The 2026 Market: A World of Constant Rotation

Published March 23, 2026

Global Chief Investment Officer

Key Takeaways

- As AI-driven concentration pushes the Magnificent Seven above one-third of the S&P 500 while leadership rapidly rotates beneath the surface, investors should consider strategies like the WisdomTree U.S. Value Fund (WTV) that capitalize on emerging valuation dislocations.

- Traditional value indices are increasingly distorted by methodology—where expensive mega-cap stocks like Apple and Tesla still receive “value” weight—creating an opportunity for WTV’s more disciplined focus on shareholder yield and true valuation.

- WTV offers a differentiated approach to value that selectively captures mispriced growth opportunities, including companies like Nvidia trading at compelling growth-adjusted valuations.

The market environment entering 2026 has been defined by two seemingly contradictory forces.

On one side, a handful of technology companies, especially those tied to artificial intelligence infrastructure, have dominated headlines and index weights. The “Magnificent Seven” have at times represented more than one-third of the S&P 500’s total weight1.

Yet leadership beneath the surface has rotated rapidly. AI enthusiasm has created pockets of extreme valuation while other profitable businesses, sometimes in the very same sectors, have been sold aggressively.

In classic equity frameworks, the market is divided into growth and value. But when the same company can oscillate between “expensive growth story” and “temporary bargain,” the lines begin to blur.

That is where a fundamentally driven approach with active management sensitive to value becomes particularly important.

TheWisdomTree U.S. Value Fund (WTV) focuses on companies generating strong shareholder returns through dividends and buybacks while maintaining attractive valuations.

WTV’s portfolio can sometimes look very different from traditional value indices.

A Different Definition of Value

S&P style indices classify companies using separate growth and value scores based on standardized financial factors. The value score incorporates three valuation ratios:

- Book-to-price,

- Earnings-to-price and

- Sales-to-price.

Companies are ranked based on their growth and value characteristics, with roughly one-third of market capitalization allocated to value, one-third to growth and the remainder split proportionally between the two styles depending on each company’s profile. This process can lead to some surprising outcomes if looking for real value stocks.

Companies that many investors associate with higher valuations—and not traditional “value”—still appear in the S&P 500 Value Index. Under S&P’s framework, a stock doesn’t need to be “cheap” for a portion of its market cap to be allocated to Value. If a stock falls into the “blend” zone, its market cap can be split across both the Value and Growth indices. As a result, several high-profile companies receive meaningful weight in Value.

The takeaway isn’t that these stocks have become “value” in the traditional sense—many even have negative value-factor z-scores in S&P’s own scorecard—but that the methodology assigns weight across both indices when a company’s profile is not extreme enough to be classified entirely as Growth.

In short, a stock can screen expensive on traditional valuation metrics and still land partly in the Value Index if its growth and momentum characteristics aren’t strong enough to place it exclusively in Growth.

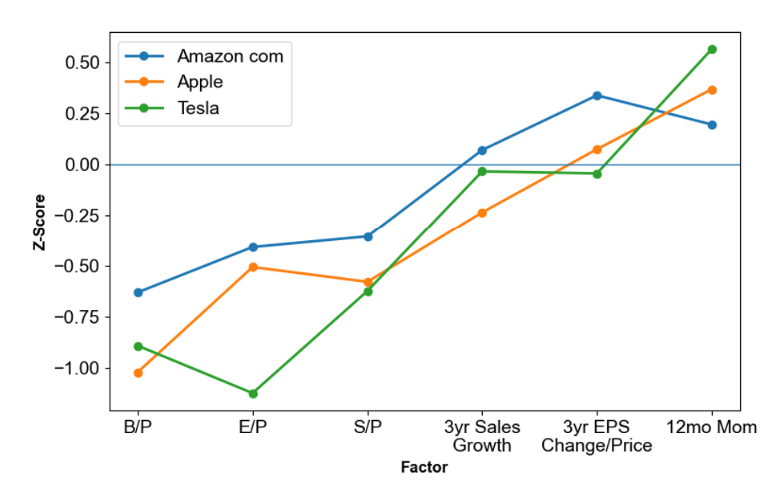

Take Tesla as an example. Tesla has sharply negative z-scores across the three value factors. But because its growth-factor z-scores are not comparably strong (with only 12-month momentum positive), a portion of its market cap is allocated to the Value Index.

Figure 1: Factor Z-Scores vs. S&P 500

Figure 2 highlights the 10 largest S&P 500 constituents (by index weight) whose market cap is split between the Value and Growth indices. Notably, Apple, Amazon and Tesla—each with positive Style Scores (more Growth than Value)—still show up as meaningful weights in the Value Index because their market caps are so large relative to the rest of the Value sleeve.

