WENT LN

WisdomTree Energy Transition Metals

Publié le 12 mars 2026

For most of the last decade, global supply chains were built for efficiency. The lowest cost won, inventory was minimised and commodity security was treated as a corporate procurement issue. That model is breaking down. Geopolitics is no longer a background risk. It is now shaping where mines get financed, where processing capacity gets built, and which projects get fast-tracked.

Strategic metals and critical minerals sit at the centre of this shift. They underpin electrification and digital infrastructure, but they also sit inside defence supply chains. In a more fragmented world, that combination matters. When policymakers look at rare earths, graphite, gallium or antimony, they are not thinking in commodity terms. They are thinking in terms of leverage, resilience and strategic autonomy.

Rare earth demand is often discussed through the lens of electric vehicles (EVs), but the story is broader. Wind turbines, industrial motors, robotics and a long list of consumer and industrial applications also pull on the same magnet materials. EVs and wind get most of the attention, but a wide range of other uses still account for a significant share of demand. That breadth matters because it means growth isn’t riding on a single end-market or a single policy lever. As electrification accelerates and data centres, automation and grid investment expand, the bigger issue shifts from whether demand rises to who can secure supply as it does.

That’s where geopolitics bites.

China dominates mined production, but the more important choke point is midstream capacity. In rare earths, the hard part is not simply digging up ore. It is processing, separating, refining, and then producing magnet-grade materials at consistent quality and scale. Those steps are capital intensive, technically complex, and environmentally sensitive. They also take years to replicate.

This concentration shows up clearly in refined supply: even as global rare earth refining has grown over recent years, the incremental volumes have remained heavily skewed toward China, with only a modest contribution from other regions. That matters because it’s the refined and separated material (not the ore) that feeds magnets and end-industries.

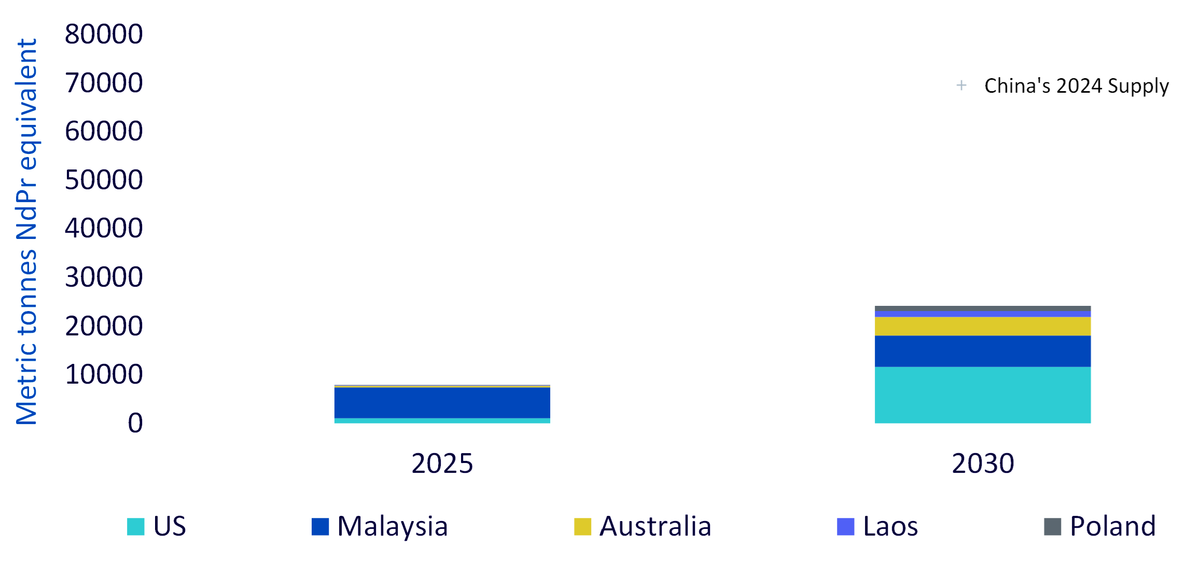

Source: BloombergNEF, WisdomTree as of 31 December 2025. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

That’s why the market’s focus has shifted from “reserves” to “control”. In a world where export licensing, trade policy, and industrial subsidies can move faster than new supply can be built, concentration becomes a policy variable rather than just an investment risk factor.

