Commodity Outlook: Finding antivenoms in the Year of the Snake

Published 4 March 2025

Key Takeaways

- In the Year of the Snake, we are searching for antivenoms to counter the potential threats posed by trade wars, a strong US dollar, and a China that may be unable or unwilling to overcome its economic weakness.

- We see strong opportunities in gold, silver, aluminium, copper, zinc and European natural gas, as each of these has compelling drivers that could withstand broader headwinds in the commodity complex.

- As policies become clearer, we may find that our fears were overstated, potentially paving the way for a relief rally across the broader commodity complex. Until then, we place our confidence in these antivenoms.

- Related Products WisdomTree Core Physical Gold, WisdomTree Core Physical Silver, WisdomTree Aluminium, WisdomTree Copper, WisdomTree Zinc, WisdomTree European Natural Gas Find out more

We are about a month into the Chinese Year of the Snake. The preceding Year of the Dragon (10 February 2024 to 28 January 2025) brought significant momentum to the asset class with broad commodities rising 10%, precious metals rising 36%, industrial metals rising 12%, and even energy and agriculture mustering a late gain (close to 2% each)1. However, the Year of the Snake presents several macro challenges for commodities. Renewed trade protectionism from the US, under the new Trump Administration, is likely to dampen global trade. Additionally, higher bond yields and a strong US dollar create further headwinds for the commodities market. China’s reticence to stimulate big is also holding back the asset class.

Despite these headwinds, we have identified several micro factors that could provide support for certain commodities—what we refer to as our ‘antivenoms’. We remain optimistic about precious metals, aluminium, and European natural gas. Additionally, some of the macroeconomic challenges may ultimately prove less severe than initially anticipated, creating potential upside opportunities for commodities that currently reflect bearish sentiment.

