A Post-Election and Post-Fed Look at Treasuries

Published November 13, 2024

Head of Investment and Fixed Income Strategy

Key Takeaways

- Following the U.S. presidential election, U.S. Treasury (UST) yields experienced a sharp rise akin to the “Trump Trade” of 2016, but the market will shift its focus back to macroeconomic data and Federal Reserve (Fed) policy.

- Concerns over ballooning budget deficits and increased Treasury supply are valid but secondary, with macroeconomic conditions and Fed decisions driving rate trends more significantly.

- The Federal Reserve’s data-dependent stance, reinforced in the November FOMC meeting, suggests further rate cuts are possible, but UST yields are likely to remain elevated without a significant deterioration in labor market conditions.

Listen to the accompanying episode of the Basis Points podcast:

Last week was chock full of headline-making events, to say the least. Typically, an FOMC meeting would take center stage, but when you have a presidential election day occurring in the same timeframe, Powell & Co. took a backseat this time around. That being said, both of these events deserve their due course, and that’s what this blog post is going to do in terms of how they impact the U.S. Treasury (UST) market.

Let’s begin with the post-election part of the equation. As of this writing, control of the House of Representatives had yet to be officially determined, but the money and bond markets (as well as the betting market) were all assuming the Republicans would retain the majority. In other words, the “red sweep” would be the final outcome.

The UST market didn’t wait for the final results, that’s for sure, as the “Trump Trade” was on full display in a knee-jerk response to the outcome of Election Day, with UST yields rising in a rather noticeable fashion. The rise in the UST 10-Year yield was just like in 2016, when an increase of roughly 20 basis points (bps) occurred the day after the election. However, there is one big difference: the Fed was raising rates back then, not cutting them…more on that later.

A great deal of attention was given to the potential negative effects of a “red sweep” on the budget deficit and the attendant increase in Treasury supply. But let’s put it into some perspective. Budget deficits and increased Treasury supply were going to occur no matter a red or blue sweep, and a divided government would still mean baseline deficits approaching $2 trillion remaining the norm. To illustrate, the fiscal year 2024 shortfall came in at $1.8 trillion, or +8.1% higher than FY 2023’s deficit of $1.7 trillion.

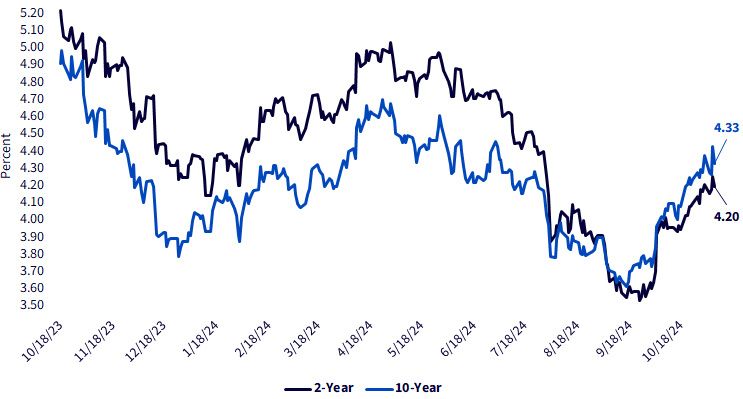

U.S. Treasury Yields

Source: Bloomberg, as of 11/8/24.

While anxiety surrounding swelling deficits and Treasury supply are legitimate concerns, there’s more to the story than these factors. Indeed, in the past, when deficits and the attendant required increase in Treasury supply have been contributing factors to rate trends, this factor usually served as more of a secondary or tertiary force. The macro and Fed policy backdrops are the primary drivers for rate trends, with deficits and supply essentially adding to or deleting from an existing trend. This is exactly the case this time around as well because President-elect Trump’s policies were viewed by the bond market as being more pro-growth and inflationary than what a “blue sweep” would have resulted in.

Interestingly, as the graph highlights, the UST 2- and 10-Year yields have fallen by roughly 100 bps two times in the last year, even when budget deficits were approaching $2 trillion and the market was dealing with record supply. In my opinion, the UST market will move on from the election results and return its focus to the macro-economic data and the Fed.

That brings us back to the Fed, where the November FOMC meeting and accompanying Powell presser underscored that future policy decisions will remain highly data-dependent and not be influenced by the election results any time soon. Remember, legislation needs to be passed first and actually implemented before one can make any economic/inflation assessments. As I wrote in my post-FOMC blog piece last week, the December FOMC gathering will be a “live” meeting, where another quarter-point rate cut seems likely at this point, data permitting.

Conclusion

Instead of focusing on how high the UST 10-Year yield may be headed, I think the more pertinent question is whether it can go back down to where it was around mid-September. Unless the labor market data collapses, the answer would be “no,” with yields more than likely remaining elevated in the months ahead.

About the contributor

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.