DXJ

Japan Hedged Equity Fund

Published January 8, 2026

Research Analyst

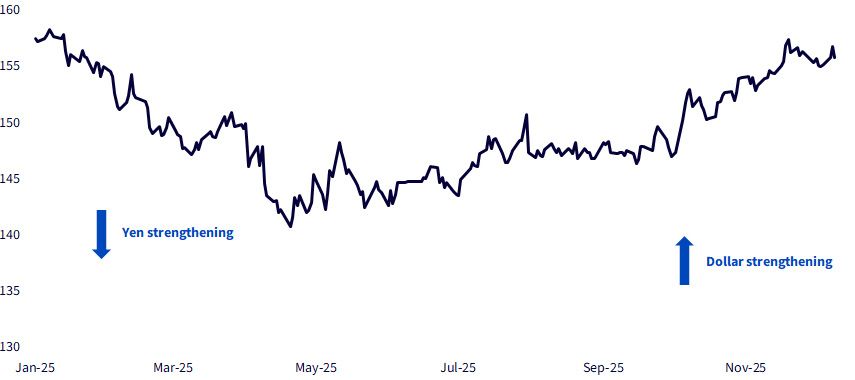

The yen experienced a dramatic round-trip in 2025.

In the spring, at the height of the "sell America" trade, the dollar was down more than 10% versus the yen.

As that trade faded, and as a new Prime Minister in Japan raised expectations of a weaker yen, the dollar recouped nearly all those losses.

At the time of this writing, the yen remains modestly stronger, just less than 1% year-to-date.

Sources: WisdomTree, FactSet. Data from 1/1/25–11/28/25.

Investing in foreign companies always comes with foreign currency risk.

Hedging the currency exposure—for example, selling the yen short in a forward currency contract—can neutralize the yen exposure within an equity allocation. In a year when the yen appreciates, currency hedging would typically be a headwind relative to unhedged exposures, as you don't get the benefit of the yen strengthening.

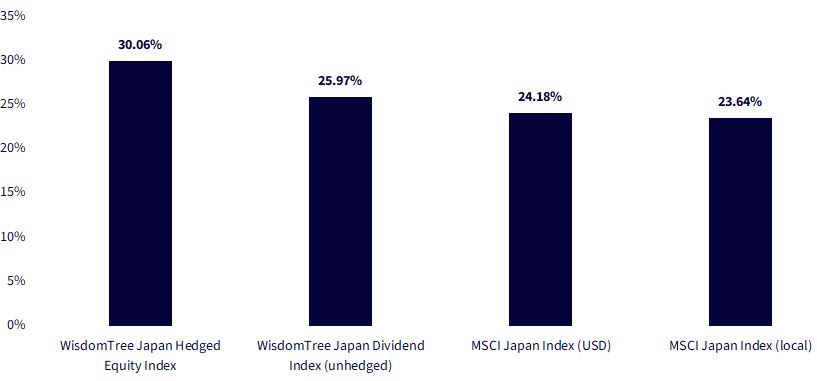

But 2025 is a unique example and really highlights a case for investors who don't have a strong view on the yen.

In a year when the yen is basically flat to slightly up, our currency-hedged Japan dividend Index has outperformed its unhedged counterpart by more than400 basis points (bps).

How, you ask? Because currency hedging not only aims to replicate local equity returns but also indirectly enhances returns via interest rate carry. When short-term rates in the U.S. are higher than those of the foreign currency, a U.S. investor earns the interest rate differential by being long the dollar and short the foreign currency.

As shown in the chart below, the WisdomTree Japan Hedged Equity Index, tracked by the WisdomTree Japan Hedged Equity Fund (DXJ), returned more than 400 bps this year compared to the local currency equity index, and more than 600 bps compared to its benchmark, the MSCI Japan Local Index, while the MSCI Japan Index returned 54 bps less in local returns than USD.

Sources: WisdomTree, MSCI, FactSet. Data as of 11/28/25. Past performance is not indicative of future results. You cannot invest directly in an index.