The recent pattern of Chinese export restrictions across strategic inputs highlights the point. These measures are often framed as licensing requirements rather than outright bans, but the practical impact is similar: approvals can be delayed, tightened, or redirected depending on policy priorities.

For manufacturers, it raises the risk of supply disruption and sudden price spikes. For investors, it increases the value of non-China assets that can credibly sit inside allied supply chains. For governments, it has accelerated a shift in posture: critical minerals are increasingly being treated like infrastructure.

The key change over the past year is that governments are moving beyond strategy papers into direct intervention. What stands out is how quickly the approach has shifted from simply incentivising projects to actively participating in them, through loans, long term offtake agreements and, in some cases, direct equity style exposure to ensure projects are developed and supply is secured.

In the US, the response is increasingly hands-on. Washington is now willing to underwrite capacity across the chain, not just at the mine mouth. That includes backing a domestic mine-to-magnet push (MP Materials1), financing downstream lithium conversion (Lithium Americas/Thacker Pass2), supporting rare earth separation capacity onshore (Lynas USA3 ), and taking a stake-plus-finance approach to newer entrants. Evidently, countering China’s dominance requires more than diversifying suppliers. It requires building parallel industrial systems, even if that means the government becoming a strategic shareholder and customer of last resort.

That urgency is also visible in the planned build-out of rare earth refining capacity outside China. New capacity is coming, but the near-term pipeline remains small relative to the scale of China’s existing supply, which highlights why policymakers view midstream capacity as a strategic vulnerability rather than a routine investment cycle. While capacity growth is underway, it is starting from a low base and takes time to compound.

That backdrop also explains the next step: Europe is now trying to tighten alignment with the US.

The latest development is that the European Union (EU) is preparing to propose a critical minerals partnership with the United States, explicitly aimed at curbing China’s influence over supply chains and reducing dependence on abundant, cheap Chinese minerals. The EU’s proposal would involve signing a memorandum of understanding and developing a “Strategic Partnership Roadmap” within three months4.

What’s notable is the breadth of the stated pillars. The plan is not just about signing up new mines. It is about cooperating to secure supply chains, deepening industrial and economic integration, and collaborating on research and innovation along the entire value chain.

In other words, Europe is trying to move the relationship from ad hoc project support to a coordinated framework that covers upstream, midstream, and technology. If it gains traction, it also strengthens the investment case for Western-aligned supply chains because it signals policy continuity across multiple major demand centres, not just one.

Greenland is a useful example of how geopolitics and geology are colliding. It sits in the Arctic corridor between North America and Europe, is politically tied to the Kingdom of Denmark, and has meaningful mineral potential. From a strategic perspective, it is one of the few places that can plausibly sit within a Western framework while offering exposure to minerals that have become politically sensitive.

Greenland also shows why supply cannot be “willed” into existence. Arctic operations are logistically difficult and costly. Environmental standards and community considerations are front and centre. Policy can evolve as the island weighs economic development against social and ecological priorities. That can slow timelines, but it also reinforces a key point: credible, high-quality jurisdictions can become strategically valuable precisely because they are hard to replicate.

