WSLV LN

WisdomTree Core Physical Silver

Published 22 April 2025

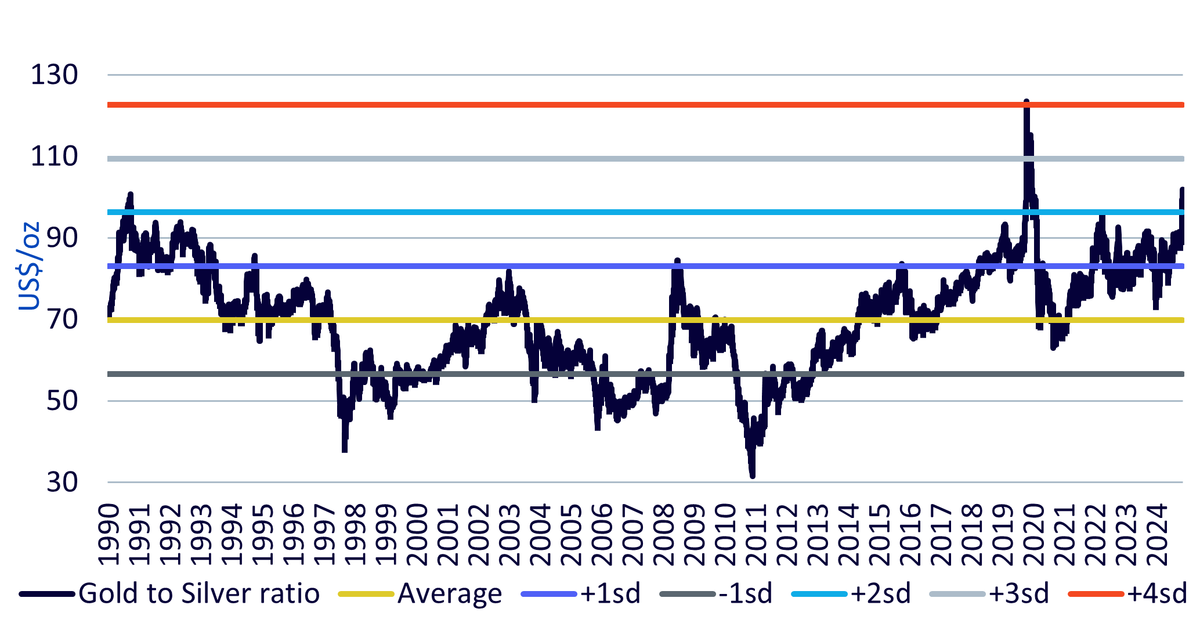

In Q1 2025, silver was outpacing gold. However, the geopolitical shift marked by "Liberation Day" (02 April 2025) reset the scales, allowing gold to overtake silver following a sharp correction. The gold-to-silver ratio has now exceeded 100 for the first time since the COVID-19 crisis of 2020—two standard deviations above the long-term average since 1990. Historically, such deviations have indicated strong catch-up potential for silver. For example, in 2020, silver prices rallied 94% between May and August, highlighting the scale of potential upside.

Source: WisdomTree, Bloomberg 01/06/1990 – 10/04/2025). Sd = standard deviation. Historical performance is not an indication of future performance and any investments may go down in value.

