WCBR

Cybersecurity Fund

Published August 20, 2024

Global Head of Research

As the earnings reports across major technology companies have come out in July and August 2024—so far—the primary question seems to be: We are seeing all of this money spent on AI, but what is going to generate a reasonable return on that investment?

Technologies are really just tools, not ends in themselves. Their value comes from how we use them. When we speak to investors, the topic that seemingly gets them the most excited is the possible breakthroughs in biotechnology.

However, excitement doesn’t always translate into share price returns, and biotechnology returns, in general, have been challenged in recent years. These companies are very speculative. We often write of newer technology companies that may not yet have positive earnings, but in the biotechnology space, it is not difficult to find companies that don’t even have revenues. It is very difficult to repeatedly look at companies that don’t even have revenues and try to determine if they will (or won’t) find success.

Challenges have also abounded:

These challenges, and others, are important to be aware of even if we recognize that the environment can shift at any time, with former headwinds quickly becoming tailwinds.

For the better part of the period from November 2022 leading into July 2024, equity market performance was defined by the largest companies—we even started to call them the “Magnificent 7”2—leading the market. More speculative companies—like those in biotechnology—were not associated with equity performance leadership in any sort of major trend during this period.

During July 2024, catalyzed by a cooler inflation report that could lead to a greater expectation of actual U.S. Federal Reserve policy rate cuts, we suddenly saw smaller market-capitalization companies outperform the largest market-capitalization companies.3

Biotechnology companies, even those within the WisdomTree BioRevolution Fund (WDNA), participated in this rally. In figure 1b, we even see that amongst WisdomTree’s six different thematic Funds, WDNA was actually the top performer during the month of July 2024.

Source: WisdomTree, specifically data is from the PATH Fund Comparison Tool, as of 6/30/24. NAV denotes total return performance at net asset

value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of

an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current

performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance

and to download the respective Fund prospectuses, click the relevant ticker: WDNA, WCBR, WCLD, WTAI, WBAT and WTRE.

Source: WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 8/4/24. NAV denotes total return performance at

net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and

principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their

original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and

standardized performance and to download the respective Fund prospectuses, click the relevant ticker: WDNA, WCBR, WCLD, WTAI,

WBAT and WTRE.

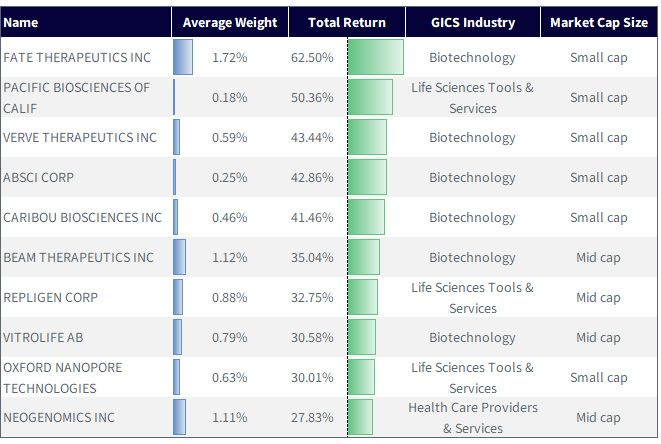

If we dig into the WDNA portfolio, we see the top 10 performing companies—with some pretty big returns in a short time—emphasizing that “small cap” status. Even if there are, of course, broadly diversified small-cap equity funds, WDNA is also tapping into this rally somewhat.

We’d recognize that these companies are high on the risk spectrum. Yes, July 2024 looked strong, but in a tougher market condition, it would be difficult to argue that these companies would exhibit share price performance that mitigated downside risk.

Source: Bloomberg. Data pulls in the top 10, ranked by performance, for the month of July 2024 from within WDNA. “Average

Weight” refers to the weight during July 2024 within WDNA, averaged for the period. “GICS” refers to the “Global Industry

Classification Standard,” which is shown at the “industry” level. “Small cap” refers to companies below $2 billion in market

capitalization. “Mid cap” refers to companies between $2 billion and $10 billion in market capitalization. Past performance is

not indicative of future results. Holdings subject to change.

