China’s Third Plenum: Focus on Manufacturing and Very Short-Term Stimulus

Published August 19, 2024

Liqian Ren

Director of Modern Alpha

Baoqi Zhu

Associate Director, Quantitative Research & Multi Asset Solutions

Key Takeaways

- China’s four-day Third Plenum emphasized a very short-term stimulus to achieve this year’s growth target and continued investment in manufacturing, leading to a negative market reaction, with the CSI 300 Index dropping by 3.4% and the Hang Seng Index falling by 4.4%.

- Despite mentioning potential reforms like fiscal reform and easing restrictions on migrant workers, the documents did not introduce significant new information or fundamental reforms to boost consumption despite weak GDP growth and deflation risks.

- Specific industries—particularly in manufacturing with advanced technology—might benefit from new policies, with the lithium-ion battery industry showing strong potential due to global demand for renewable energy and energy storage solutions.

China’s four-day Third Plenum, which typically centers on economic policies and reforms, concluded on July 18, 2024. The meeting highlighted a very short-term stimulus to achieve this year’s growth target and emphasized continued investment in manufacturing without initiating significant new stimulus measures.

Unsurprisingly, market reactions were less than favorable. The CSI 300 Index dropped by 3.4%, and the Hang Seng Index fell by 4.4% in the week following the meeting. We’ve discussed this in our podcasts and blogs before and after the meeting, explaining why a framework of minimal stimulus remains a reasonable baseline.

China’s Macro Conditions:

Although the communique and follow-up documents mentioned potential reforms, such as fiscal reform and easing restrictions on migrant workers, the implementation details are crucial. Most of the content, including industry policies like “new quality productive forces,” aligned with previous policies and did not introduce new information.

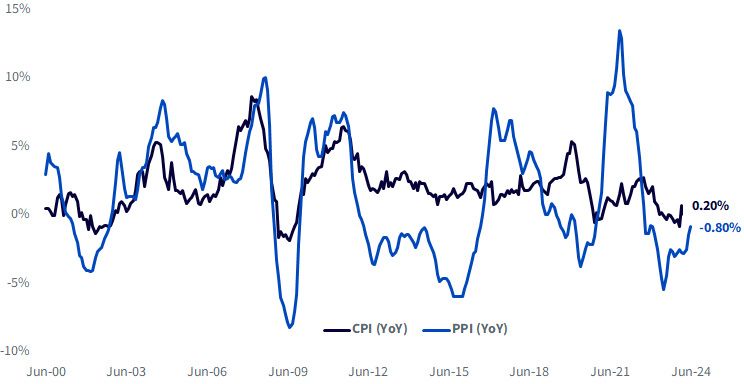

China’s CPI year-on-year (YoY) turned negative last year, slightly rebounding to 0.2% in June 2024. Meanwhile, the PPI YoY remained negative in the same month. Despite earlier cuts to interest rates and the reserve requirement ratio, the market is eager to see if there will be significant stimulus, particularly for the consumption sector, to combat deflation risks. Weak GDP growth and a declining household consumption share have fueled these expectations. However, current documents from the Plenum indicate no fundamental reforms to boost consumption.

Figure 1: China CPI (YoY) and PPI (YoY)

Source: Bloomberg, for the period January 2000–Jun 2024.

Potential Opportunities in Manufacturing:

Not all industries are facing challenges. Although the long-term effects of industry policies, such as the “new quality productive forces,”1 will take time to materialize, focusing on specific industries could provide potential opportunities. Industries, particularly in manufacturing with a high market share and advanced technology, might benefit from new policies, offering potential growth despite broader economic uncertainties.

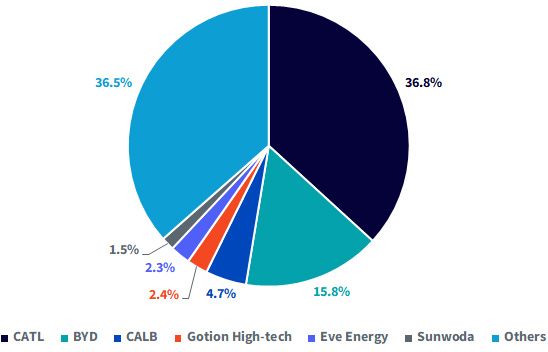

One such industry is lithium-ion batteries. The top six Chinese battery makers— CATL, BYD, CALB, Gotion High-tech, Eve Energy and Sunwoda—accounted for 63.5% of the global market share in 2023, with CATL alone holding more than one-third of the global market share.

Figure 2: Global Market Share of Lithium-Ion Battery Makers (2023)

Source: "From Jan to Dec in 2023, Global EV Battery Usage Posted 705.5GWh, a 38.6% YoY Growth",

SNE Research, as of 2/7/24.

