Central Banks, Gold and the Shifting Foundation of Reserves

Published September 23, 2025

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- In a historic reversal, 2025 marks the first time in decades that central banks hold more reserves in gold than in U.S. Treasuries, signaling greater questioning around dollar hegemony1 and rising demand for geopolitical hedges.

- Gold’s greater than 30% year-to-date surge positions 2025 among the top 10 performing years since 1971, reshaping its role from a slow-moving diversifier to a high-volatility performer akin to the 1970s.

- Investors can now access gold’s upside without sacrificing equity exposure through WisdomTree’s efficient core strategies GDE and GDMN, offering $180 of notional exposure per $100 invested.

From Bretton Woods to a New Reserve Reality2

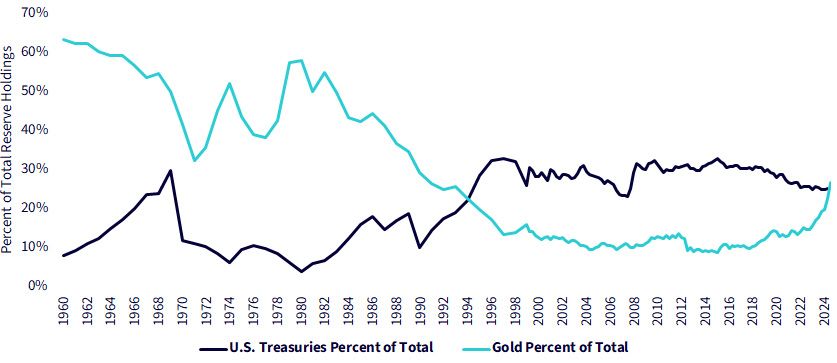

Over the past several decades, the composition of central bank reserves has undergone a structural transformation. In the mid-20th century, gold accounted for more than 60% of global reserve holdings, while U.S. Treasuries represented less than 10%. The Bretton Woods system3 anchored this hierarchy, but once it collapsed in the early 1970s, the world transitioned toward fiat-based reserves. This shift, alongside the deepening liquidity of U.S. government bonds, gradually pushed Treasuries into the dominant role. By the 2000s, gold's share of official reserves had dwindled to barely 10%, while Treasuries hovered closer to one-third of the total. The prevailing narrative was simple: gold was relic, Treasuries the cornerstone.

That narrative is now cracking. Persistent central bank gold purchases, particularly from emerging markets, paired with a powerful rally in gold prices have led to a remarkable milestone: central banks now hold a larger share of reserves in gold than in U.S. Treasuries. This reversal reflects not only portfolio rebalancing, but also geopolitical hedging and a questioning of the long-term role of the dollar.

The Story behind the Shift

- From dominance to decline: Gold once represented the overwhelming majority of central bank reserves in the post–Bretton Woods era, but its share steadily eroded as U.S. Treasuries rose to dominance.

- A multi-decade reversal: Since the 2000s, gold's role has been quietly rebuilt, while Treasuries have faced erosion from rising U.S. debt levels, geopolitical frictions and questions around dollar hegemony.

- The crossover moment: In 2024–2025, for the first time in roughly three decades, gold again surpassed Treasuries in central bank reserve share, signaling one of the most consequential portfolio rebalancings in modern history.

Figure 1: Gold Surpasses U.S. Treasuries in Central Bank Reserves for the First Time in Decades

Sources: World Gold Council (2025), "Central banks' gold as percentage of total international reserves," extracted from IMF International Financial Statistics (IFS), retrieved from World Gold Council Goldhub data portal; International Monetary Fund (2025), "International Financial Statistics (IFS) and Currency Composition of Official Foreign Exchange Reserves (COFER)," via Central Banking's "Appendix 3: Reserve statistics," Central Banking, retrieved from Appendix 3: Reserve statistics, (Central Banking, 2025). Past performance is not indicative of future results.

Gold's Returns in Context: When 30% Matters

Historical Extremes: Where 30% Stands

Gold's track record is filled with both fireworks and flameouts. The best year in modern history was 1979 (+126%) amid oil shocks,4 inflation and dollar stress. The worst, 1981 (-33%), came as Volcker's policies at the U.S. Federal Reserve sought to crush inflation.5 Against this backdrop, 2025's ~30% year-to-date surge already puts it among the 10 best annual returns since 1971, even with four months left in the year.

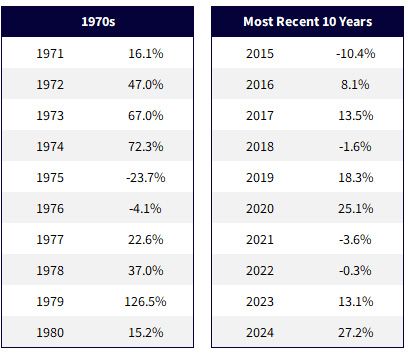

Figure 2a: Gold's Rollercoaster (Best & Worst Years since 1971)

Source: Bloomberg. 1971 marked the end of the dollar's peg to gold, as on August 15, 1971, President Richard Nixon announced the "Nixon Shock": the U.S. would suspend the dollar's convertibility into gold. This was meant as a temporary measure but became permanent. Past performance is not indicative of future results.

The 1970s Parallel: Volatility as the Norm

The 1970s were an archetype for gold bull markets. Between 1972 and 1974, gold notched three blockbuster years before suffering declines in 1975 (-24%) and 1976 (-4%), only to rocket again in 1979 (+126%). Gold in such regimes doesn't trend neatly upward; it convulses. If 2025 continues its trajectory, the parallels related to gold's appreciation in that decade might grow stronger.

