WTAI

Artificial Intelligence and Innovation Fund

Published November 12, 2024

Global Head of Research

It has been nearly two years since the release of ChatGPT, the viral application that achieved a milestone of 100 million users in two months1 and changed our collective perception regarding artificial intelligence’s potential.

Global equity markets have since been led by the Magnificent 72—the companies large enough to develop, train and run models with similar capabilities as ChatGPT.

Megatrends do not move in a simple upward trend without correction. Even if AI continues to march forward, it will naturally get tougher for the world’s largest companies to beat expectations and continually raise guidance to keep their already enormous market capitalizations growing.

This piece highlights a few ideas to participate in the exciting new technologies that are being developed.

Perhaps the hottest area of investment in the artificial intelligence space has been generative AI, the broader category of applications that ChatGPT represents. However, many of the most notable models are massive, with hundreds of billions, if not trillions, of parameters. The infrastructure and expertise needed requires a level of resources only realistic for the world’s largest firms.

The cloud hyperscalers,3 with their sprawling datacenters, are central to the story. We saw an example play out with OpenAI and Microsoft—OpenAI needed money, and Microsoft has thus far provided roughly $14 billion,4 but equally if not more important was access to Microsoft’s Azure cloud computing infrastructure.

Alphabet, Microsoft and Amazon—the companies running the three largest public cloud platforms—are in a race. Giving users on these platforms access to the largest AI models is an added carrot that, possibly, encourages users to spend even more money and helps these companies grow their cloud revenues that much faster.

Nvidia has also created an extremely valuable niche in this discussion of behavioral economics and business strategy. Each Nvidia chip release gets massive attention. Customers on the hyperscaler cloud platforms see the capabilities of the A100, then H100 and soon-to-be B100 chips—and they want access. Each cloud provider needs to provide at least a baseline level of access to Nvidia’s newest technologies or risk customers going elsewhere.

As Nvidia’s chips provide faster model development, training and inference capabilities, these companies continue to buy Nvidia’s chips—even if they all simultaneously are seeking to develop their own internal semiconductors.

Bottom line: While spending on AI infrastructure will not last forever, it should last for a number of years. The world’s most well capitalized companies see this as existential investment and at all costs plan to keep up with peers rather than focus on return on investment (ROI), telling us these firms are betting that there is a lot of growth to come.5

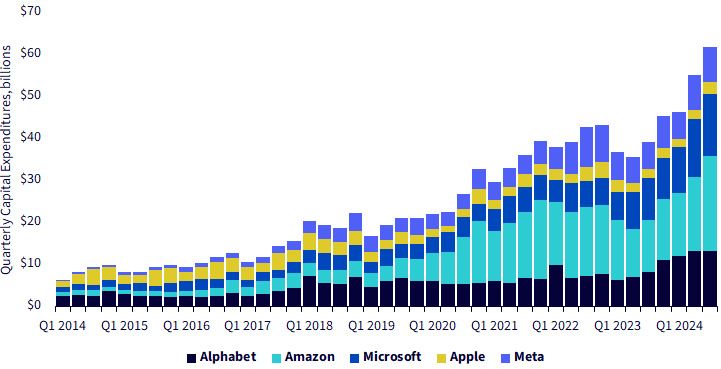

Figure 1 looks at the quarterly capital expenditures (CapEx), publicly reported for Alphabet, Amazon and Microsoft (the hyperscalers), plus Apple and Meta Platforms.

The narrative around this figure is discussed when each company reports quarterly earnings. Currently, the language is focused on the idea of “maintaining” and “growing,” rather than signaling a return to more of a profitability focus. We are seeing an annualized rate in the neighborhood of $250 billion for just these five firms.

Sources: Bloomberg, FactSet. Past performance is not indicative of future results.