Apple is the top holding in the S&P 500 Value Index (7.3%) and the fourth-largest holding in the S&P 500 Growth Index (6.4%). Yet on traditional valuation measures, it trades well above the broader market, which many investors would not associate with classic value.

Figure 2: Top 10 Split Constituents in the S&P 500 Style Rebalance

A Potentially “Purer” Value: WisdomTree U.S. Value Fund (WTV)

WTV is designed to be more intentionally value-oriented. Rather than relying on relative style scores that must balance market cap, WTV targets shareholder yield (dividends plus buybacks) and uses additional quality-oriented screens to help avoid classic value traps.

WTV is also actively managed and its process can identify stocks that screen as high quality value.

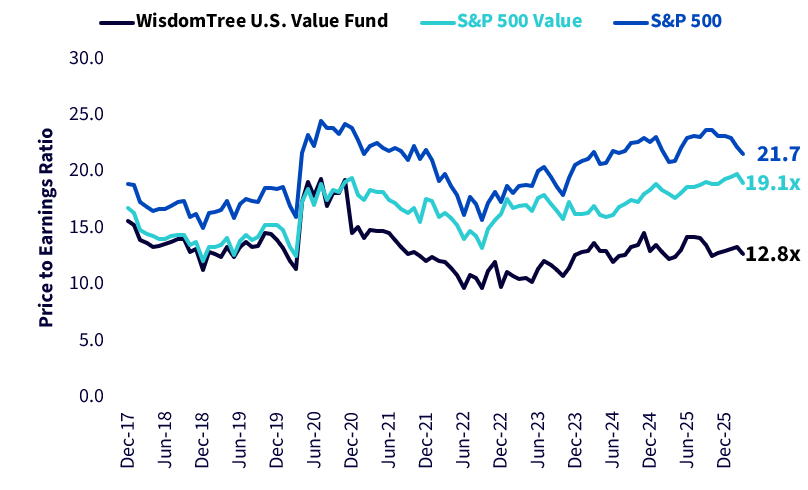

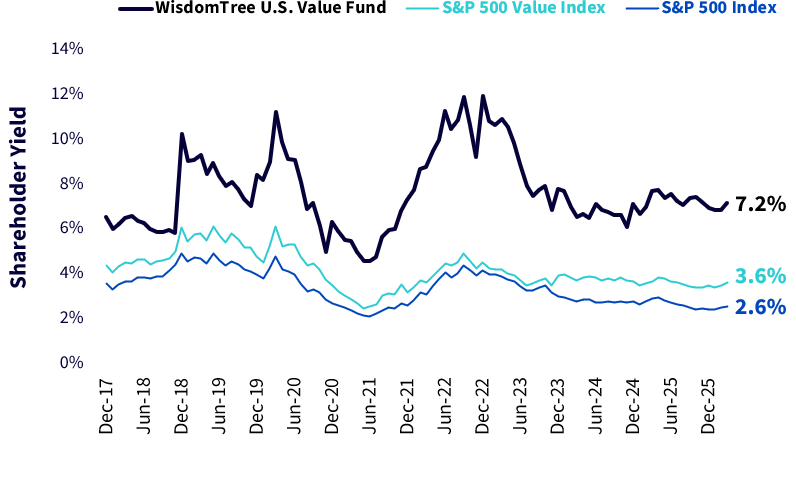

The end result is a portfolio that is meaningfully cheaper on a forward P/E (Figure 3a) and materially higher on shareholder yield (Figure 3b) than the S&P 500 Value Index.

Following the most recent rebalance, WTV’s shareholder yield sits around 7.0%, roughly double that of the S&P 500 Value Index at roughly 3.5%.

At the same time, the fund maintains attractive valuations, with a forward price-to-earnings ratio of about 12.8x, compared with 19.1x for the S&P 500 Value Index.

Figure 3a: Forward P/E Over Time

Figure 3b: Shareholder Yield Over Time

WTV is not simply chasing cheap stocks. It is identifying companies that are reasonably valued and actively returning capital to shareholders.

Broad Diversification Without Megacap Concentration

WTV typically holds around 120 companies, allowing the portfolio to focus on businesses with stronger shareholder-return characteristics.

Interestingly, more software companies are increasingly showing up in the top 10 holdings due to their high levels of share buybacks that are reducing shares outstanding—a reversal of their high valuations 4-5 years ago.

The current portfolio also tends to avoid the heavy concentration that has characterized many broad market benchmarks.

For example, the Magnificent Seven collectively represent more than 34% of the S&P 500, yet WTV currently holds only one of those companies—NVIDIA—at a 3% weight, far below its S&P 500 Index weight2.

We see this in Figure 4.

