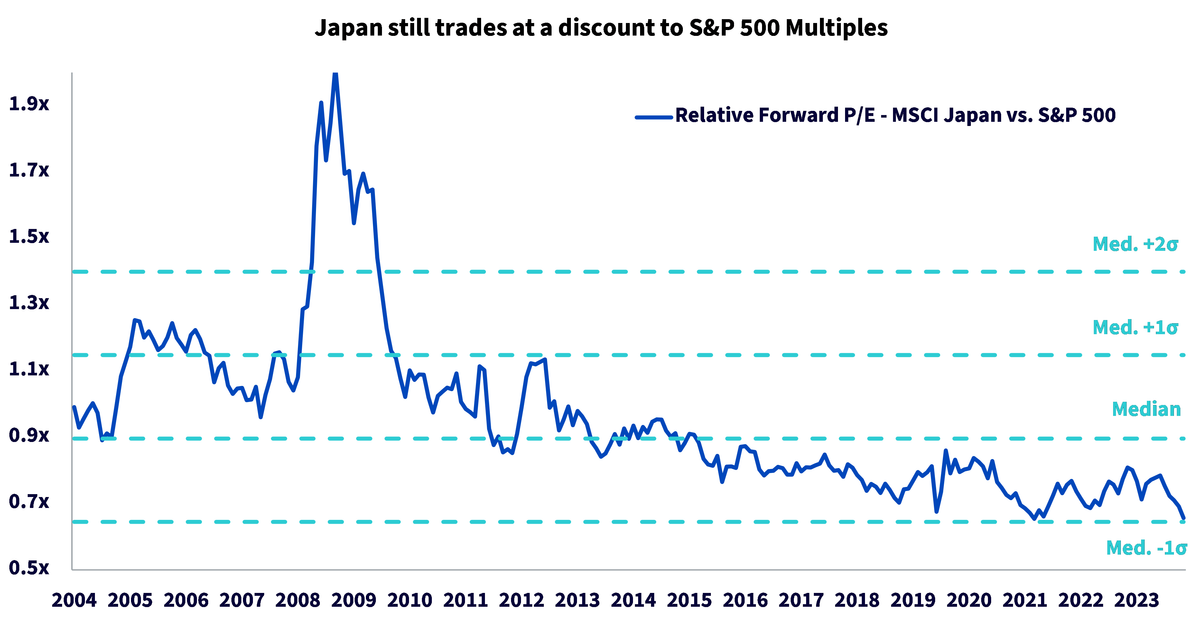

As a result, the likelihood of the yen remaining weak against the US dollar for the rest of the year remains high. The yen continues to play a major role in corporate fundamentals. Initiatives aimed at deepening corporate governance reforms have encouraged cash rich companies to put their capital to productive use. Japanese exporters continue to benefit from a weaker yen and resilient global macro backdrop. In 2024, the WisdomTree Japan Hedged Equity UCITS Index rose 28.8% whilst the Nikkei Index rose 19.1%5. Despite the strong performance in 2024, Japan still trades at a significant discount to the S&P 500 Index with the relative forward Price to Earnings (P/E) multiple approaching 1-standard deviation below the median, providing an attractive route to diversify concentrated portfolios.

Source: Bloomberg, WisdomTree as of 30 November 2024. Historical performance is not an indication of future performance and any investments may go down in value.

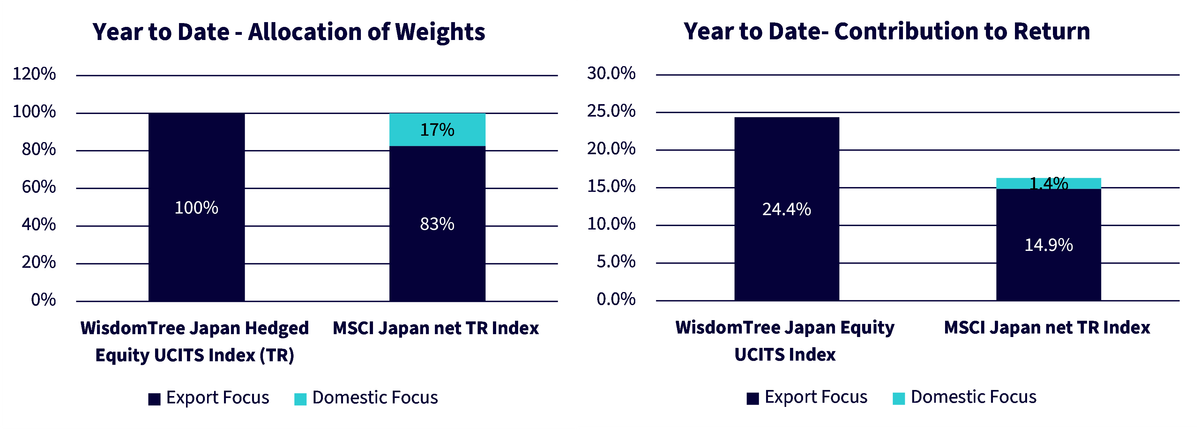

Taking a hedged exposure, amidst the weaker yen versus the US dollar with the WisdomTree Japan Equity UCITS ETF - USD Hedged (Ticker: DXJ) provided a higher return of 25.9% year-to-date in 20246. Dollar-based investors get a free carry trade sweetener for tapping into Japanese equities. Investors can earn a 4.7% return from swapping their in-demand dollar for yen, near the highest level since 2000. The outperformance of the WisdomTree Japan Hedged Equity UCITS Index versus the MSCI Japan net Total Return Index is closely tied to its higher tilt towards dividend paying Japanese exporters as highlighted below.

Source: FactSet, WisdomTree from 29 December 2023 to 29 November 2024. Historical performance is not an indication of future performance and any investments may go down in value.