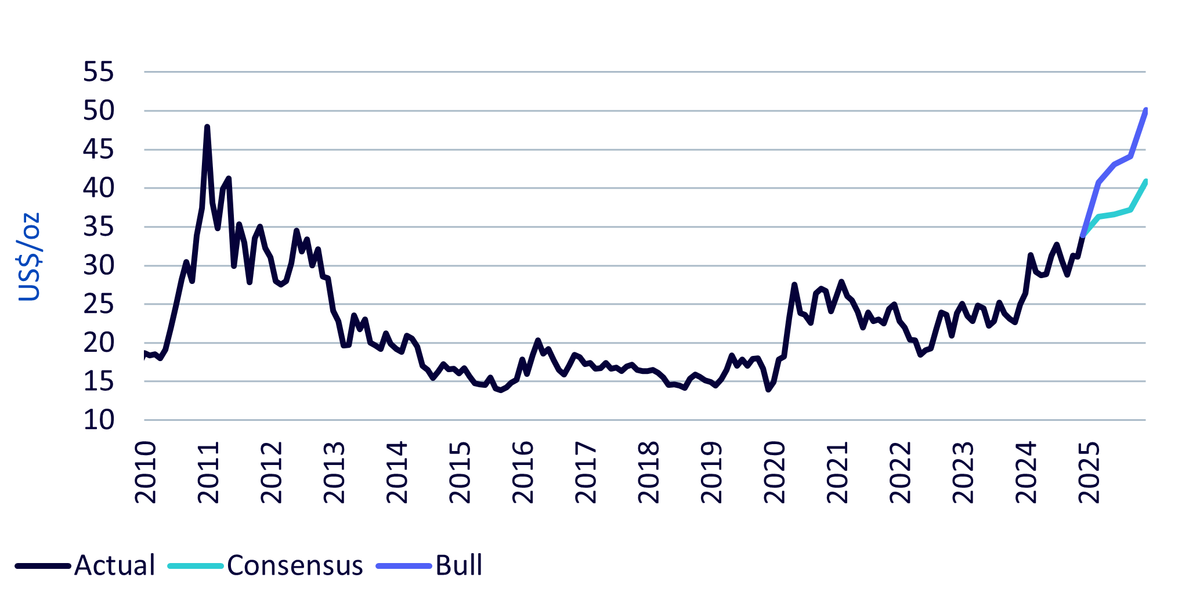

Following our recent gold forecast update to Q1 2026, we now present our silver outlook. Under the 'consensus' gold forecast scenario—which is based on prevailing views on the US dollar, Treasury yields, and inflation—silver prices could reach $40/oz. However, it's important to note that consensus macro forecasts were established prior to Liberation Day.

Under our 'bull' scenario for gold, which factors in a sharper depreciation of the dollar and elevated inflation, gold could exceed $4,000/oz. Holding all other assumptions in the silver model constant, this would imply silver prices could surpass $50/oz, marking a new all-time high1.

Source: WisdomTree (forecasts), Bloomberg (historic data). Historic: April 2010 to March 2025. Forecasts: April 2025 to March 2026. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

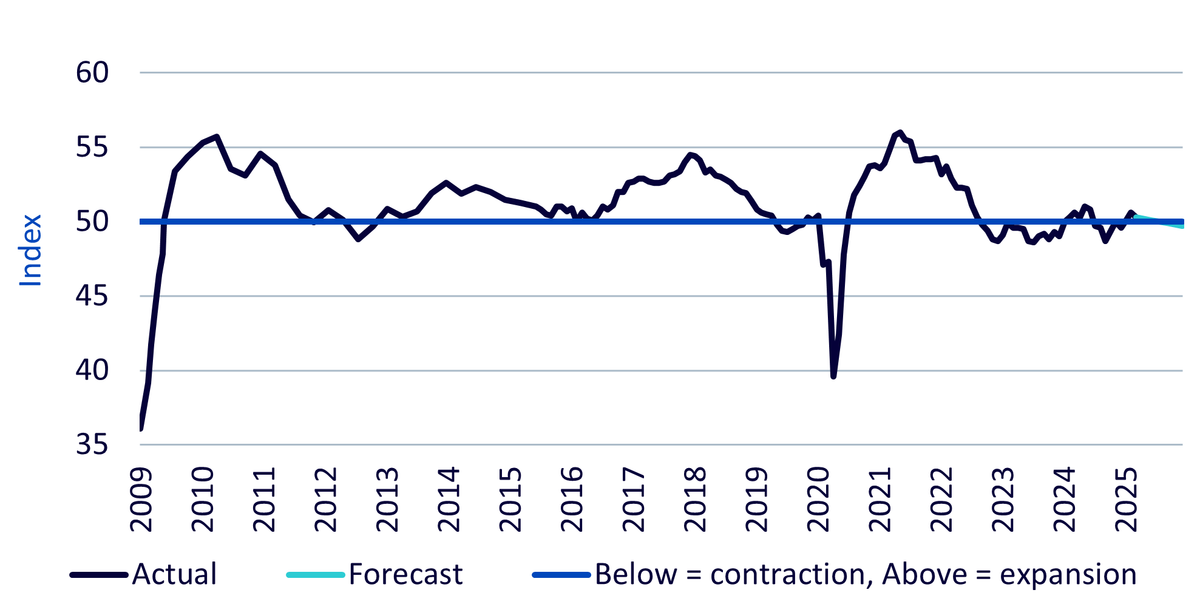

We anticipate that the ongoing trade war will lead to a contraction in industrial activity, with Global Manufacturing Purchasing Manager Indices (PMIs) likely to fall below the 50 mark, signalling contraction.

