Want to Go Long Duration? Not Recommended at This Time

Published November 5, 2025

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

- With the Federal Reserve cautiously navigating rate cuts and inflation remaining sticky, the macro environment suggests limited upside for long duration fixed income strategies.

- Treasury yields have moved within a volatile range over the last two years, and current levels near 4% imply that long duration positions would require a recession-level drop to be profitable.

- Historical yield curve dynamics point to a potential rise in the 10-Year Treasury yield, an unfriendly investment backdrop for re-allocating to long duration.

The age-old question in fixed income is when should I go long duration? Over the last two years, this has been an ongoing query for investors. More recently, with the Federal Reserve resuming rate cuts, it has come back on the front burner for sure.

In my opinion, when trying to determine where yields may be going, one should start at the cornerstone for rates, which is the macroeconomic and Fed landscape. Our baseline case is for the U.S. economy to continue on a modest/moderate growth path, with inflation proving to be sticky but not yet impacted in a meaningful way by tariffs. The Fed is still highlighting the potential employment risks of their dual mandate, but some voting members appear to be throwing some caution for another rate cut this year. Then, post-shutdown, we'll see how the jobs data looks for 2026 monetary policy decision making.

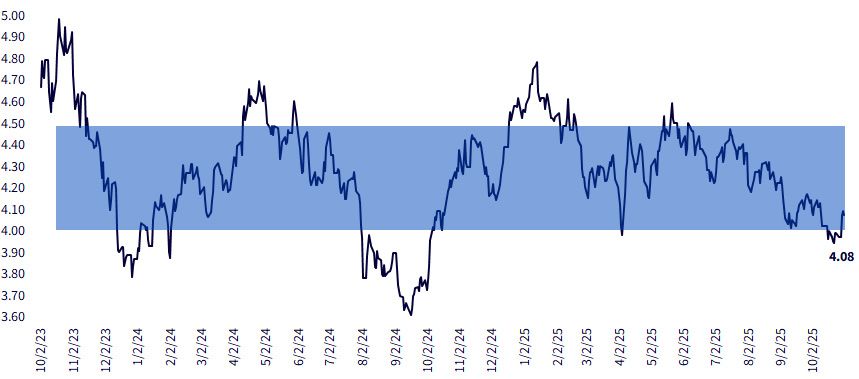

U.S. Treasury 10-Year Yield

Source: Bloomberg, as of 10/31/25.

The Fair-Trading Range…without a Recession

- Trading activity has been rather volatile over the last two years, with large movements in absolute yield (roughly 100-basis point (bps) swings from highs to lows) against the backdrop of a broader sawtooth pattern

- Going long duration inherently means you believe the economy is headed toward a recession with no inflationary pressures and that the UST 10-Yr yield is going to decline to the 2024 low of 3.6%, at a minimum

- An economic backdrop of moderate growth and no meaningful upward price pressures puts the UST 10-Yr yield in a fair-trading range of 4%-4.5%

- As of this writing, the UST 10-Yr yield is barely above the lower 4% boundary and was recently trading as low as 3.93%

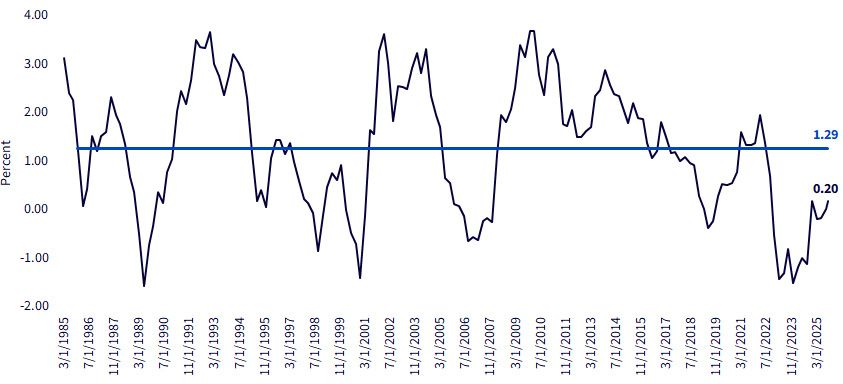

Fed Funds vs. UST 10-Year Yield

Source: Bloomberg, as of 10/31/25.

What Does History Tell Us

- Although the Treasury yield curve has un-inverted, it remains historically flat

- Following the Fed's most recent 25-bp rate cut, the spread between the new Fed Funds mid-point and the UST 10-Yr yield is around +20 bps

- The long run average for the Fed Funds/UST 10-Yr spread is +129 bps, or more than 100 bps above its current level

- A widening in the Fed Funds/UST 10-Yr spread to less than half, or roughly half, of its long-term average could place the 10-Year yield in the 4.5%-4.75% range

Conclusion

Given the track record for long duration over the last two-year period, as well as our macroeconomic outlook and relative value analysis, we would recommend holding off on the going-long duration trade.

Categories

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.