GDE

Efficient Gold Plus Equity Strategy Fund

Published November 18, 2025

Global Head of Research

There's a quiet revolution taking shape in portfolios. For decades, the 60/40 mix—60% equities, 40% bonds—was the shorthand for prudence, diversification and balance.1 But the regime that made that formula work—low inflation, stable growth and negative stock-bond return correlations—appears to have shifted. After 2022, investors tend to question how well bonds may dampen equity risk.2 In this new macro geometry, investors are re-examining what the "40" should really be. Morgan Stanley's latest Global Insights calls gold "an attractive hedge against fiscal largesse and geopolitics," noting its 50% rally year-to-date and near-zero equity correlation.3 Gold is not just a store of value; it's a statement about the limits of paper promises.

Allocating to gold in 2025 isn't about fear; it's about function. Exchange-traded fund (ETF) inflows of more than $10 billion in September alone show that institutional and retail investors alike are beginning to re-engineer portfolios for an era of structural deficits and active fiscal policy.4The asset's behavior has evolved: what was once a rate-sensitive trade has become a fiscal-risk hedge. Correlations with Treasury yields have flipped from deeply negative to positive, implying that gold now rises with, not against, higher long-term rates when those rates reflect sovereign stress.5 That's an inversion of an old mental model. Investors aren't running from volatility; they're buying the only liquid asset that sits outside the liabilities of any government or central bank.

The conceptual shift is profound. Instead of treating gold as an accessory to a portfolio, some strategists now treat it as a core sleeve of real assets—a 20% reallocation from the bond bucket that acknowledges diversification is no longer about opposites, but about orthogonality.6 For allocators, this isn't nostalgia for the gold standard; it's recognition that the architecture of portfolio resilience is changing. The new 60/20/20 mindset—equities, fixed income and real assets—may prove less a radical break than a quiet return to first principles: holding something that no one else owes you.

Europe's Gold Awakening, and Why It Matters for U.S. Investors

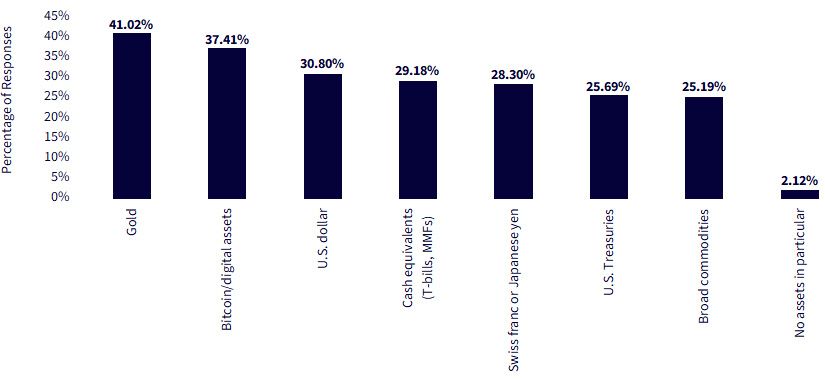

European investors are signaling something important about global portfolio behavior. In WisdomTree's 2025 Investor Survey of 802 European and U.K. participants, gold ranked as the top safe-haven asset, with 41% of respondents identifying it as their preferred store of value, well ahead of Bitcoin and the U.S. dollar. Perhaps more telling, average portfolio allocations to gold now stand at 5.7%, equal to holdings in developed-market sovereign debt. That balance suggests gold is no longer viewed as a fringe diversifier but as a mainstream, fixed component of institutional portfolios. In a globalized capital system, these regional shifts don't stay regional; European reallocations toward real assets inevitably influence global flows and price discovery, amplifying gold's liquidity and institutional relevance across markets.