Source: WisdomTree, Bloomberg, S&P Global, Historic: January 2029 to March 2025. Forecasts: April 2025 to March 2026. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Despite overall industrial weakness, silver-specific demand is expected to remain resilient. This is largely due to strong photovoltaic (PV) demand, as China intensifies its energy transition efforts to stimulate domestic growth.

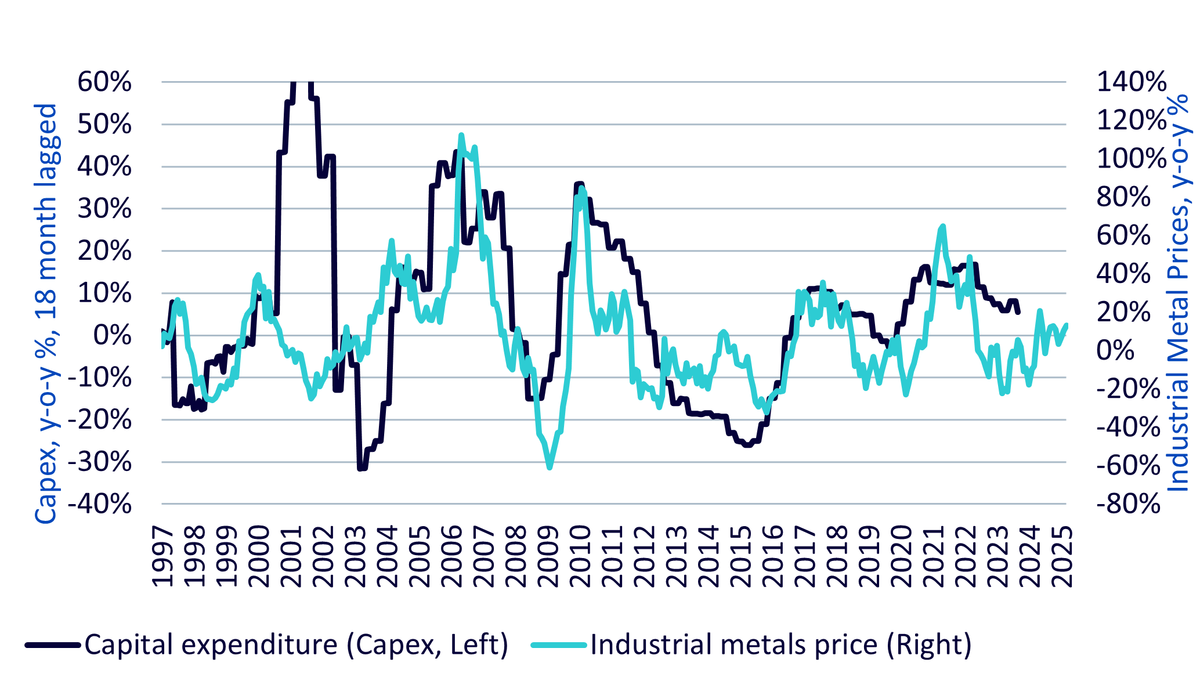

Mining capital expenditure has been slowing, reflecting past declines in industrial metal prices. Given the lag between CAPEX and production, we do not expect a near-term rise in supply. As a result, silver is likely to remain in a supply deficit for the fifth consecutive year in 2025.

Source: WisdomTree, Bloomberg, February 1996 to March 2025. Historical performance is not an indication of future performance and any investments may go down in value.

Silver appears primed for a significant rebound relative to gold, following a temporary loss in momentum after Liberation Day. As gold ascends to fresh highs, silver could test its previous peak and potentially exceed it, particularly under our bullish gold scenario.

For investors, this creates an asymmetric opportunity: silver remains undervalued on a relative basis and continues to benefit from robust demand fundamentals and constrained supply.

1 Previous high reached in April 2011 of $49/oz.

WisdomTree Core Physical Silver

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.