DXJ LN

WisdomTree Japan Equity UCITS ETF - USD Hedged

Published 16 March 2026

The global economy entered 2026 in a comparatively supportive backdrop for equities: growth expectations stabilised, inflation anxiety eased and earnings stayed resilient. The global backdrop is shifting toward a form of modern mercantilism, a more adversarial multipolar system where trade, technology and security are increasingly negotiated as part of a broader strategic bargain.

Q1 2026 has reinforced the same message. Markets have become more selective and more rotational. Artificial intelligence (AI) is still a structural theme, but equity performance is increasingly driven by dispersion across regions, sectors and styles, rather than a single index trade. The shifting pattern of global equity market performance in 2025 is a useful precursor, reminding us that return dispersion across regions is likely to remain a defining feature of 2026.

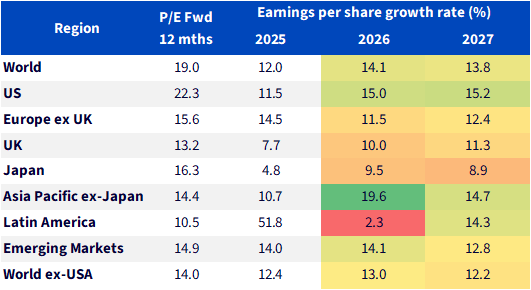

Source: MSCI, FactSet, WisdomTree as of 31 December 2025. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

The US continues to set the tone for global risk appetite, but the internal market structure has become more important than the headline index. The defining shift is that the market is no longer rewarding ‘AI exposure’ in a blanket way. It is differentiating between AI enablers with clear earnings visibility and mega-cap growth, where expectations were already stretched. That matters because concentration remains a first-order risk. By late 2025, the top 10 names were roughly 40% of S&P 500 market capitalisation, amplifying index sensitivity to a small set of stocks and raising the probability of volatility even when the median company is behaving normally. This is one reason Q1 2026 has felt ‘two-speed’: the index can hold up, but leadership can rotate sharply underneath.

US equities can still do well, but the market is less forgiving. A high valuation and concentration backdrop raises the hurdle for another straightforward year of multiple expansion. The more robust approach is to lean into breadth: balance-sheet strength, cash-flow durability, and selectively cyclical earnings where pricing power and order visibility can carry through softer patches.

One of the most useful frames for what we’ve seen so far in 2026 is the HALO effect: Heavy Assets, Low Obsolescence. It captures the market’s growing preference for capital-intensive businesses tied to capacity, networks, infrastructure and engineering complexity, areas where assets ‘age’ slowly, pricing is often supported by long-cycle demand, and competitive moats are physical rather than digital.

This matters because the AI cycle is increasingly a real-economy buildout: data centres, power delivery, cooling and grid investment. As investors become more valuation-sensitive around US tech, they’ve been more willing to pay for the ‘picks-and-shovels’ layer of AI and electrification. In other words, HALO is a mechanism that helps explain why leadership can broaden even when the AI narrative remains intact.

Europe entered 2026 pulled in two directions: external pressures (tariffs, currency strength, competition) versus more constructive internal forces, easier monetary conditions, a clearer fiscal turn, and gradual progress in structural reforms. The base case in the original outlook was that domestic forces would increasingly matter for earnings confidence, and Q1 has been broadly consistent with that. Europe’s opportunity set looks more balanced than it has for much of the last decade. Europe also benefits from less concentration risk than the US, which becomes more valuable when dispersion rises.

On reform, progress is real but incomplete. The European Policy Innovation Council’s (EPIC) tracking shows that only about 11% of Draghi’s recommendations have been fully implemented, and a further 20% partially implemented, highlighting both upside (if delivery accelerates) and constraints (from political bottlenecks).

