Bullets, Bandwidth and Backlogs: The Case for the WisdomTree Global Defense Fund

Published October 29, 2025

Christopher Gannatti, CFA

Global Head of Research

Samuel Rines

Macro Strategist, Model Portfolios

Key Takeaways

- As global conflicts expose severe underinvestment in defense infrastructure, multiyear contracts and rising backlogs signal a long-duration rearmament cycle investors can tap into now. It’s about building up a long-term algebra of deterrence rather than any specific current conflict.

- From Europe’s Zeitenwende to Asia’s accelerated defense buildout, capacity growth within the U.S. alliance system is creating durable earnings visibility across specialized manufacturers and suppliers.

- The WisdomTree Global Defense Fund (WDGF) targets high-purity defense companies positioned at critical chokepoints in modern warfare—from munitions to AI-driven software—offering investors scalable exposure to the new era of “deterrence as a service.”

The "peace dividend"1 is dead. It has been replaced by the "production dividend."And the rebuilding of allied arsenals, the factories behind them and the software definednervous systems that make them intelligent are beginning to come to life. Investors can already see the outcomes—long backlogs at primes, multiyear munitions contracts, satellite constellations ordered in tranches and allied governments reserving plant capacity the way utilities reserve power.

ADurable Deterrence

The underlying shifts can be broken down into three buckets:

1. Consumption shock. Real wars burn through equipment and ammunition faster than peacetime planning models assumed. That gap must be closed with expanded lines, not simply higher spending. In spring 2023, Ukraine was firing roughly 6,000–8,000 155mm shells per day—enough to match the entire U.S. pre-war monthly output (~14,000) in about two days—exposing a peacetime planning gap that can only be closed by new lines and plants, not just bigger budgets.2

2. Allied rearmament. Europe's shift from severe underinvestment to credible deterrence is real, and IndoPacific democracies are standing up capacity—South Korea exports, Japan remilitarizes, Australia invests and India accelerates domestic production. As one example, Germany's Bundestag passed a constitutional amendment allowing defense and security spending exceeding 1% of GDP to be exempt from the "debt brake" (Schuldenbremse), the fiscal rule that typically limits structural deficit to 0.35% of GDP. The package also establishes a €500 billion special fund for infrastructure and climate investments.3

3. Technology turnover. Drones, sensors, countersensors, software and space have changed the cost curve. In Ukraine, 117 commercial drones—each costing around $2,000—destroyed over $1 billion in Russian aircraft in a single operation.4 This illustrates how cheap, scalable payloads outperform legacy platforms. Old platformcentric procurement is giving ground to payloads, networks and software. That mix benefits companies that can iterate quickly and scale manufacturing—they are often companies with specialist moats or primes that control critical bottlenecks.

This is not a short-term, one-off. This investment cycle is years of investment to compensate for decades of under-investment.

From Promises to Profits

Sometimes the boring parts of the supply chains are the most important. Propellants, rocket motors, fuses and warheads have proved to be the gating items for modern arsenals. When nations buy interceptors, cruise missiles and artillery shells, they are buying energy and guidance. That favors suppliers scaling capacity under multiyear, takeorpay agreements.

- Rheinmetall has expanded its ammunition production capacity tenfold in just three years, and now expects "thousands and thousands" of tank and vehicle orders over the next 12 months—scale that should push unit costs down despite surging demand. The company forecasts €80 billion in new orders by mid-2026, up from a €55 billion backlog the prior year, underscoring how automation and volume can reverse the usual defense-inflation story.5

- BAE Systems and RTX (Raytheon) are central to resupplying guided and unguided munitions. RTX's missile franchises sit at the heart of layered air and missile defense; when interceptors are expended, orders follow.

- L3Harris absorbed Aerojet Rocketdyne—the U.S. solid rocket motor crown jewel—consolidating a critical chokepoint. Owning the motors means owning the pace of the missile supply chain.

- On the allied periphery, Poongsan (ammunition, South Korea) and Chemring (energetics and countermeasures, U.K.) represent the offU.S. capacity that NATO customers are increasingly reliant on.

