EES

U.S. SmallCap Fund

Published October 17, 2024

Global Head of Research

Small-cap stocks have a lot riding on the upcoming election.

When former President Trump was elected in 2016, there was a massive rally in U.S. small-cap stocks. One central catalyst was the U.S. corporate tax rate cut, as small-cap companies tend to have effective tax rates closest to the headline figure—at that time, 35%. Because President Trump won the election with a majority in both the U.S. House of Representatives and the U.S. Senate, he was able to lower this rate to the current level of 21%.1

Tax rates will be renegotiated next year, and small caps again will be in focus.

But we were curious if a rally in U.S. small-cap stocks happened solely in 2016 or if there is a pattern beyond just that single year.

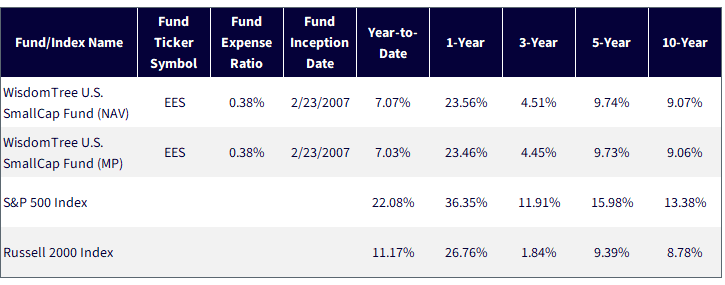

The WisdomTree U.S. SmallCap Fund (EES) was launched on February 23, 2007. It is designed to track the total return performance, before fees and expenses, of the WisdomTree U.S. SmallCap Index.

The most well-known U.S. small-cap equity index is the Russell 2000 Index. As of September 30, 2024, 27.37% of the weight in this Index was in companies that did not deliver positive earnings over the past 12 months.2 WisdomTree’s approach seeks to include only small-cap companies with positive core earnings and to also weight these stocks by their earnings, thereby lowering the overall price-to-earnings (P/E) ratio.

An index of small-cap companies with a lot of domestic earnings should be sensitive to changing tax rates.

Source: WisdomTree; specifically, data is from the PATH Fund Comparison Tool, accessed as of 10/13/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results.

Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be

worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted.

For the most recent month-end and standardized performance, click here.

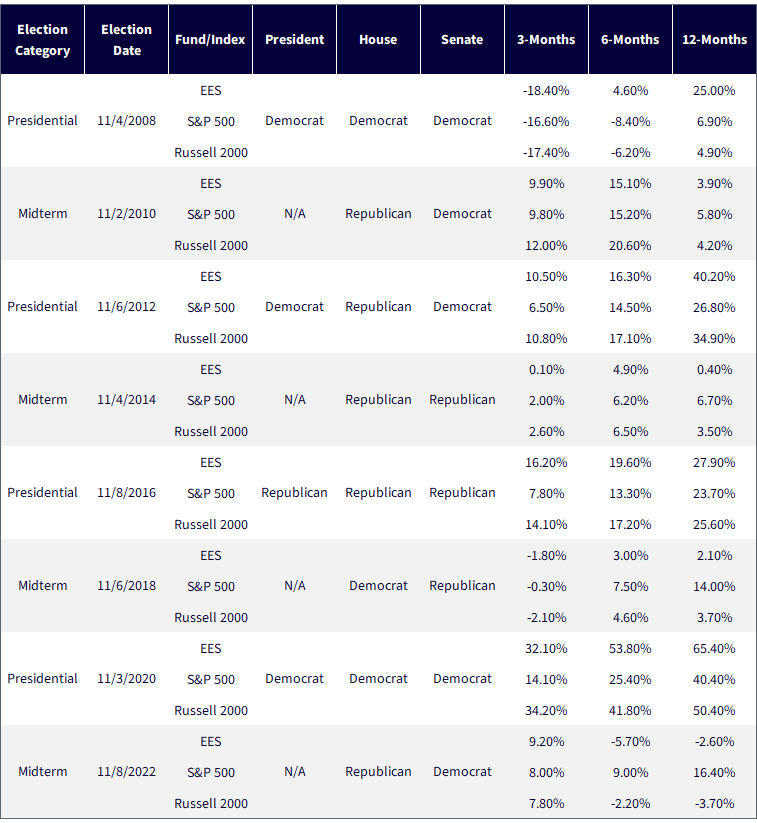

In figure 2, we evaluate 3, 6 and 12 months after all of the elections, midterm and presidential, for which EES has had live performance history.

Sources: Wikipedia for election dates and winning parties within the presidency, U.S. Senate and U.S. House of Representatives. WisdomTree for

the returns; specifically, data is from the PATH Fund Comparison Tool, accessed as of 10/13/24. NAV denotes total return performance at net

asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal

value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original

cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and

standardized performance, click here.

When we calculated the simple averages of the returns of the different periods shown in figure 2, we saw that, on average, looking at 12 months following the election represented the strongest overall group of returns. For most of these elections, the picture was positive. EES had a stand-out year in 2020.

The causality in any of these cases can be tricky. We mentioned 2016 because there was 1) a tax policy change discussed in the campaign and then 2) a sweep across the presidency, U.S. Senate and U.S. House of Representatives by a single party. This allows us to at least build a narrative that can connect tax policy expectations to equity returns.

In 2020, we were in the midst of the COVID-19 global pandemic. Equity markets crashed until March 23, 2020, and then rallied significantly through the end of the year. There was a lot of fiscal and monetary stimulus being implemented during this time, so it is a bit of an outlier relative to the others.

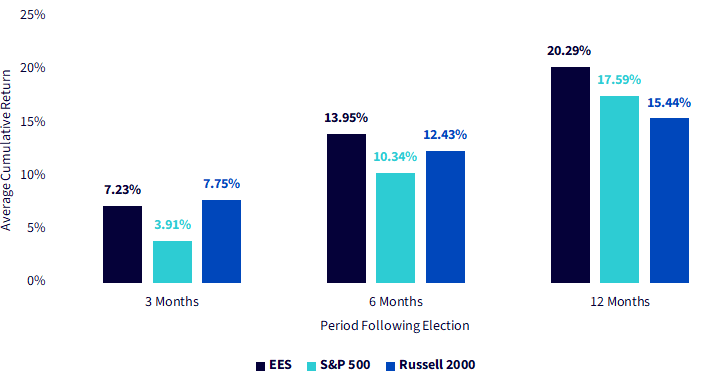

Source: WisdomTree; specifically, data is from the PATH Fund Comparison Tool, accessed as of 10/13/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results.

Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may

be worth more or less than their original cost. Current performance may be lower or higher than the performance data

quoted. For the most recent month-end and standardized performance, click here.

Now, even with all of that said, as divided as the rhetoric may sound as we approach the 2024 U.S. election, if history has been any guide, it has been a losing proposition, for the most part, to bet against U.S. equity markets.

There are never guarantees as to what we may see, return-wise, but we’d remind people that, frequently, the most likely outcome is a divided government where much of the current policy simply continues along.

1 Source: Benjy Sarlin, “Republican-led Congress passes sweeping tax bill,” CNBC.com, 12/20/17.

2 Source: WisdomTree; specifically, WisdomTree’s Fund Comparison tool within its broader PATH family of tools, with data accessed as of 10/13/24.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. SmallCap Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.