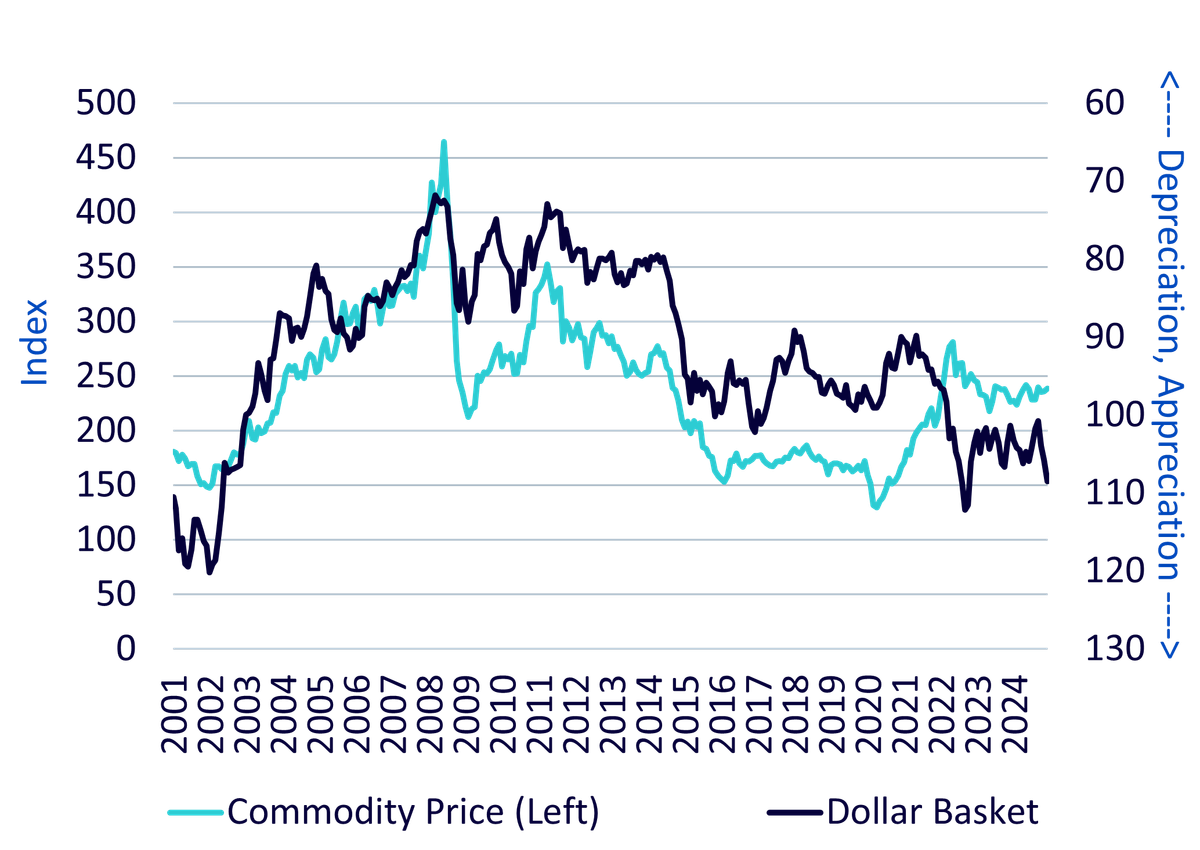

Strong US dollar

The recent strength of the US dollar has historically correlated with weaker commodity prices. While this pattern has been inconsistent post-COVID-19, the dollar's resurgence could once again pressure commodities. Historical data suggests a strong dollar often aligns with declining commodity values.

Figure 1: Commodities and US dollar

Source: WisdomTree, Bloomberg. 2001 to 2024. Commodity is Bloomberg Commodity Index Total Return. Historical performance is not an indication of future performance and any investments may go down in value.