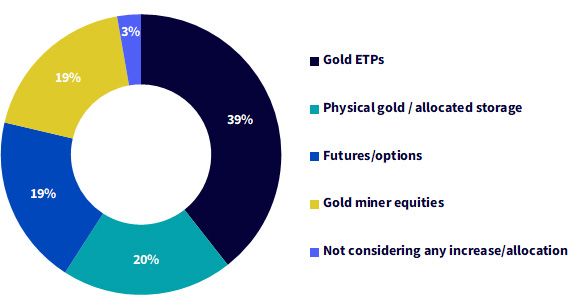

Equally notable is how investors are choosing to access gold. The survey shows nearly 40% favor exchange-traded products (ETPs), far surpassing preferences for physical bullion, futures or mining equities. The logic is pragmatic: ETPs deliver transparency, low cost and scalability that fit the modern portfolio construction toolkit. For U.S. investors, the European experience is an instructive case study. It suggests that the conversation about gold's role has moved beyond the "why" to the "how." As more allocators integrate gold as a core sleeve within real assets rather than a tactical overlay, the result may be a gradual convergence between U.S. and European portfolio design, one in which hard assets are recognized not as outliers, but as foundational pillars of modern diversification.

Figures 1 and 2 follow with an illustration of some of these results.

Figure 1: In a major risk-off environment, which asset do you view as the most reliable safe haven, if any? (Select up to three)

Source: WisdomTree survey of 802 institutional investors across European markets.

Figure 2: If you were to allocate/increase your exposure to gold, how would you most likely implement it?

Source: WisdomTree survey of 802 institutional investors across European markets.

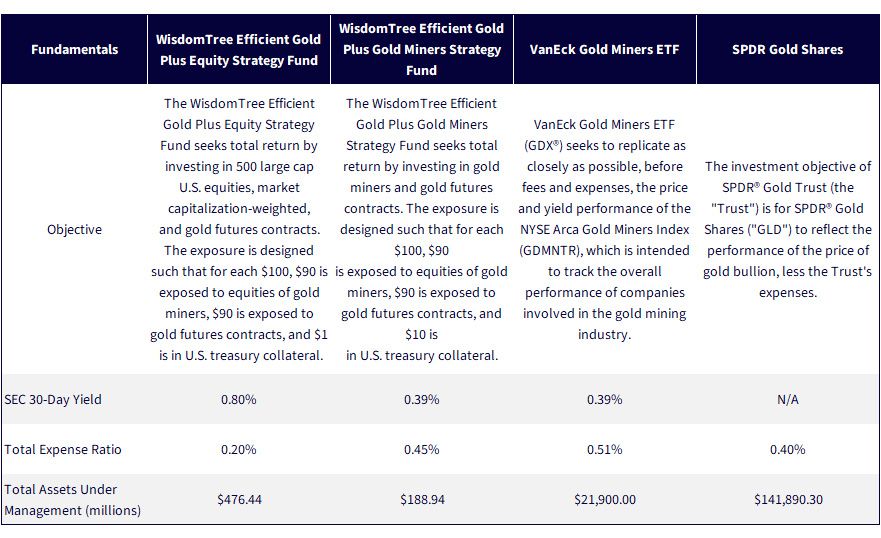

For decades, gold exposure came down to a binary choice: physical bullion or an ETF like the SPDR Gold Shares (GLD), where each share represents a portion of physical gold stored in a vault. There has also been the option to look at the VanEck Gold Miners ETF (GDX) for those seeking to own businesses directly connected to gold rather than the metal itself. But as portfolio construction evolves, investors are no longer confined to "either/or" decisions. The rise of capital-efficient strategies means a single allocation can now express multiple exposures—gold and miners, or gold and equities—within the same position. That shift reframes gold from a static diversifier to a dynamic building block capable of compounding its impact across asset classes.

In practical terms, this evolution is about optimization, not substitution. Investors seeking gold's defensive and inflation-hedging properties can now pursue those aims without sacrificing growth or efficiency. The question is no longer just how much gold belongs in a portfolio, but what kind of gold exposure delivers the most robust potential outcome.