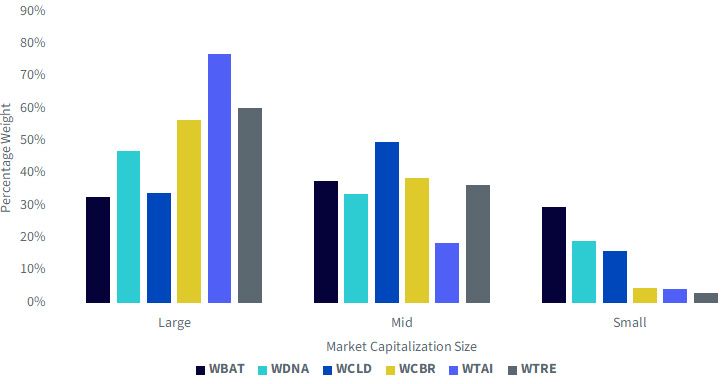

We can also confirm in figure 3 that WDNA, relative to WisdomTree’s other thematic equity Funds, has the second-highest proportion of small-cap companies.

Source: the WisdomTree Fund Compare Tool within the PATH suite of tools, as of 6/30/24. Holdings subject to change.

At WisdomTree, we work with Dr. Jamie Metzl, who recently published the book Superconvergence, detailing how different megatrends, like artificial intelligence, are converging with advances in biotechnology and leading to a massive amount of potential innovation. We’ve written a series of blog articles about different concepts discussed in this book.

Take mRNA as an example. We saw what happened with the COVID-19 vaccines generated in record time with technologies that had been under study for decades. Companies like Moderna rallied massively as they served the market’s insatiable appetite for vaccines. We love to discuss mRNA not only for what it did in the past with COVID-19 but for what it represents in the future—a platform upon which other therapies may be built. We are on the cusp of using this technology on a far broader basis—and it is not the only one.

The excitement, we find, is resilient, and we believe that with further announcements and developments, the biotechnology space may very well generate a period of stronger returns—especially if the macro backdrop becomes a bit easier with lower interest rates.

1 Source: Professor Jeremy J. Siegel, "It's Time for the Fed to Cut", WisdomTree,8/5/24, https://resources.wisdomtree.com/weekly-siegel-commentary/archive-august-5-2024

2 Refers to Amazon, Apple, Alphabet, Microsoft, Tesla, Nvidia and Meta Platforms.

3 Source: Christopher Gannatti, "Will July 2024 Be a Harbinger of Small-Cap Strength in U.S. Equities?", WisdomTree, 8/6/24, https://www.wisdomtree.com/investments/blog/2024/08/06/will-july-2024-be-a-harbinger-of-small-cap-strength-in-us-equities

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WDNA: The Fund invests in BioRevolution companies, which are companies significantly transformed by advancements in genetics and biotechnology. BioRevolution companies face intense competition and potentially rapid product obsolescence. These companies may be adversely affected by the loss or impairment of intellectual property rights and other proprietary information or changes in government regulations or policies. Additionally, BioRevolution companies may be subject to risks associated with genetic analysis. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee, and the Index may not perform as intended.

WCBR: The Fund invests in cybersecurity companies, which generate a meaningful part of their revenue from security protocols that prevent intrusion and attacks to systems, networks, applications, computers and mobile devices. Cybersecurity companies are particularly vulnerable to rapid changes in technology, rapid obsolescence of products and services, the loss of patent, copyright and trademark protections, government regulation and competition, both domestically and internationally. Cybersecurity company stocks, especially those that are internet-related, have experienced extreme price and volume fluctuations in the past that have often been unrelated to their operating performance. These companies may also be smaller and less experienced companies, with limited product or service lines, markets or financial resources and fewer experienced management or marketing personnel. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended.

WCLD: The Fund invests in cloud computing companies, which are heavily dependent on the internet and utilizing a distributed network of servers over the internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended.

WTAI: The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee, and the Index may not perform as intended.

WBAT: The Fund invests in equity securities of exchange-listed companies globally involved in the investment themes of battery and energy storage solutions (“BESS”) and innovation. The value chain of BESS companies is divided into four categories: raw materials, manufacturing, enablers and emerging technologies. Innovation companies are those that introduce a new, creative or different technologically enabled product or service in seeking to potentially change an industry landscape, as well as companies that service those innovative technologies. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets, and the Index may not perform as intended.

WTRE: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in real estate involve additional special risks, such as credit risk, interest rate fluctuations and the effect of varied economic conditions. A Fund focusing on a single country and/or sector and/or emphasizing investments in smaller companies may experience greater price volatility. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.