DES

U.S. SmallCap Dividend Fund

Published September 4, 2025

Head of Equity Strategy

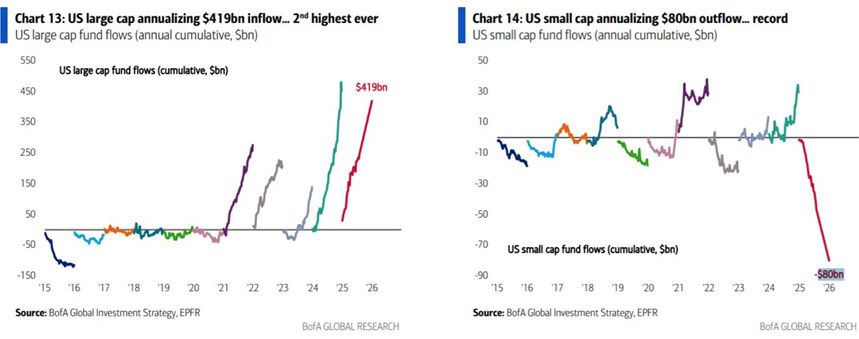

The house of pain continues with small caps, at least on a relative basis. Year-to-date, the S&P 600 index has posted a 3.0% gain, so it's not like money is being burned. But still, even the Bloomberg Aggregate Bond index is up 4.9% YTD and the S&P 500 is up 10.9%.1

BofA's fund flow data tells a thousand words.

Figure 1: A Tale of Two Asset Classes

Source: BofA Global Research, July 2025.

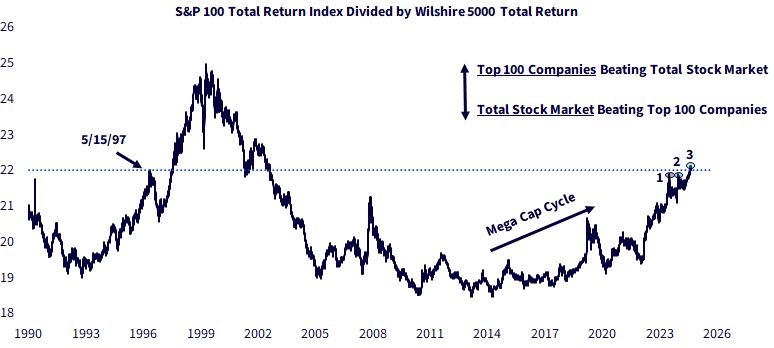

We're at a moment of truth with large versus small, too. When I plot the S&P 100 relative to the big, broad Wilshire 5000 index, it is making its third attempt at resistance levels that date to the 1990s. If recent action holds, this would mark an important breakout for large caps.

Figure 2: AMoment of Truth

Source: Refinitiv, total return indexes, as of 8/21/25.

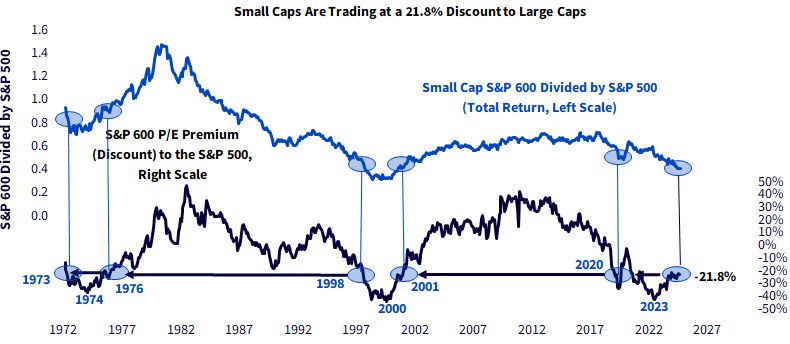

Because of small caps' multi-year struggle, the group is trading at a 21.8% discount to large caps on reported earnings (figure 3). It doesn't mean a small-cap resurgence will start tomorrow, but I do find solace in these valuation gaps resembling the situation that manifested in both the mid-1970s and the turn of the century.

Source: Refinitiv, DataStream reported earnings calculations, 12/31/1972–7/21/2025.