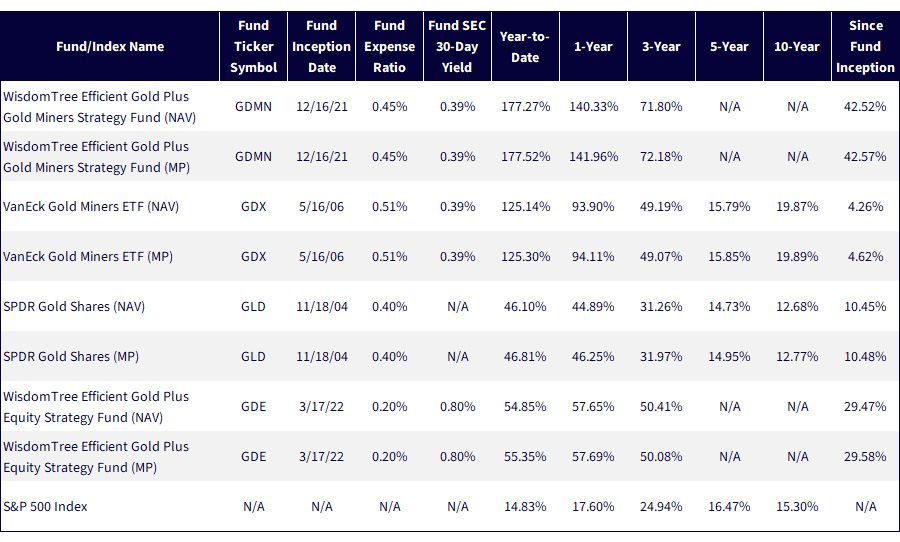

Sources: WisdomTree, FactSet; specifically, data from the Fund Comparison Tool in the PATH suite of tools, accessed 10/22/25, with returns as of 9/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the relevant ticker: GDMN, GDE, GDX, GLD.

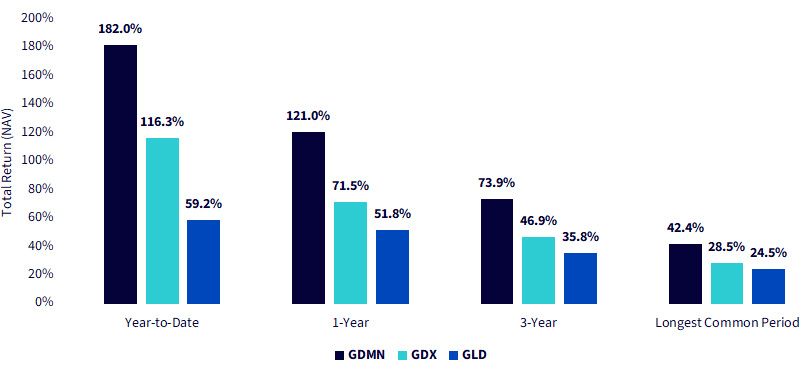

Performance data reinforces the structural advantage of capital-efficient design. As of late October 2025, GDMN has far outpaced both GDX and GLD, delivering a roughly 157% year-to-date total return, compared with 102% for GDX and 50.8% for GLD. Over every measured period—one-year, three-year and the longest common track record—GDMN consistently led the way. The visual arc of its performance tells the story: when gold rallied, GDMN captured the metal's momentum and the mining equity beta in one line item. That dual exposure has allowed it to magnify upside while maintaining liquidity and simplicity. It's a clear illustration that portfolio innovation isn't just about holding more; it's about doing more with the same dollar, a theme echoed across WisdomTree's capital-efficient strategies.

We'd recognize that 2025 is an example of a year when both gold and gold mining equities saw very strong positive returns. In years where both of these see negative returns, GDMN can be pulled downward further than either the price of gold or the performance of the miners alone. It's important to understand the uniqueness of roughly the first 10 months of 2025.

Figure 4a: Dual Exposure, Amplified Results

Sources: WisdomTree, FactSet; specifically, data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/5/25, with returns as of 11/4/25. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: GDMN, GDX, GLD.

Figure 4b:Capital Efficiency That Compounds Over Time

Sources: WisdomTree, FactSet; specifically, data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/5/25, with returns as of 11/4/25. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the relevant ticker: GDMN, GDX, GLD.

