DON

U.S. MidCap Dividend Fund

Published January 22, 2025

Research Analyst

Large-cap stocks have outperformed mid- and small caps for the last decade. The emergence of various cleverly named groups of market leaders over the years shows that large companies, particularly tech-enabled growthy ones, have done particularly well in recent times.

Since 2012, the S&P 500 Index returned 13%, compared to the S&P MidCap 400's and S&P SmallCap 600's respective returns of 9.63% and 9.15%. With recent market rallies often being led by FAANGs, then MAANGs, then Magnificent Sevens, etc., mid- and small-cap stocks—value stocks in particular—are often overlooked by investors in favor of larger and more glamorous names.

Those investors may be surprised to find out that, over a longer period, mid- and small-cap (also referred to as SMID) stock baskets handily beat large-cap baskets.

In fact, the smallest value stocks beat the largest growth stocks by more than 6% on average since the Great Depression, as seen in figure 1.

Sources: WisdomTree, Kenneth French Data Library. Universe is all NYSE, AMEX and NASDAQ stocks. Size segment = market capitalization. Returns are average annual returns. Past performance is not indicative of future returns.

Many investors allocate to SMIDs for growth potential. Yet the small-cap growth category had some of the weakest returns. Often, these companies are too expensive and unprofitable—having to issue shares to stay alive.

How would an investor go about selecting value stocks? There are myriad metrics to choose from, including price-to-earnings, price-to-cash flow, price-to-book and more. We believe a dividend approach is an effective strategy for value investing within the SMID universe.

Allocations to dividend-paying small-cap and mid-cap securities help investors avoid common pitfalls associated with value investing. Companies often distribute earnings to shareholders in the form of dividends to demonstrate financial stability and confidence in future earnings, as well as to make their shares more attractive to current and prospective investors.

WisdomTree not only screens for dividends but also applies some risk controls focused on profitability to help filter out value traps.

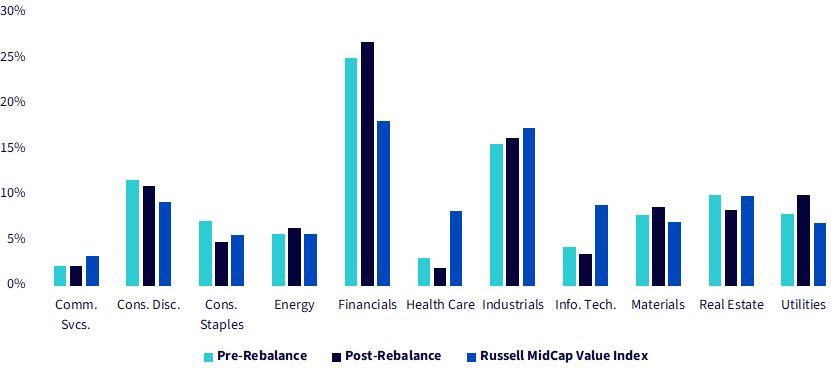

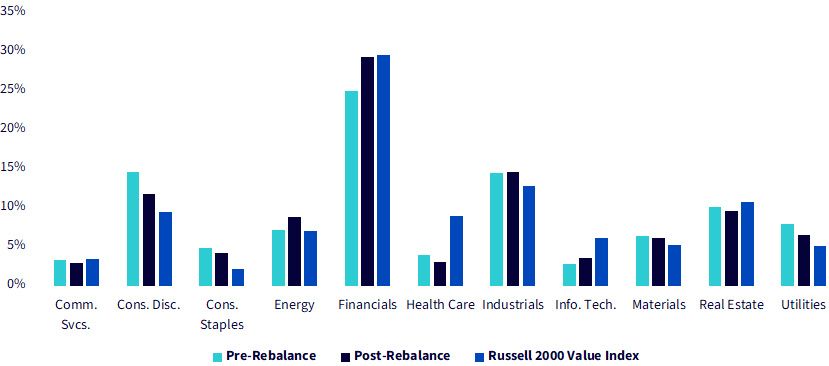

The Indexes tracked by the WisdomTree U.S. MidCap Dividend Fund (DON) and the WisdomTree U.S. SmallCap Dividend Fund (DES) underwent their annual reconstitutions earlier last December.