Small caps are cheap, at least relatively, but there is a potential 2026 headwind that we should address.

The S&P 600 index of small caps has an easy hurdle this calendar year, in that the Street is penciling in earnings growth of just 2.7% to the S&P 500's 7.4%, according to Yardeni Research. But for next year, the Street has S&P 600 earnings jumping another 18.8% (the S&P 500 is expected to see earnings growth of 13.9%). Those will probably both be revised down, as usual, but it's still an easier hurdle for large caps than small caps.

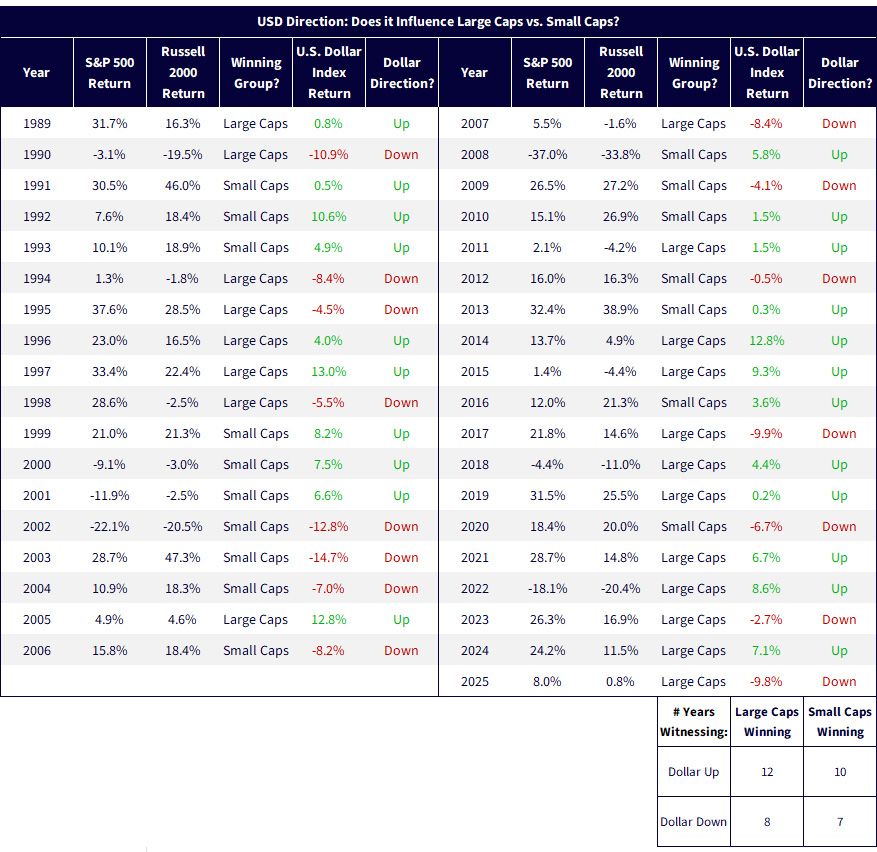

As for the Dollar

It's one of the most common questions we get on large versus small. I wish I had some strong view here, but I don't. The problem with the dollar is you must get two things correct to make money:

It's easier said than done, as I think figure 4 makes clear. Even if you accurately predict the dollar, good luck making heads or tails out of large and small because of it.

Figure 4: Predicting This Stuff Isn't Easy

Source: Refinitiv, total return indexes, as of 7/30/25.

I have given the "dollar vs. cap size" concept a ton of thought over the years.

The common refrain goes something like this: "If the dollar rises, that is going to be bad for big U.S. multinationals, because their costs will be in expensive dollars and their customers will pay them in weak euros and weak yen. Therefore, if I'm bullish the dollar, I should go for small caps."

If it were only that simple. Dollar up, give me small caps. Everyone knows that. But it isn't necessarily true.

How about if "dollar up" is happening because some hedge fund is blowing up or a banking institution is dying in real time? In those markets, people are doing wild things like getting diamonds into Swiss safe deposit boxes, emptying ATMs and so on. In that world, where the grab for dollars is on, you probably aren't going to be happy with small caps.