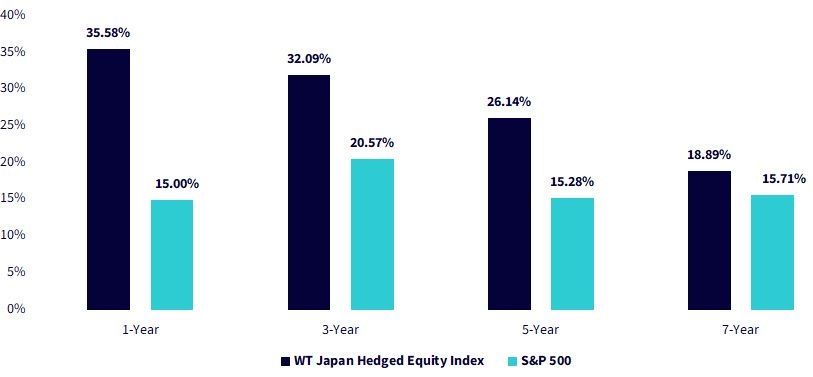

DXJ's performance leadership isn't limited to 2025. As the chart below shows, DXJ's Index has outpaced the S&P 500 across the one-, three-, five- and seven-year periods, an underappreciated trend that challenges the idea that Japan is only a tactical trade. This multiyear advantage reinforces the case for viewing Japan, and DXJ specifically, as a strategic allocation rather than a short-term opportunity.

Sources: WisdomTree, S&P, FactSet. Data as of 11/28/25. Past performance is not indicative of future results. You cannot invest directly in an index.

The case for DXJ goes beyond performance. Driven by strong corporate governance reforms and efforts to attract retail investors by the Tokyo Stock Exchange, Japanese companies have substantially hiked dividends and are on track to pay record total dividends for 2025.

Sources: WisdomTree, S&P, FactSet. Data as of 11/28/25. You cannot invest directly in an index.

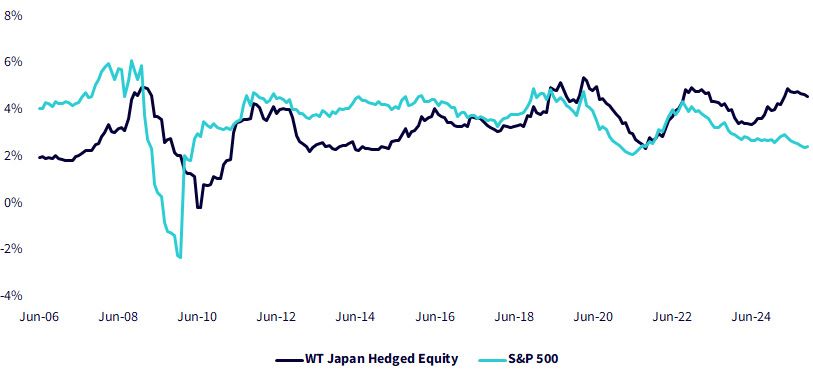

During most years following its inception, DXJ's Index lagged the S&P 500 Index in terms of shareholder yield, which we define as the sum of dividend yield and share reduction yield. There has since been a reversal of that trend in recent years, and the Index currently yields more than two percentage points more than the S&P 500.

Sources: WisdomTree, S&P, FactSet. Data from 6/30/06–11/30/25. You cannot invest directly in an index.

Importantly, this shift in shareholder yield has occurred while valuations remain meaningfully below those of U.S. equities. DXJ's Index currently trades at a significant discount to the S&P 500 Index—13 price-to-earnings (P/E) turns lower—while also delivering superior returns and paying shareholders more by every metric.

Sources: WisdomTree, S&P, FactSet. Data as of 11/28/25. Share reduction yield measures how much value a company returns to shareholders through share repurchases. Shareholder yield is the sum of dividend yield and share reduction yield. You cannot invest directly in an index.

Japan's market story in 2025 shows how much currency swings can shape investor outcomes and how effective hedging can be in navigating them. DXJ's strong performance this year, alongside its consistent leadership over longer horizons, reflects a renewed appreciation for Japan as more than a tactical allocation. For investors who do not have a strong view on the yen, DXJ offers a straightforward, strategic way to maintain exposure to Japan's equity market while reducing the uncertainty that comes from FX volatility.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Japan Hedged Equity Fund

Research Analyst

Hyun Kang joined WisdomTree in July 2022 as a Research Analyst. As a part of the Index team, he assists with the creation and maintenance of the firm’s indexes and supports the group’s research initiatives across various strategies. Hyun graduated from Carnegie Mellon University, with a B.S. in Business Administration and an additional major in Statistics and Machine Learning.