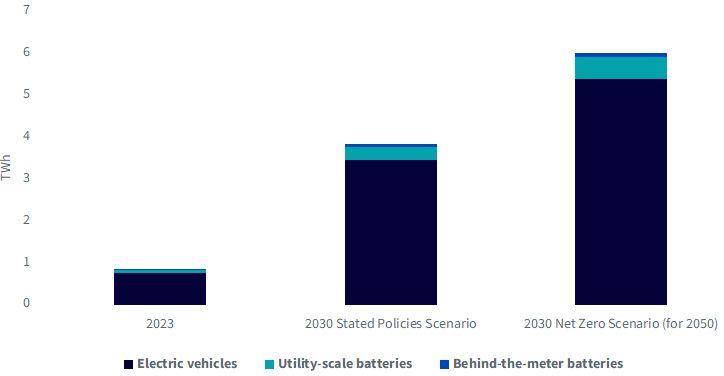

The potential demand for batteries is enormous. World leaders have pledged to significantly expand renewable energy capacity by 2030, expecting a sixfold increase in energy storage, which greatly enhances the potential for sales growth.

Figure 3: Annual Battery Demand by Application and Scenario, 2023 and 2030

Source: "Batteries and Secure Energy Transitions - World Energy Outlook Special Report", IEA (April 2024). TWh = trillion watt-hours.

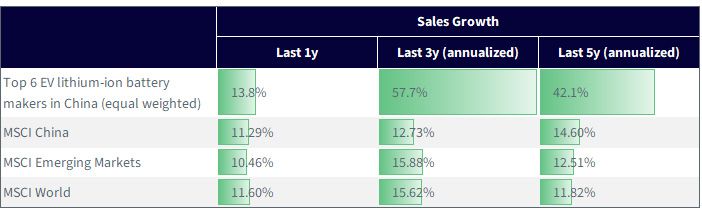

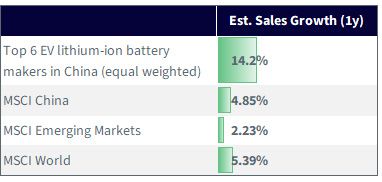

For the top battery makers in China, sales have soared in recent years, surpassing both China’s and the world’s benchmarks. These companies also have significantly higher estimated sales growth for the next year, indicating China’s strong potential in this area.

Figure 4: Sales Growth YoY over the Last 1, 3 and 5 Years

Source: FactSet, as of 7/20/24. You cannot invest directly in an index.

Figure 5: Sales Growth YoY Forecasts for the Forward 1 Year

Source: FactSet, as of 7/20/24. You cannot invest directly in an index.

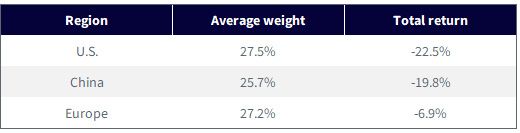

To illustrate the performance of the battery industry, we use the WisdomTree Battery Value Chain and Innovation Fund (WBAT) as an example. WBAT aims to provide targeted exposure to companies involved in battery and energy storage solutions and innovation. The strategy primarily targets the U.S., China and Europe.

In the first half of 2024, the total returns across these three regions within WBAT's portfolio showed minimal differences despite varying macroeconomic conditions. This suggests that company-level factors may play a more significant role than macro factors when investing in battery solutions.

Figure 6: Average Weights and Total Returns of U.S., China and Europe Domicile Companies in WBAT

Source: Bloomberg, for the period 12/29/23–6/28/24.

Conclusion

The absence of significant new policies and the market’s lukewarm response highlight the challenges ahead. However, short-term measures like slightly lower loan rates are expected to be implemented to achieve the 5% GDP growth target. Additionally, focusing on high-potential manufacturing industries with a substantial market share and advanced technology, such as lithium-ion batteries, could offer promising opportunities for investors.

1 “New quality productive forces” refers to a major concept put forward by President Xi Jinping. Marked by innovation, new quality productive forces are advanced productivity in essence, with high quality as the key and substantial increase in total factor productivity as its core hallmark.

Important Risks Related to this Article

For current holdings of WBAT, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. The Fund invests in equity securities of exchange-listed companies globally involved in the investment themes of battery and energy storage solutions (“BESS”) and innovation. The value chain of BESS companies is divided into four categories: raw materials, manufacturing, enablers and emerging technologies. Innovation companies are those that introduce a new, creative or different technologically enabled product or service in seeking to potentially change an industry landscape, as well as companies that service those innovative technologies. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

Related articles

About the contributors

Liqian Ren

Director of Modern Alpha

Liqian Ren, Ph.D., joined WisdomTree as Director of Modern Alpha in 2018. She leads WisdomTree’s quantitative investment capabilities and serves as a thought leader for WisdomTree’s Modern Alpha® approach. Liqian was previously at Vanguard, where she worked for 12 years, most recently as a portfolio manager in the Quantitative Equity Group managing Vanguard’s active funds and conducting research on factor strategies. Prior to joining Vanguard, she was an associate economist at the Federal Reserve Bank of Chicago. Liqian received her bachelor’s degree in Computer Science from Peking University in Beijing, her master’s in Economics from Indiana University—Purdue University Indianapolis, and her MBA and Ph.D. in Economics from the University of Chicago Booth School of Business. Liqian co-hosts a podcast on China and Asian markets with Jeremy Schwartz, WisdomTree’s Global Head of Research, and she is a co-host on the Wharton Business Radio program Behind the Markets on SiriusXM 132.

Baoqi Zhu

Associate Director, Quantitative Research & Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).