You cannot rebuild a credible deterrent and reliable defense without investing in the fundamentals. When governments prioritize establishing and rebuilding stockpiles, the bottlenecks begin to emerge—propellants, motors, fuses—leading to potential pricing power and visibility. These dull parts of defense cannot be ignored.

The "Invisible Arsenal" and Backlog

Lethality is shifting from the platform you see to the sensors and waveforms you don't. Air defense is a radar and software problem; finding drones is a passivesensing problem; surviving is an electronicwarfare problem. These are not oneoff upgrades. As adversaries jam and spoof, software, firmware and electronics need constant refresh. That points to recurring revenue and margin durability.

This is not meant to imply that the large platforms are obsolete. They remain the anchor of allied combat power, and their production rhythms are finally adjusting to geopolitics. Many of these platform providers represent a stable of programs where backlog visibility can be measured in years, not quarters. And the visibility is important. The platforms are slow to certify, but once certified, they throw off decades of production, retrofit and sustainment to the bottom line. Backlog is safety; upgradeability is upside.

While NATO rearmament creates a credible deterrence to military action from primarily Russia, the buildout of capabilities by Asian countries is about deterring China. When it comes to the newly emergent great power competition, it is a race between China and the U.S. It is largely played out in three ways:

1. Sanctions and exportcontrol risk. The odds of value-destructive policy shocks for Chinese defense-adjacent equities are nontrivial. And the ability of the People's Republic of China should not be underestimated.

2 .Capital markets frictions. Index removals, audit standards and investment restrictions can prove difficult to anticipate.

3. Where capacity is actually growing for investors. The investable buildout is happening inside the U.S. alliance system and its close partners. South Korea is exporting at scale. India is ramping domestic champions. Europe is moving from intent to orders. Australia is embedding supply chains. That is likely to continue and should not be shrugged off.

The Risk of Peace

Defense stocks have rallied during periods in 2025, particularly when geopolitics turned for the worse. Peace, while the preferred state of the world, does not end the case for the long-term defense spending we are indicating. It refocuses it on earnings power and duration. Policy risk cuts both ways. Budget noise is perennial, but multiyear contracts for munitions and air defense are harder to reverse. The politics of stockpiles are different from traditional politics.Peace risk is the right kind of risk to own. If deterrence holds, arsenals still need to be rebuilt and rotated. If deterrence fails, demand accelerates. Either way, stockpiles do not build themselves.

Which brings us to the flywheel that is often missed:

1. Threat perception rises

2. Allies raise budgets, place multiyear orders

3. Industry invests in capacity (often with government support)

4. Unit costs fall and delivery confidence rises

5. More allies buy because supply is credible

6. Backlogs extend and cash flows stabilize

7. More capacity is justified.

For context, Europe is moving from "pledges" to orders. Germany's turning point ("Zeitenwende") started the psychological shift; Russia's sustained aggression locked it in. The NATO members that lagged are catching up, and the ones that led are rearming again. South Korea is an exporter with credibility on price and delivery. India is accelerating domestic programs and coproduction. Australia is reshaping its industrial base. Japan is breaking longstanding taboos and increasing spend. None of this requires guessing who wins the next election. It requires recognizing that allied democracies are rebuilding arsenals to buy time and stability, and that rebuilding is measured in years.

Deterrence as a Service

This is the focus of the WisdomTree Global Defense Fund (WDGF): deterrence as a service. Missiles that hit, sensors that see, software that decides, satellites that connect, and the components and services that keep it all running. It spans the alliance system but excludes China to reduce political tail risk and stay aligned with where capital and technology sharing are deepening.