Moral of the story: like small caps because you like small caps, not because of any U.S. dollar forecast that is on your mind.

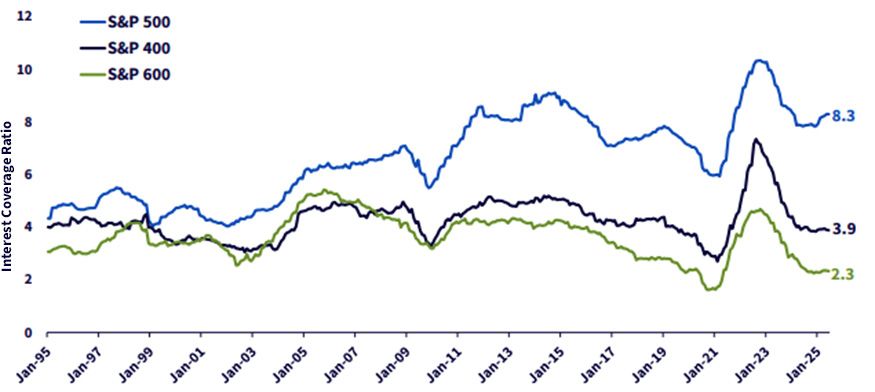

Now…that doesn't mean you can't engage in some old-fashioned Fed Kremlinology. That work could help small caps because of a narrative that figure 5 lays out. It shows a concept that is intuitive: as a collective, large caps tend to stand on sturdier balance sheet ground than small caps. Interest coverage (earnings before interest and taxes divided by interest expense) is a notably different scene as you move across the cap spectrum.

Figure 5: Interest Coverage Ratio

Source: WisdomTree, as of July 2025.

If the Fed starts cutting rates, that helps not only people and companies with large debt burdens, but also those who are more likely to have floating rate obligations. Both of those descriptors apply more to small caps than large caps. It's something to consider if the Fed starts easing policy.

If you like the charts in this blog post, be sure to check out our new Daily Charts, which features timely charts from various WisdomTree thought leaders.

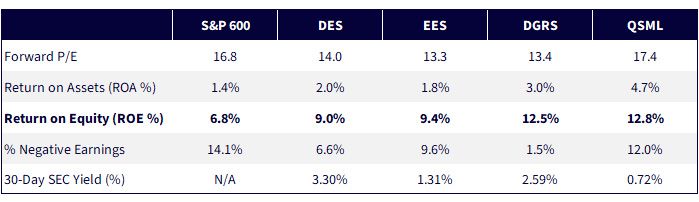

Figure 6 sorts our four U.S. small-cap Funds by quality (return on equity).

Figure 6: U.S. Small-Cap Fundamentals

Source: WisdomTree PATH software, as of 7/31/25. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the respective ticker: DES, EES, DGRS, QSML.

Funds mentioned in figure 6:

1 Performance figures from WisdomTree's PATH software, as of 8/27/25.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Head of Equity Strategy

Jeff Weniger, CFA, has been with WisdomTree since 2017 and serves as the Head of Equities. He shapes the firm’s market outlook through a combination of macroeconomic and fundamental analysis. With more than two decades in investment strategy, Jeff is known for his work on market cycles and valuations. Before joining WisdomTree, Jeff was with BMO Private Bank and BMO Global Asset Management for 11 years. At BMO, he sat on the firm’s Asset Allocation Committee and co-managed ETF model portfolios across the U.S. and Canada. In 2013, at age 32, he became the youngest member of BMO’s Global Investment Forum. When he left BMO to come to WisdomTree, his final role was Director, Senior Strategist in the Office of the CIO in 2017.

Jeff is a frequent television guest on networks such as CNBC, Bloomberg, and Schwab, with regular print appearances in The Wall Street Journal, Barron’s and Reuters. He also appears weekly on the Behind the Markets podcast and is a regular on SiriusXM’s The Business Briefing. On X, Jeff has developed one of the larger followings in financial media. He earned a B.S. in Finance from the University of Florida and an MBA from the University of Notre Dame. He has held the CFA charter since 2006.