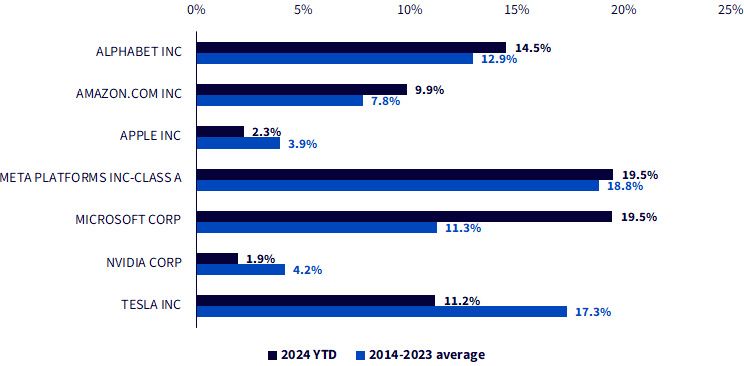

Another way to look at this is shown in figure 2, where we open things up from the companies where CapEx is in extreme focus to the broader Magnificent 7. Nvidia and Tesla face different market dynamics than the aforementioned five companies in figure 1. Even so:

Sources: Bloomberg, FactSet. Past performance is not indicative of future results.

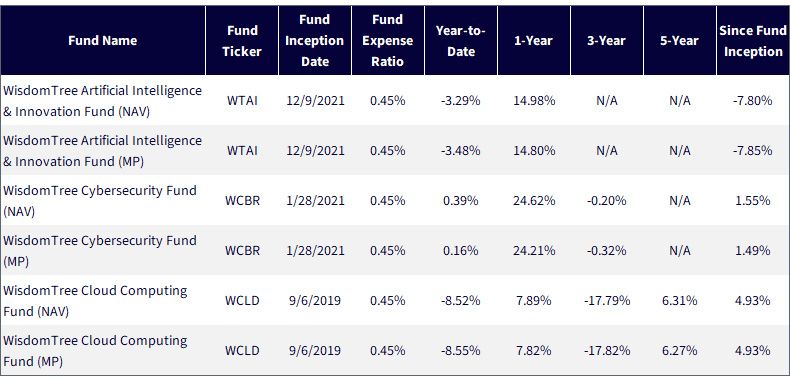

WisdomTree has three distinct investment strategies that relate to AI directly:

Sources: LSEG, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, as of 9/30/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return

and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their

original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and

standardized performance, click the relevant ticker: WTAI, WCBR, WCLD.

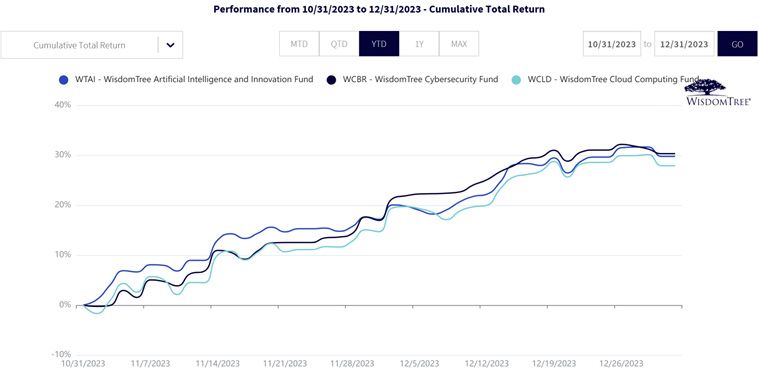

Equity markets are constantly taking in new information. During November and December 2023, it was viewed as nearly certain that the U.S. Federal Reserve would lower interest rates quickly in 2024. This was the primary reason that WTAI, WCBR and WCLD exhibited a roughly 30% return in two months.

While we’d love to say otherwise, for any two-month period, this should be viewed as an extremely unusual level of returns.

Sources: LSEG, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, for the period 10/31/23–12/31/23. NAV

denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future

results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be

worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the

most recent month-end and standardized performance, click the relevant ticker: WTAI, WCBR, WCLD.