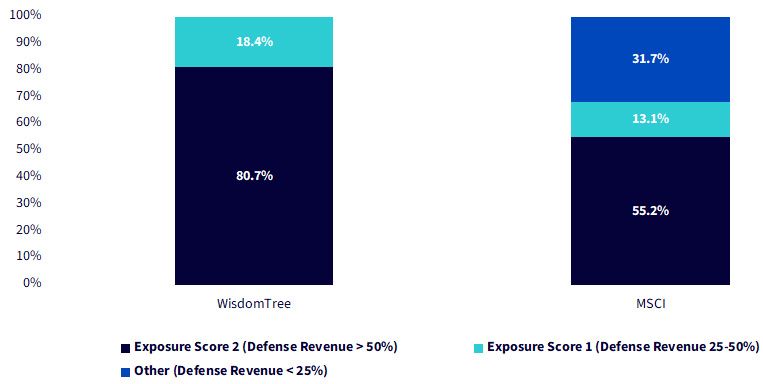

As with any thematic strategy, it is critical to look under the hood and understand that the businesses in the strategy have the desired exposure. In figure 1, we see that the WisdomTree Global Defense Index (which the WisdomTree Global Defense Fund is designed to track6) has more than 80% exposure to companies that derive more than 50% of their revenues from defense activities. The MSCI ACWI Aerospace and Defense Index only has 51.4% exposure to such companies.

To put an even starker point on it, the WisdomTree strategy does not include companies with less than 25% of their revenues from defense activities.

Figure 1: Invest Where the Defense Revenues Really Are

Sources: WisdomTree, FactSet. Holdings as of 6/30/25. Defense revenue exposure is sourced from multiple in-house and external sources. Data is as of the most recent rebalancing screen. You cannot invest directly in an index.

It's also true that, when many investors think of defense companies in 2025, the first thought is no longer Lockheed or Raytheon—it's Palantir. There is no question that Palantir has built an incredible business, but the company's valuation as of October 2025 is polarizing. Palantir's blistering growth—revenue up 48% year over year in Q2 2025 and quadruple its 2020 level—has investors valuing it at roughly $415 billion,7 a market cap that hearkens back to the peak multiples of the dotcom bubble's most extreme cases. Bulls argue that its unique moat—classified data access, high-level security clearances and AI-enabled analytics—positions it to dominate sensitive intelligence and defense software markets. Skeptics counter that at current valuations, Palantir would need to multiply revenue by 5.6 times while sustaining annual growth above 40% just to justify today's price, a bar even tech's most celebrated giants have rarely cleared.8

That is the essence of the investment case. The world has moved from a theoretical need for defense to a practical one. The practical world pays invoices. And the companies positioned at the bottlenecks, at the refresh points, and at the nexus of software and steel are set to turn that reality into durable cash flows.

For investors, this is a rare combination. Secular growth with government-level credit risk, global diversification within an alliance system and technology curves that are just starting to bend. The WisdomTree Global Defense Fund is built to track that bend—across bullets, bandwidth and the backlogs that make deterrence credible.

1 "Peace dividend," Fortune, 1968. This is often cited as the first use of this term.

2 Source: N. Robertson, "Production of Key Munition Years Ahead of Schedule, Pentagon Says," Defense News, 9/15/23.

3 Source: "German Parliament's Upper House Gives Final Approval to Huge Defense and Borrowing Package," The Associated Press, 3/21/25.

4 Source: D. Michaels, "Ukraine's Drone Attack Exposes Achilles' Heel of Military Superpowers," The Wall Street Journal, 6/6/25.

5 Source: L. Pitel, "Rheinmetall Chief Says Tanks to Get Cheaper as Defence Spending Surges," Financial Times, 8/12/25.

6 The WisdomTree Global Defense Fund is designed to track the total return performance, before fees and expenses, of the WisdomTree Global Defense Index.

7 Source: Bloomberg, with data as of 10/22/25.

8 Source: "Palantir Might Be the Most Over-Valued Firm of All Time," The Economist, 8/12/25.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. To the extent the Fund invests a significant portion of its assets in securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. Investments in non-U.S. securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Investments in non-U.S. securities also may be subject to withholding or other taxes and may be subject to additional trading, settlement, custodial and operational risks. These and other factors can make investments in the Fund more volatile and potentially less liquid than other types of investments. These risks may be heightened to the extent the Fund invests in companies domiciled in or otherwise tied to developing or emerging market countries. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributors

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Samuel Rines

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.