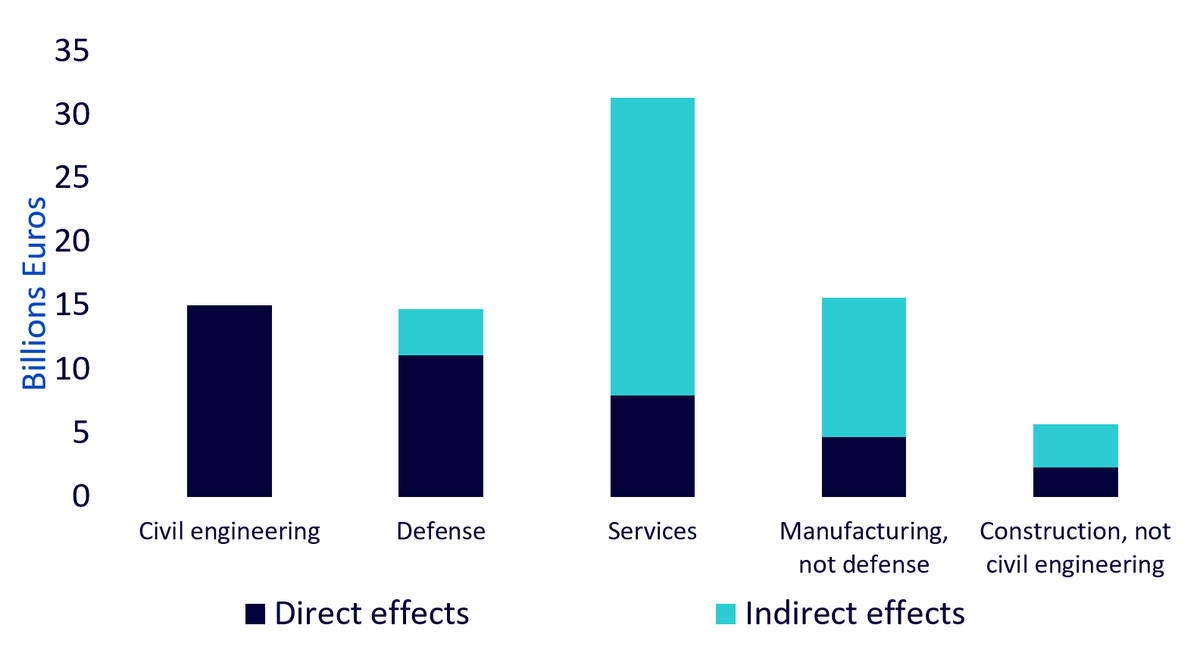

Europe’s push for strategic autonomy is increasingly evident in fiscal policy. Defence spending is a key component, but the more investable implication is broader: industrial capacity, infrastructure, digitisation and innovation. Germany is central here. We expect the additional fiscal spending following the relaxation of Germany’s constitutional debt brake could add roughly 0.4% to German growth in both 2026 and 2027, even with near-term bottlenecks such as approvals and labour constraints. The spillover potential is meaningful. Germany is a key trading partner for much of the region, and a turn from stagnation towards modest growth can lift confidence and spending beyond its borders.

Source: Destatis, WisdomTree as of 31 January 2026. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

The UK equity investment case is still differentiated. Less about growth leadership and more about income, valuation support and rate sensitivity. The outlook argues that easier monetary policy can support areas like life assurance, property and construction, where starting valuations are depressed and dividend yields can compensate for uncertainty.

While the UK case is anchored in dividends and valuation support, Japan offers a different kind of appeal: a reform story that is becoming more embedded, supported by governance pressure and a clearer domestic policy direction.

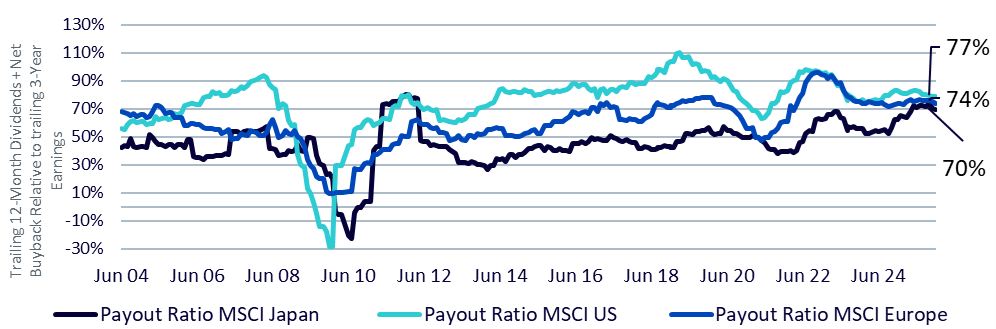

Japan remains one of the more consistent structural stories in developed markets. It reflects a rare combination of policy clarity and governance momentum. Prime Minister Sanae Takaichi’s success in the snap elections and the backdrop of the new growth strategy remain key tailwinds. And governance matters. The Tokyo Stock Exchange’s push on cost of capital and valuation has accelerated corporate actions: higher disclosure, fewer sub-book stocks, and rising buybacks, all of which support breadth.

Source: FactSet, WisdomTree as of 31 January 2026. Historical performance is not an indication of future performance, and any investments may go down in value.

The emerging markets (EM) message is constructive but nuanced: macro conditions can help, but outcomes hinge on country selection and earnings durability through the AI and commodity cycles. The framework remains supportive, with an EM growth premium, easing inflation, improving earnings revisions and stronger external positions helping reduce macro risk premia.

The tailwinds remain in place, supported by resilient earnings and a constructive global backdrop. But the crosswinds are real, including policy uncertainty, geopolitics and a US market structure that remains concentrated and valuation sensitive. In that environment, diversification becomes more than risk control. It becomes a source of returns. Positioning for broader leadership, including the Q1-visible HALO rotation toward capital-intensive sectors with durable cash flows, may prove the most resilient strategy.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.