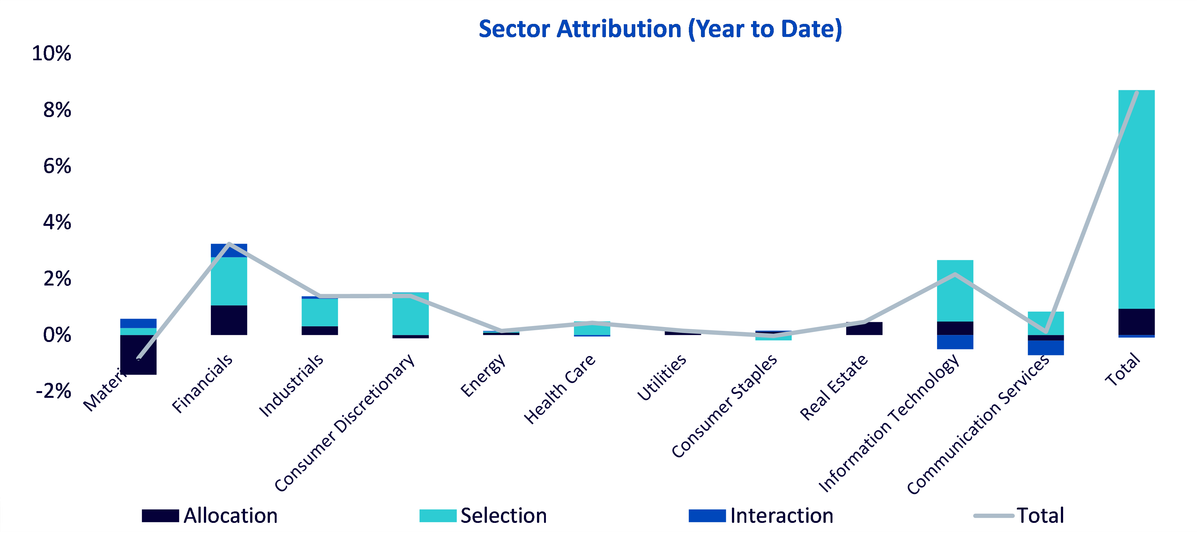

WisdomTree classifies export-oriented companies as those companies that derive at least 20% of their revenue from countries outside Japan. The higher stock selection in sectors such as financials, information technology, consumer discretionary and industrials played an important role in the 8.6% outperformance of the WisdomTree Japan Hedged Equity UCITS Index versus the MSCI Japan net Total Return Index Year to Date.

Source: FactSet, WisdomTree from 29 December 2023 to 29 November 2024. Historical performance is not an indication of future performance and any investments may go down in value.

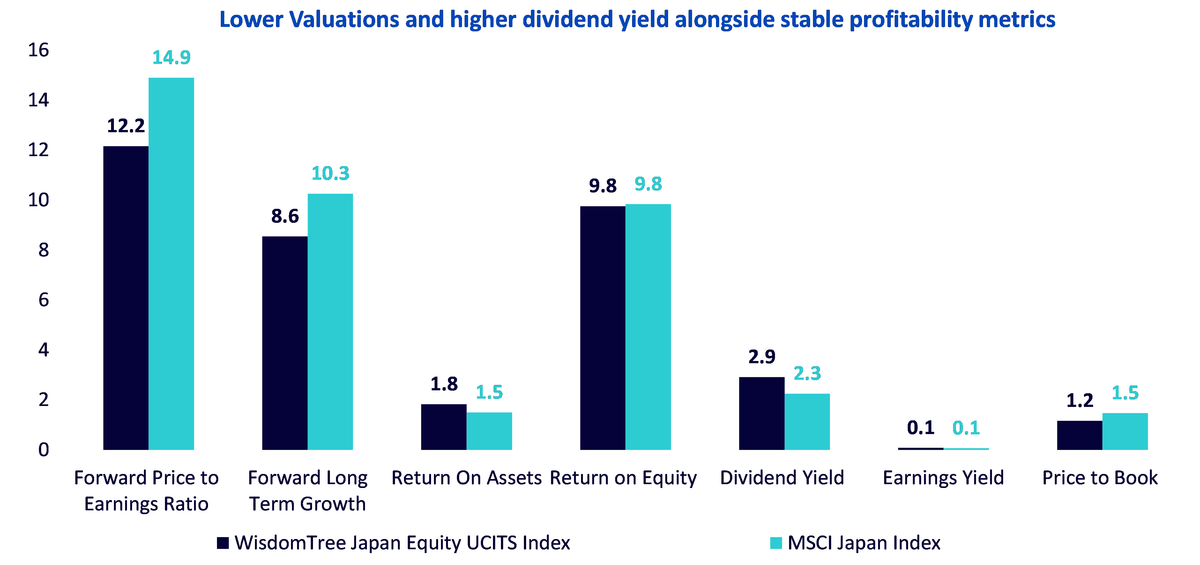

On comparing key fundamental metrics of the WisdomTree Japan Hedged Equity UCITS Index versus the MSCI Japan Dividend net Total Return Index we find the WisdomTree Japan Hedged Equity UCITS Index offers attractive value-based fundamentals via lower valuations alongside a higher dividend yield without compensating for quality metrics.

Source: FactSet, WisdomTree from 29 December 2023 to 29 November 2024. Historical performance is not an indication of future performance and any investments may go down in value.

1 Bloomberg as of 31 August 2024.

2 Japan Ministry of Finance.

3 Bloomberg as of 31 January 2023.

4 Yomiuri November 2024.

5 Bloomberg from 29 December 2023 to 12 December 2024.

6 FactSet, WisdomTree from 29 December 2023 to 31 October 2024.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.