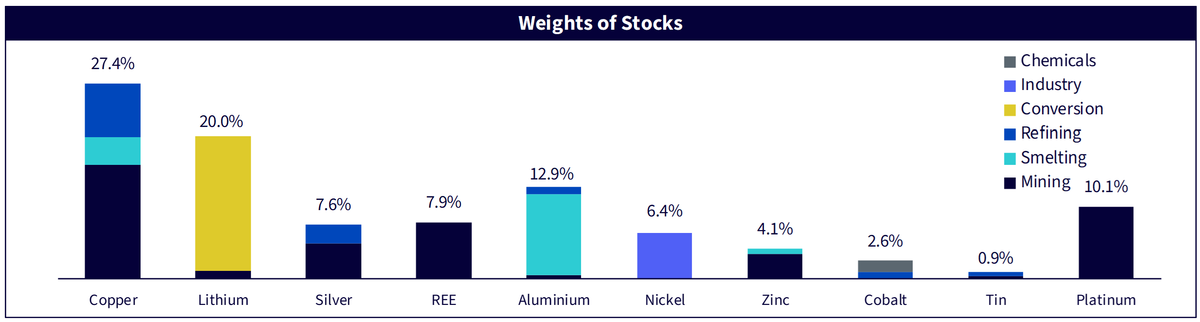

This policy pivot is also reframing the opportunity set for investors. Markets are increasingly valuing strategic metals and rare earths as enablers of the infrastructure for electrification, digitisation and defence. The WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF (Ticker: RARE) is designed to give targeted equity exposure to that shift by focusing on miners and related companies positioned across the strategic metals and rare earths ecosystem. The fund offers a way to express that theme through equities, capturing the upside from rising strategic urgency as well as structural demand growth across the energy transition and industrial electrification. The WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF seeks to track the price and yield performance of the WisdomTree Energy Transition Metals and Rare Earth Miners Index (Ticker: WTMRAREN).

The WisdomTree Energy Transition Metals and Rare Earth Miners Index is designed to identify globally listed companies from developed and emerging markets involved in the Energy Transition Metals Value Chain (ETMVC). Companies are mapped into ten metal categories: aluminium, cobalt, copper, lithium, nickel, platinum, silver, tin, zinc, and rare earth elements (REE) and across six mining subsectors such as mining, refining, smelting, chemicals, conversions and industry.

Source:WisdomTree as of 31 December 2025. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

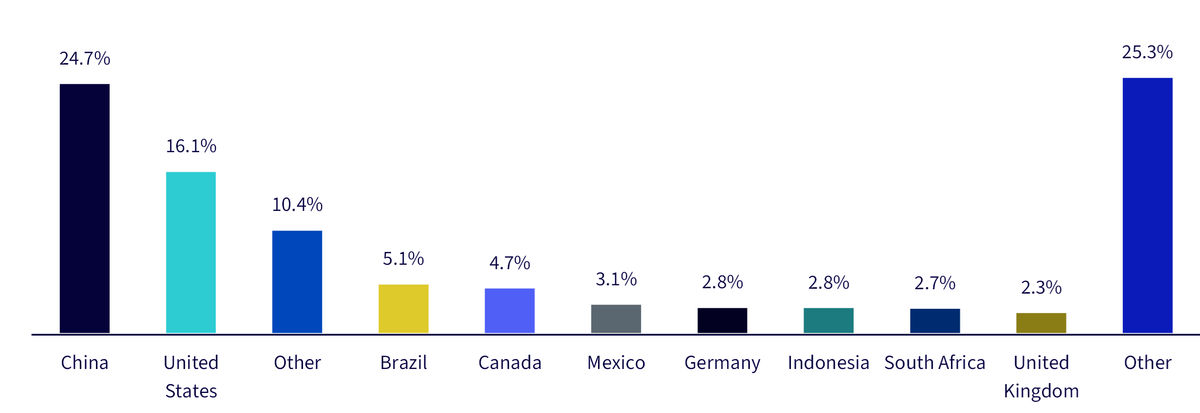

While China drives a significant share, the rest of the world, particularly the US, Australia, Canada, Europe, and select emerging markets, is accelerating REE development through projects and policy support. WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF offers diversified exposure across regions, with portfolio revenues spread across multiple geographies.

Source: WisdomTree as of 31 December 2025. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