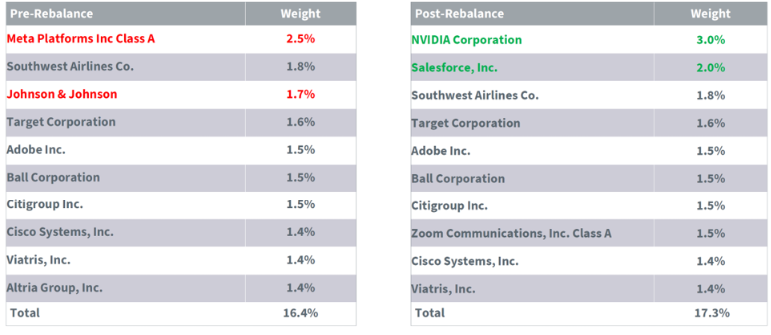

Figure 4: March 2026 Rebalance Shifts Exposure to Certain Tech Names

Source: WisdomTree, FactSet. Rebalance effective at the close of 3/11/26. Holdings subject to change.

That positioning reflects an important principle of the strategy:

The goal is not to avoid large technology companies—but to own them only when valuations make sense. The strategy repositioned from Meta Platforms towards Nvidia and Salesforce—but also has top 10 weights in Zoom, Cisco and Adobe.

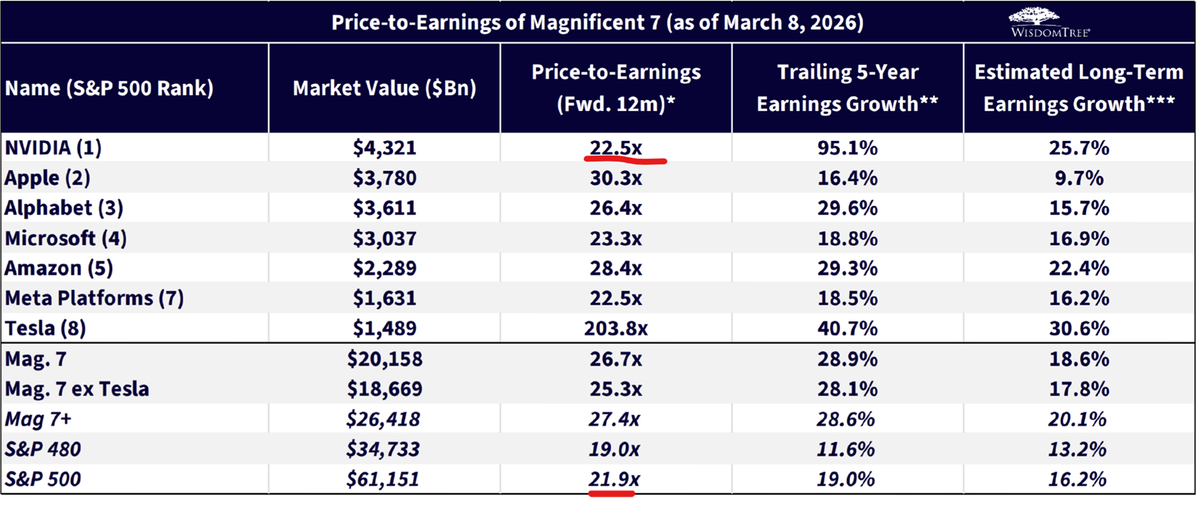

What we find fascinating in the case of Nvidia, a company with a market capitalization above $4 trillion, is the forward price-to-earnings ratio is very similar to that of the overall S&P 500 Index. But, as we see in Figure 5:

- Nvidia’s trailing 5-Year earnings growth clocked in at 95.1%, annualized. The market came in at 19.0% per year.

- On a forward basis, Nvidia’s earnings are forecast to grow at 25.7% per year, as opposed to the market at 16.2%.

Bottom line: Nvidia’s growth trajectory at a valuation similar to the market represents, to us, a significant value opportunity.

Figure 5: Nvidia’s Price Relative to its Growth Rate Looks Compelling

The Bigger Picture

The investment landscape of 2026 continues to be shaped by rapid technological change, geopolitical shifts and evolving monetary policy.

In that environment, valuation discipline may matter more than ever.

The WisdomTree U.S. Value Fund seeks to capture that discipline by focusing not simply on low multiples, but on companies generating tangible returns for shareholders while trading at attractive valuations.

Having a shareholder yield that is approximately double that of traditional S&P 500 value indices shows how differentiated the positioning is.

Sometimes those companies will look like traditional value stocks.

Other times they may include world-class technology firms temporarily caught in a market rotation.

As investors wonder about the overall valuation levels of the market by and large, we think the close to 7% shareholder yield of WTV is far from expensive—it is a truly differentiated value portfolio.

1Source: Daly, L. (2026). The Magnificent Seven’s market cap vs. the S&P 500. The Motley Fool.

2Sources: WisdomTree, Factset. Rebalance effective at the close 2/12/2026. Holdings subject to change.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Value stocks, as a group, may be out of favor with the market and underperform growth stocks or the overall equity market. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.