The Other Side of Tariffs

Published June 18, 2025

Samuel Rines

Macro Strategist, Model Portfolios

Key Takeaways

- In June 2025, recreational vehicle companies like Brunswick and Polaris Industries revealed deepening earnings pressure from a trifecta of headwinds: tariffs, interest rates and post-pandemic demand collapse.

- While these companies face ongoing struggles, a key shift—tariff rates on Chinese goods dropping from 145% to 30%—has improved forward earnings outlooks and exposed contrarian opportunities.

- Both firms are responding strategically with leaner operations, build-to-order models and domestic production, positioning them to rebound when interest rates fall and consumer demand stabilizes.

The onslaught of tariff news from Washington has overshadowed the impact on companies. Those impacts are meaningful in some cases. Some traditional retailers—like GAP—have stated that tariffs will be a significant hit to their profitability. Others—like Best Buy—have downplayed the issues given their flexible sourcing. Some win, some lose and some are trapped. Attempting to paint a clear picture of what the tariffs really mean for equities is difficult to parse. As always, there is only one question that matters: Are the companies that are taking the most significant tariff hits now the opportunities of the future?

That remains to be seen. But for some of the most impacted, it is not the only headwind they face. Digging through the earnings calls provides a stark, somewhat jolting, realization. Many of the companies with the largest disclosed earnings pressure from tariffs were already facing downturns in their end markets. Many of the companies in the midst of those market downturns were interest rate sensitive as well. That is not the best trifecta of issues to be facing in the current environment.

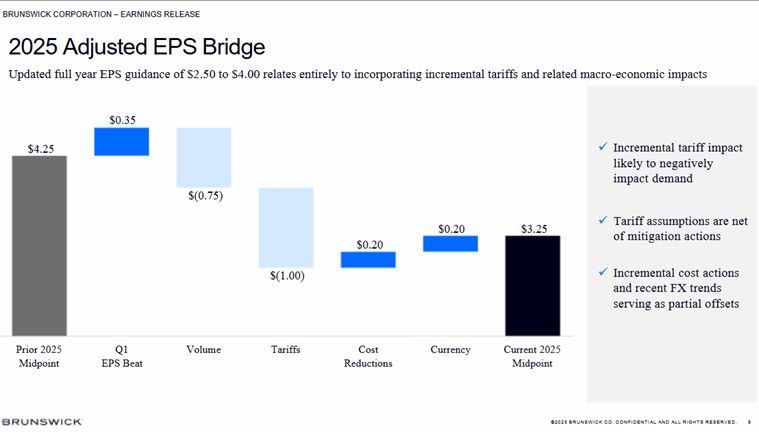

Building boats was a great business during and immediately following the pandemic. Then it wasn’t. The problems of consumer saturation (everyone who wanted a boat bought one) and elevated interest rates (boats tend to be financed) combined to create a downturn. The volume hit in the earnings bridge above tells that part of the story. The tariff bar tells the new, more pronounced part of the issue.

To be clear, Brunswick is not the only one facing this trifecta of challenges. There are others. One is Polaris Industries, with a similar story of boom, bust and turmoil. But a few pieces of the story are being ignored. The boom and bust cycle is not surprising to anyone who has followed the recreational vehicle industry. Interest rate increases? Not new. Tariffs on top of both of those? New. And that is where the opportunity lies.

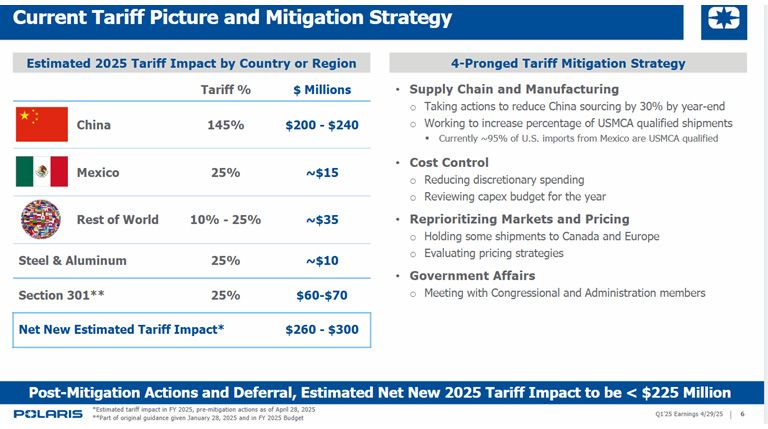

That opportunity is embedded in the current headwinds. Both companies are three years into a downturn. Both companies took the opportunity to increase prices during the pandemic. Both companies are reliant—to a degree—on financing and therefore interest rates. Both companies are getting slammed by tariffs. But those headwinds are not going to last forever. Polaris Industries guided for the “tariffs of the time” on China. That 145% is no longer. Instead, it is now 30%. That in and of itself changes the outlook for the company on the earnings front.

Not to mention, the cycle will eventually normalize. At some point, the downturn will end. Interest rates will be less of a headwind. And the tariffs will be less of a problem. In the interim, these two are finding ways to be “leaner and meaner” for the next cycle. Less inventory overhang with better build-to-order practices is a start. More resilient supply chains and domestic production (which both have) are—oddly—headwinds for now. As the tariff and trade situation evolves and interest rates normalize, the COVID boom and post-COVID lessons of the recreational vehicle makers will be among the more intriguing investment evolutions.

Categories

About the contributor

Samuel Rines

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.