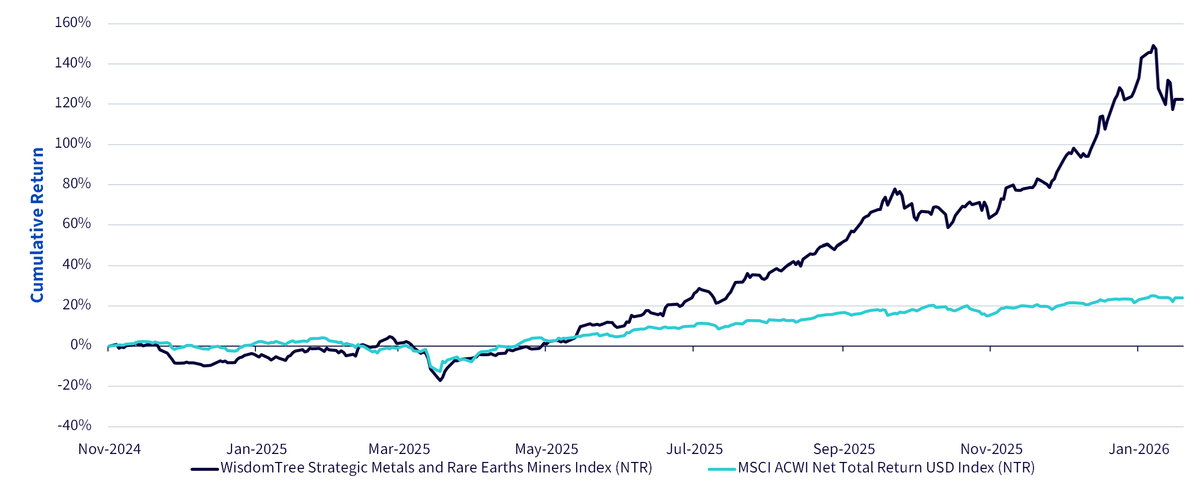

Since the start of the year, the WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF is up 14.94%5 outperforming the MSCI All Country World Index by 3.37%, underscoring the strength of the theme amid shifting macro and political currents.

Source: WisdomTree, Bloomberg. As of 9 February 2026. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

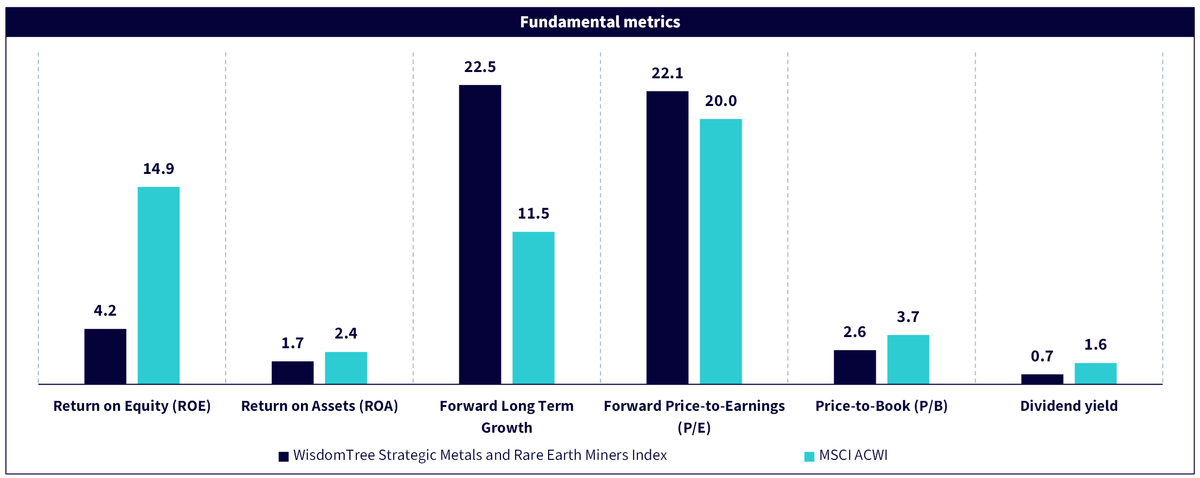

The WisdomTree Energy Transition Metals and Rare Earth Miners Index currently trades on a higher Price to Earnings ratio (P/E) of 22.1 and a lower price-to-book (P/B) ratio of 2.6x versus the MSCI All Country World Index, pointing to a mix of stronger growth expectations alongside a more asset-backed valuation profile. Looking ahead, consensus long-term earnings growth is materially higher at 22.5% for the WisdomTree Energy Transition Metals and Rare Earth Miners Index versus 11.5% for the MSCI All Country World Index.

Source: WisdomTree, FactSet, Bloomberg. As of 31 December 2025. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Geopolitics is no longer a temporary shock. It is becoming an organising principle for capital allocation in strategic resources. The EU’s push for a US partnership is the latest sign that Western economies are trying to coordinate their response not just to secure supply, but to reduce China’s ability to set the terms of trade. For investors, the implication is that strategic metals and rare earth miners are increasingly being priced through a security-of-supply lens, not just a commodity cycle.

1. MP Materials as of 10 July 2025

2. Bloomberg as of 1 October 2025

3. Reuters as of 27 August 2025

4. Bloomberg as of 3 February 2026

5. Bloomberg from 31 December 2025 to 6 February 2026

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.