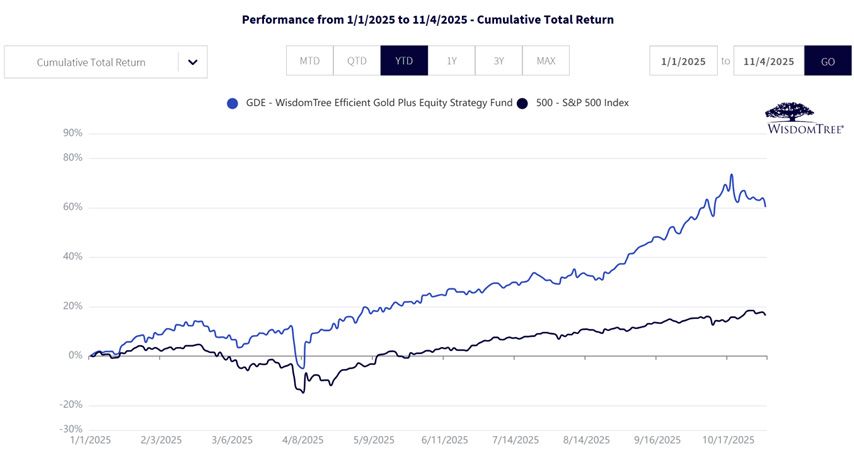

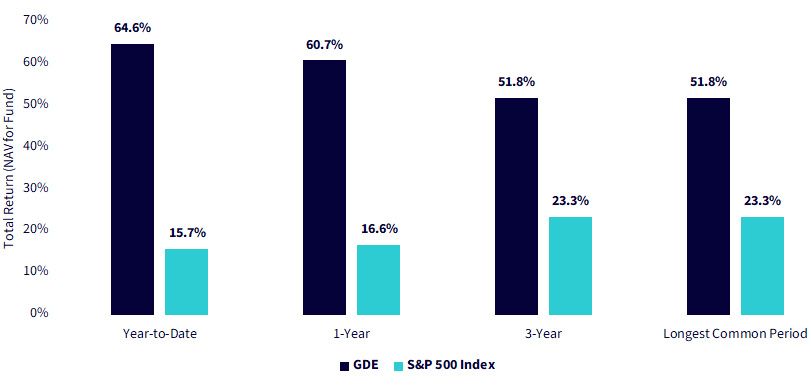

The performance story for GDE underscores the value of pairing equity growth with gold's defensive ballast inside a single structure. As of early November 2025, GDE delivered a 60.2% total return year-to-date, compared with 16.4% for the S&P 500 Index. Across every measured period—one-year, three-year and the longest common track record—GDE's returns have been roughly three times higher. The Fund's 90/90 design, full equity exposure plus an equivalent notional allocation to gold, has turned diversification into a source of incremental return rather than opportunity cost. When U.S. equities rallied, GDE captured that strength; when volatility or fiscal fears boosted gold, the portfolio's overlay amplified resilience. It's a live demonstration that diversification, when engineered efficiently, can compound performance rather than dilute it.

While the strategy was designed with "defensive ballast" of gold in mind, that's not what we experienced during roughly the first 10 months of 2025, when we saw equities largely rising and gold rising by even more. It's important to understand that GDE may experience years when both gold and equities drop, and how GDE may drop by more than either of the two individually. However, if history is any sort of guide, the more likely expectation would be equities going in one direction and gold remaining more stable or going in the other.

Figure 5a:Dual Exposure, Singular Performance

Sources: WisdomTree, FactSet; specifically, data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/5/25, with returns as of 11/4/25. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

Figure 5b: Consistent Outperformance across Market Cycles

Sources: WisdomTree, FactSet; specifically, data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/5/25, with returns as of 11/4/25. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

Conclusion: The New Role of Gold in Portfolios

Gold's resurgence in 2025 is more than a price story; it's a portfolio story. In a world where bonds no longer provide the ballast they once did, investors are rebuilding diversification from the ground up. The WisdomTree European Investor Survey showed a clear shift: allocators are not merely holding gold, they're institutionalizing it, embedding it beside sovereign debt and equities as a core element of long-term strategy. This reflects a broader evolution in portfolio design, away from static 60/40 constructs and toward capital-efficient, multi-exposure frameworks.

