An Inflationary Mulligan Stew

Published 24 May 2021

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Treasury Secretary Janet Yellen seemed to forget for a moment that she was in a new role, one that does not set monetary policy. Against that backdrop, let’s just say Secretary Yellen got her first mulligan1.

As a reminder, Yellen said that “it may be that interest rates will have to rise somewhat to make sure our economy doesn’t overheat”2, but quickly pivoted away from that statement later on. The premise of Secretary Yellen’s initial comment came from being asked if the current, and proposed, spending from the Biden Administration could create a setting where inflation may need to be reined in.

There is no question the inflation debate is currently gaining momentum in the markets, specifically the fixed income arena. Is inflation looming on the horizon, and will any potential increase prove to be ‘transitory’ as the Federal Reserve (the Fed) believes, or will it be more sustainable? At this stage, there appears to be four undeniable factors that should push inflation higher in the months ahead:

- Base effects, i.e. year-over-year readings will be compared to very low readings from 2020

- Higher commodity prices

- Disruptions in supply chains and low inventories

- Pent-up demand from Covid-related reopening’s

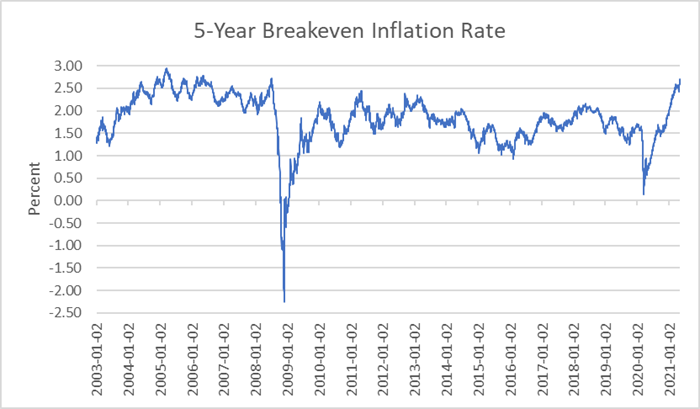

Source: St. Louis Fed, as of 5/7/2021

Historical performance is not an indication of future performance and any investments may go down in value.

So, who is right in this inflation debate? I like to take my cues from the bond market, and as you can see, inflation expectations have been on a rather visible ascending trajectory. Looking at Treasury 5-year breakeven spreads, the latest reading of roughly 2.70% has now gone back into a territory that is rarely visited…in other words between 2.50% to 3.00% In fact, as of writing this, the last time the breakeven rate was this high you have to go back to the pre-financial crisis days of 2006.

1 Mulligan is a golf term for: getting an extra stroke after a poor shot but it’s not counted. The broader meaning is one getting a ‘do-over’.

2 Source: CNBC as of 4 May 2021

Related articles

The world's biggest market is hiding in plain sight

Equity Outlook catching the tailwinds respecting the headwinds

How the Iran War Is Reshaping the Macro Outlook

Rolls-Royce, Safran, and Airbus at the centre of Europe’s defence tech future

Inside the WisdomTree Strategic Metals and Rare Earths Miners Index rebalance

What’s Hot: What if Greenland risks were to re-escalate?

Steel, sensors, and speed: powering Europe’s deterrence

From Gripens to Goshawks: The drone-driven reinvention of European defence

Why the Magnificent 7 are still magnificent

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.