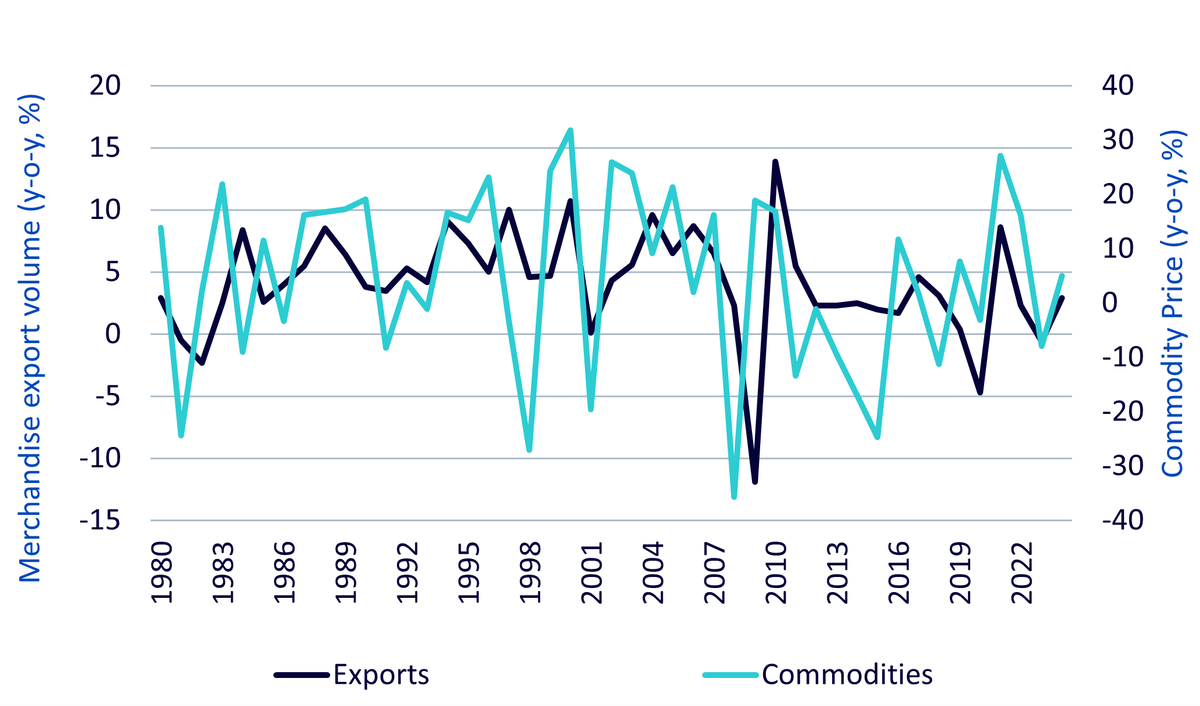

Trump’s trade policies and market impact

Donald Trump’s return to the presidency introduces uncertainty into trade and commodity markets. Trump's first presidency saw a trade war with China and other nations, negatively impacting global trade and commodity prices. While extreme tariff measures have often been bargaining tactics, the risk of real implementation remains. In his second term, some tariffs were announced and then delayed; at the time of writing, we still have no real guide as to whether they will be implemented or when. This uncertainty is already dampening market sentiment and increasing long-term interest rates, further constraining commodities.

Figure 2: Export volume and commodity price performance

Source: WisdomTree, Bloomberg. Commodity is Bloomberg Commodity Index Total Return. Historical performance is not an indication of future performance and any investments may go down in value.

Economic and inflationary concerns

Tariffs could raise inflation in the US while simultaneously depressing global commodity prices due to reduced demand. This dynamic may complicate the Federal Reserve’s (Fed) efforts to control inflation, potentially leading to prolonged high interest rates.

Climate policy reversals

Trump has vowed to withdraw from the Paris Climate Agreement and declared a “national energy emergency,” reversing climate regulations and boosting fossil fuel production. His administration is expected to cancel a $6 billion Department of Energy program aimed at industrial emissions reduction and repeal incentives for electric vehicles. These changes could suppress demand for critical materials used in clean technology, such as base metals.

At the same time, deregulation of oil, gas, and mining operations may increase the supply of key commodities like copper, aluminium, nickel, and cobalt. Major projects, such as Rio Tinto’s copper mine in Arizona, could proceed after years of delays. While immediate production increases are unlikely in 2025, long-term supply growth is possible.

Geopolitical risks and energy markets

A ceasefire between Israel and Hamas, brokered just before Trump's inauguration, has eased some geopolitical risk, though its stability remains uncertain. As we write, a peace deal between Russia and Ukraine is being brokered by the US. Short-term oil price spikes are possible if sanctions are initially tightened to get parties to the negotiating table but, ultimately, we could see easing oil and gas prices if a deal is hashed out.

The US has been pressuring Europe to purchase more American natural gas, but Russia’s LNG shipments to the EU remain significant. A resolution of the Russia-Ukraine war could weaken US leverage in energy negotiations, making Europe less dependent on American gas.

Stricter enforcement of Iranian oil sanctions under Trump could drive oil prices higher. However, OPEC2 members may counteract this by increasing supply, potentially offsetting price gains.