Recent volatility, where gold briefly surged past $4,300 per ounce before consolidating, hasn't shaken that conviction. Rather than a reversal, the pullback looks like a healthy pause in an ongoing structural advance. The drivers remain intact: a weaker dollar, falling bond yields, persistent inflation, elevated policy uncertainty and unresolved geopolitical risks.

Funds such as GDMN and GDE embody how investors can translate that macro view into portfolio reality. By layering exposures, gold, miners and equities, within a single, efficient structure, they blend growth and defense without fragmenting capital. The result is resilience built through integration, not isolation. As fiscal expansion, higher volatility and shifting correlations define the next market era, capital-efficient real-asset strategies may stand as the most disciplined way to stay both diversified and adaptive.

Sources: Specific Fund information pages for the specified Funds, with assets under management data current as of 10/21/25.

1 Source: N. Pham, B. Cui and U. Ruthbah, "The performance of the 60/40 portfolio: A historical perspective" [research report], CFA Institute, 2/18/25.

2 Source: "Return of the 60/40 portfolio" [PDF], Morgan Stanley Investment Management, 2025.

3 Source: Morgan Stanley Wealth Management, "Global Insights: Measuring metals' momentum, as gold shines, copper charges," Morgan Stanley Smith Barney LLC, 10/15/25.

4 Source: State Street Global Advisors, "SPDR® ETF chart pack: Key charts to help navigate the market" (October 2025 edition), State Street Corporation, 10/25.

5 Source: A. Marjolin, "Treasury yields and gold prices: Breaking expectations," S&P Global Commodity Insights, 3/25/25.

6 Source: M. Yasmin, "Morgan Stanley CIO favors 60/20/20 portfolio strategy with gold as inflation hedge" [news article], Reuters, 9/16/25.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ, and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund-to-fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

Material must be preceded or accompanied by a prospectus. Click the respective ticker to view the Fund prospectus: GDMN, GDE, GLD, GDX.

GDMN: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“gold miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of gold miners, the Fund may be susceptible to financial, economic, political or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic or regulatory conditions affecting that country or region, or emerging markets generally. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDE: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDX: An investment in the Fund may be subject to risks that include, but are not limited to, risks related to investments in gold and silver mining companies, special risk considerations of investing in Australian and Canadian issuers, foreign securities, emerging market issuers, foreign currency, depositary receipts, small- and medium-capitalization companies, equity securities, market, operational, index tracking, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, Fund shares trading, premium/discount risk and liquidity of Fund shares, and non-diversified and index-related concentration risks, all of which may adversely affect the Fund. Emerging market issuers and foreign securities may be subject to securities markets, political and economic, investment and repatriation restrictions, different rules and regulations, less publicly available financial information, foreign currency and exchange rates, operational and settlement, and corporate and securities laws risks. Small- and medium-capitalization companies may be subject to elevated risks.

GLD: Investing involves risk, and you could lose money on an investment in GLD.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Commodities and commodity-index-linked securities may be affected by changes in overall market movements, changes in interest rates and other factors such as weather, disease, embargoes or political and regulatory developments, as well as the trading activity of speculators and arbitrageurs in the underlying commodities.

Frequent trading of ETFs could significantly increase commissions and other costs, such that they may offset any savings from low fees or costs.

Diversification does not ensure a profit or guarantee against loss.

GLD has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents GLD has filed with the SEC for more complete information about GLD and this offering. Please see the GLD prospectus for a detailed discussion of the risks of investing in GLD shares. You may get these documents for free by visiting EDGAR on the SEC website at sec.gov or by visiting spdrgoldshares.com. Alternatively, GLD or any authorized participant will arrange to send you the prospectus if you request it by calling 866.320.4053.

The Marketing Agent for GLD, State Street Global Advisors Funds Distributors, LLC, is not affiliated with Foreside Fund Services, LLC, or WisdomTree, Inc.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.