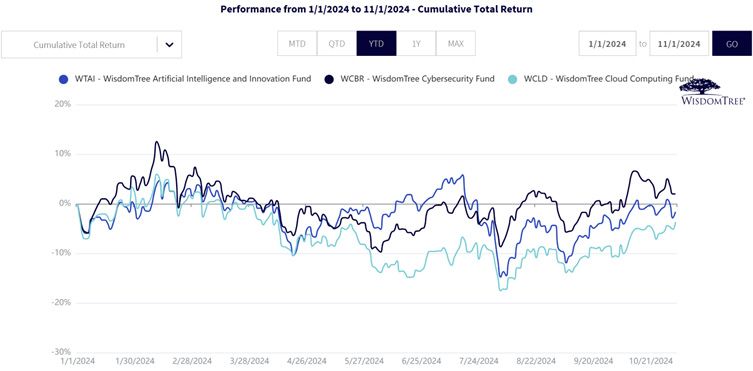

Then the expectations of six to seven rate cuts starting in early 2024 did not materialize. The volatility in returns exhibited by WTAI, WCBR and WCLD in 2024 could be viewed at least in part as an adjustment to these expectations. We see this volatility on display in figure 5, which includes impacts from all sorts of other events as well.

Sources: LSEG, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, for the period 12/31/23–11/1/24. NAV

denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future

results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be

worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the

most recent month-end and standardized performance, click the relevant ticker: WTAI, WCBR, WCLD.

The SaaS nature of WCBR and WCLD—two strategies where this is basically THE exposure on a business model basis—is important to keep in mind. Companies operating in this model can develop software and then place it in the hands of hundreds of millions of users—if the demand is there. The key expense that many of them face is how to get customers to know they exist.

We note that few business models in history have been shown to scale as quickly or with as high a gross margin as SaaS businesses, when they are in favor.

WTAI, on the other hand, includes exposure to a diversified array of companies and business models. Making physical products—like Tesla making cars—is different from creating and distributing software. Still, we don’t believe that software alone accurately reflects AI.

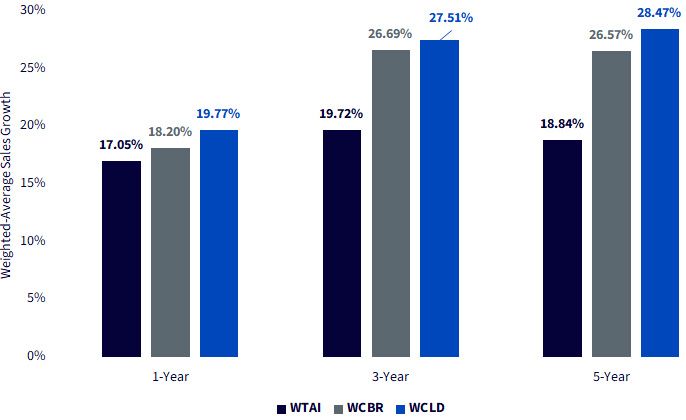

Looking to figure 6, we see that the weighted-average sales growth across all three strategies has been strong. Even if the most recent year looks a bit lower relative to the three-year and five-year periods, these figures are still strong.

Sources: LSEG, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, as of 9/30/24.

1 Source: https://www.visualcapitalist.com/wp-content/uploads/2023/07/CP_Threads-Fastest-100-Million.jpg

2 The Magnificent 7 refers to Alphabet, Amazon, Apple, Microsoft, Meta Platforms, Nvidia and Tesla.

3 When we say “cloud hyperscalers” we refer to Alphabet, Amazon and Microsoft, which are widely cited as having the world’s three largest public cloud computing infrastructure platforms.

4 Source: Jordan Novet, “Microsoft CFO Says OpenAI Investment Will Cut into Profit this Quarter,” CNBC.com, 10/30/24.

5 Source: Nate Rattner, “Breaking Down the Tech Giants’ AI Spending Surge,” Wall Street Journal, 8/3/24.

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WTAI: The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on Innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

WCBR: The Fund invests in cybersecurity companies, which generate a meaningful part of their revenue from security protocols that prevent intrusion and attacks to systems, networks, applications, computers and mobile devices. Cybersecurity companies are particularly vulnerable to rapid changes in technology, rapid obsolescence of products and services, the loss of patent, copyright and trademark protections, government regulation and competition, both domestically and internationally. Cybersecurity company stocks, especially those which are internet related, have experienced extreme price and volume fluctuations in the past that have often been unrelated to their operating performance. These companies may also be smaller and less experienced companies, with limited product or service lines, markets or financial resources and fewer experienced management or marketing personnel. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended.

WCLD: Fund invests in cloud computing companies, which are heavily dependent on the internet and utilizing a distributed network of servers over the internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties and the Index may not perform as intended.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.