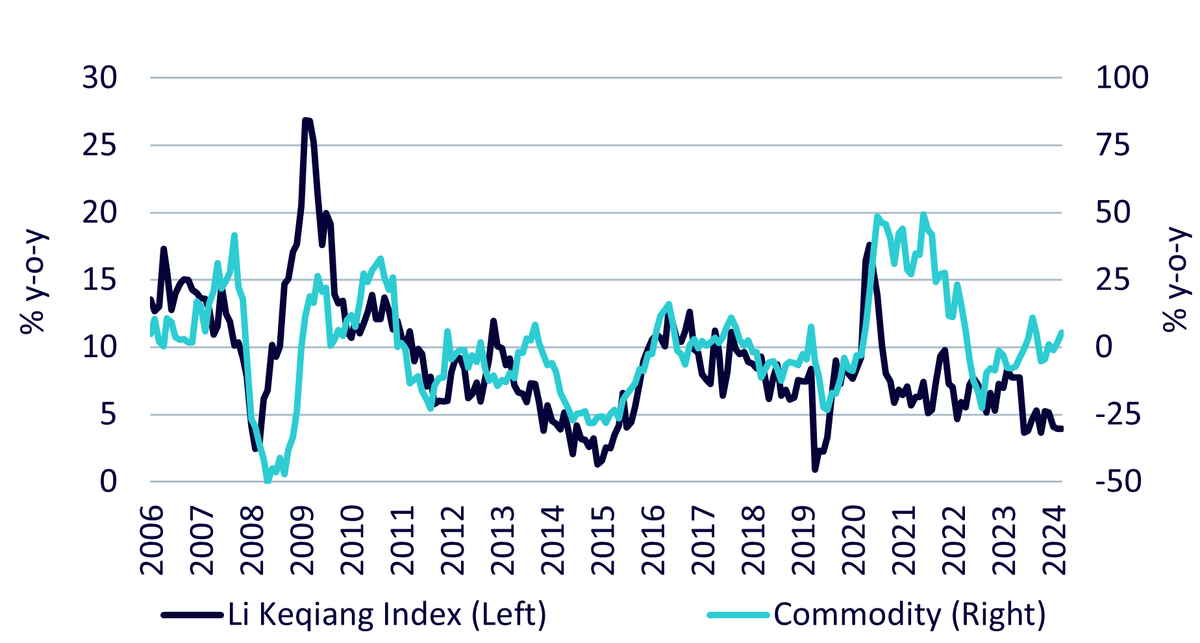

China’s economic strategy and commodity demand

China remains the world’s largest consumer of commodities, yet its recent economic weakness has limited demand growth. Unlike previous economic cycles where China launched large stimulus measures, its current approach focuses on smaller, targeted interventions. The government has stabilised the real estate sector but remains wary of excessive stimulus due to debt concerns.

China is investing heavily in clean technology and renewable energy infrastructure, supporting metal prices despite weak real estate demand. US tariffs on China could accelerate its push toward energy independence, promoting domestic adoption of solar, battery, and electric vehicle technologies.

Trade tensions could escalate into retaliatory actions, such as China restricting exports of critical materials, as seen with gallium, germanium, and graphite in response to semiconductor disputes. Further restrictions could impact global supply chains for energy transition materials.

China’s depreciating Yuan complicates economic policy. The People’s Bank of China has been intervening to stabilise the currency, limiting its ability to cut interest rates. While a policy shift to boost growth led to short-term market gains in 2024, further action remains constrained by currency pressures.

Figure 3: Li Keqiang Index and commodity prices

Source: WisdomTree, Bloomberg. January 2005 – December 2024. Li Keqiang index: 40% outstanding bank loans, 40% electricity production, 20% rail freight volume. Commodity is Bloomberg Commodity Index Total Return. Historical performance is not an indication of future performance and any investments may go down in value.

WisdomTree’s antivenoms

Outlook | |

|---|---|

Gold | Gold is scaling all-time highs as uncertainty is driving demand for the safe haven asset higher. Threats of rising inflation and potential economic instability from tariffs are further positive. Central bank demand remains extremely elevated and does not show signs of cooling. Our forecast for gold indicates further upside at $3,070/oz at the end of this year. For more see: Gold Outlook to Q4 2025 |

Silver | Silver has a high correlation with gold (close to 80%). Silver is due a catch up with gold’s outperformance. Industrial demand for silver is at record highs despite a lacklustre general manufacturing environment. Photovoltaics demand for silver is rising with higher installation and higher volumes of silver per installation. Silver is in a supply deficit. Silver currently is not considered a critical raw material but has potential under the new US Administration as frameworks are reevaluated. For more see: Silver Outlook to Q4 2025 |

Aluminium | Aluminium is heading for a multi-year production deficit. China, the world’s largest producer of aluminium, has a government-imposed production cap of 45 million tonnes per year and is close it now. China has cancelled rebates on exports, significantly dampening the incentive to export. Rising copper prices have driven aluminium demand higher in transmission and distribution cabling. Aluminium production outside China is also expected to remain limited in 2025. |