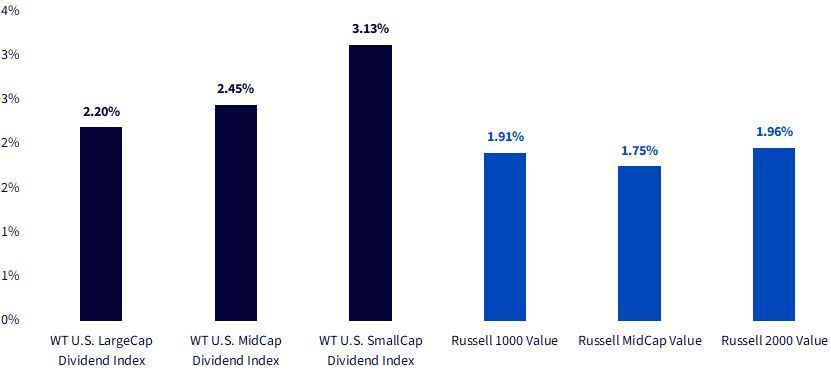

By isolating dividend payers, these Indexes have higher dividend yields than their benchmarks, as demonstrated in figure 2. These Indexes' post-rebalance baskets even had higher dividend yields than their large-cap counterpart, the WisdomTree U.S. LargeCap Dividend Index.

Sources: WisdomTree, FactSet, FTSE Russell. Benchmark data as of 11/30/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

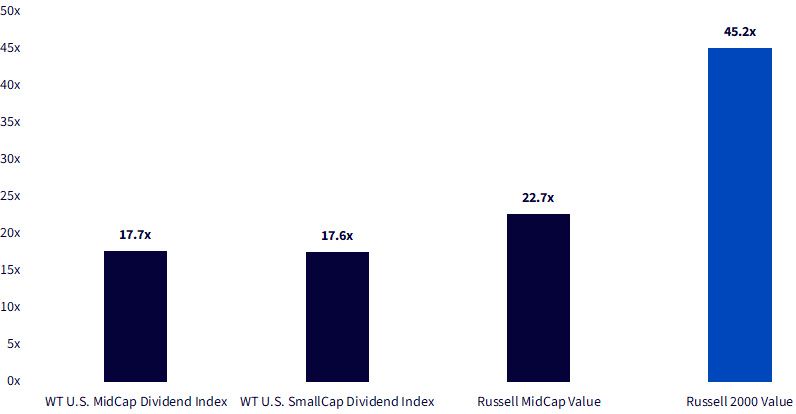

As seen in figure 3, the post-rebalance price-to-earnings ratios for the WisdomTree U.S. MidCap Dividend and SmallCap Dividend Indexes remain at discounts to their Russell Value benchmarks, especially for the SmallCap Dividend Index.

With inflation expectations remaining high, value stocks exhibiting quality characteristics such as profitability in defensive sectors like consumer staples, utilities and health care are expected to show resilience.

These stocks are likely to weather high interest rates better than their growth counterparts should the Federal Reserve pursue hikes in 2025.

Sources: WisdomTree, FactSet, FTSE Russell. Benchmark data as of 11/30/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

Sources: WisdomTree, FactSet, FTSE Russell. Benchmark data as of 11/30/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

Sources: WisdomTree, FactSet, FTSE Russell. Benchmark data as of 11/30/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

Sources: WisdomTree, FactSet, FTSE Russell. Benchmark data as of 11/30/24. You cannot invest directly in an index. Past performance is not indicative of future returns.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Research Analyst

Hyun Kang joined WisdomTree in July 2022 as a Research Analyst. As a part of the Index team, he assists with the creation and maintenance of the firm’s indexes and supports the group’s research initiatives across various strategies. Hyun graduated from Carnegie Mellon University, with a B.S. in Business Administration and an additional major in Statistics and Machine Learning.