Copper | After being in surplus in 2024, copper is heading for a production deficit in 2025. Miners have reduced their production guidance, while industrial demand likely to grow. Electrification and energy transition uses are a key driver of demand growth. China’s spending on grid infrastructure is at all-time highs. Grid infrastructure is copper (and aluminium) intensive. |

Zinc | We had a significant production deficit in zinc in 2024 and that is likely to continue into 2025 before easing in 2026. Zinc production capacity has been constrained, and price signals have not been strong enough to drive speed in upgrades. |

European Natural Gas | A colder winter has drawn down European natural gas storage to below average and significantly below 2023 and 2024 levels (the relevant benchmarks given higher storage dependency after the Ukraine war). Mandated fill levels have ironically removed the incentive to put more gas in storage as summer 2025 prices are higher than winter 2026 (backwardation in futures curve). That backwardation in futures is a performance enhancer for rolling futures strategies. For more see: European natural gas is the hottest energy commodity so far this year |

Gold is scaling all-time highs as uncertainty is driving demand for the safe haven asset higher.

Threats of rising inflation and potential economic instability from tariffs are further positive.

Central bank demand remains extremely elevated and does not show signs of cooling.

Our forecast for gold indicates further upside at $3,070/oz at the end of this year.

For more see: Gold Outlook to Q4 2025

Silver has a high correlation with gold (close to 80%).

Silver is due a catch up with gold’s outperformance.

Industrial demand for silver is at record highs despite a lacklustre general manufacturing environment.

Photovoltaics demand for silver is rising with higher installation and higher volumes of silver per installation.

Silver is in a supply deficit.

Silver currently is not considered a critical raw material but has potential under the new US Administration as frameworks are reevaluated.

For more see: Silver Outlook to Q4 2025

Aluminium is heading for a multi-year production deficit.

China, the world’s largest producer of aluminium, has a government-imposed production cap of 45 million tonnes per year and is close it now.

China has cancelled rebates on exports, significantly dampening the incentive to export.

Rising copper prices have driven aluminium demand higher in transmission and distribution cabling.

Aluminium production outside China is also expected to remain limited in 2025.

After being in surplus in 2024, copper is heading for a production deficit in 2025.

Miners have reduced their production guidance, while industrial demand likely to grow.

Electrification and energy transition uses are a key driver of demand growth.

China’s spending on grid infrastructure is at all-time highs. Grid infrastructure is copper (and aluminium) intensive.

We had a significant production deficit in zinc in 2024 and that is likely to continue into 2025 before easing in 2026.

Zinc production capacity has been constrained, and price signals have not been strong enough to drive speed in upgrades.

A colder winter has drawn down European natural gas storage to below average and significantly below 2023 and 2024 levels (the relevant benchmarks given higher storage dependency after the Ukraine war).

Mandated fill levels have ironically removed the incentive to put more gas in storage as summer 2025 prices are higher than winter 2026 (backwardation in futures curve).

That backwardation in futures is a performance enhancer for rolling futures strategies.

For more see: European natural gas is the hottest energy commodity so far this year

Conclusion

In the Year of the Snake, we are searching for antivenoms to counter the potential threats posed by trade wars, a strong US dollar, and a China that may be unable or unwilling to overcome its economic weakness.

We see strong opportunities in gold, silver, aluminium, copper, zinc and European natural gas, as each of these has compelling drivers that could withstand broader headwinds in the commodity complex.

As policies become clearer, we may find that our fears were overstated, potentially paving the way for a relief rally across the broader commodity complex. Until then, we place our confidence in these antivenoms.

For WisdomTree’s full Market Outlook, please click here.

1 Source: Bloomberg, 10 February 2024 to 28 January 2025, using Bloomberg Total Return Indices.

2 Organization of the Petroleum Exporting Countries.

About the contributor

Nitesh Shah

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.