The Modern Decade: Resetting Expectations

By contrast, the past 10 years show a muted pattern. The mid-2010s saw three consecutive annual losses (2013–2015). Even the pandemic surge in 2020 capped at +25%. Today's nearly +30% move in just eight months signals a break from that pattern: less the slow-moving diversifier of recent memory, more the volatile hedge reminiscent of the 1970s.

Figure 2b: The 1970s as Compared to the Most Recent 10 Years

Source: Bloomberg, specifically the XAU Currency price series. 1971 marked the end of the dollar's peg to gold, as on August 15, 1971, President Richard Nixon announced the "Nixon Shock": the U.S. would suspend the dollar's convertibility into gold. This was meant as a temporary measure but became permanent. Past performance is not indicative of future results.

How Investors Can Position: Efficient Core and Beyond

If the backdrop is extraordinary, the next logical question is: how should investors gain exposure to gold? The reality is there is no single way, each strategy carries its own trade-offs. At WisdomTree, we think about gold not as an isolated sleeve, but as part of an efficient core that integrates with equity exposure.

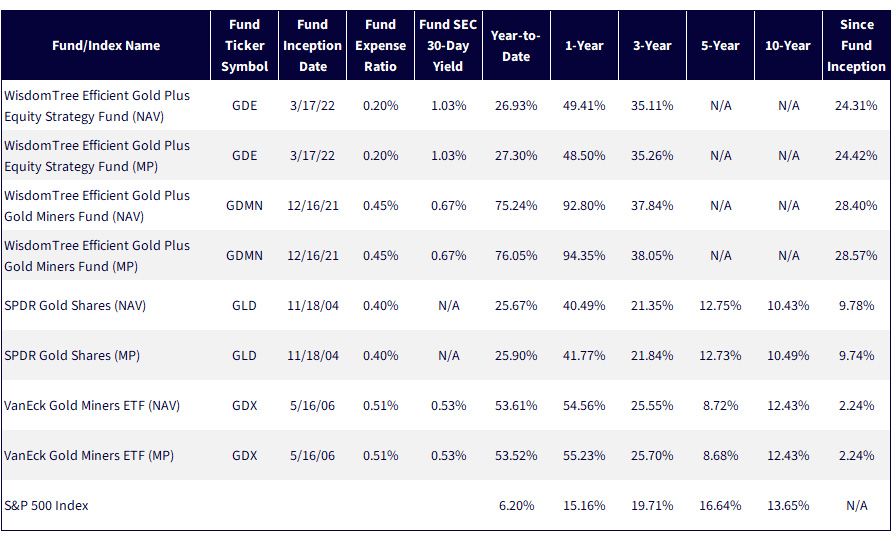

- WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE): 90% U.S. large-cap equities + 90% gold futures = $180 notional exposure for every $100 invested. This structure avoids the "either-or" trade-off between equities and gold, delivering both.

- WisdomTree Efficient Gold Plus Gold Miners Fund (GDMN): 90% gold miners + 90% gold futures = $180 notional exposure for every $100 invested. Designed for investors with a view on gold's trajectory and interest in combining the metal's potential price appreciation with miners' operating leverage.

Alongside these efficient core strategies, investors should recognize the scale of two familiar benchmark strategies for those considering different avenues of exposure related to gold:

- SPDR Gold Shares (GLD): The world's largest exchange-traded product backed by physical gold.

- VanEck Gold Miners ETF (GDX): The largest ETF tracking the total return performance of gold mining equities.

And, of course, the S&P 500 Index remains an important benchmark for most portfolios.

Figure 3: Standardized Performance

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 8/28/25, but showing returns for the period ended 6/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the relevant ticker: GDMN, GDE, GLD, GDX.

What 2025 Tells Us about Performance

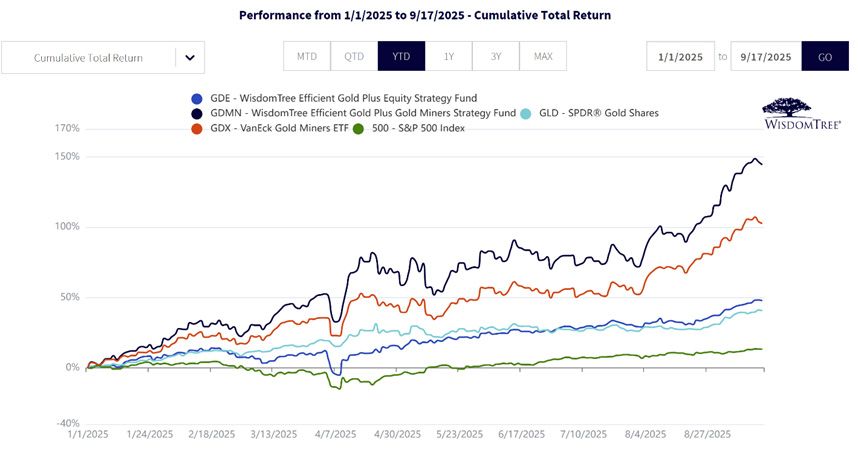

- A year of outsized gains: Gold's 2025 rally has been the common denominator, lifting GLD, GDX and the efficient core strategies GDE and GDMN all ahead of the S&P 500.

- But not every year looks like 2025: Gold's price has often delivered years of flat returns or even declined. Efficient core structures are designed with this reality in mind, offering potential upside when gold is strong but then providing potential portfolio resilience when it is not.

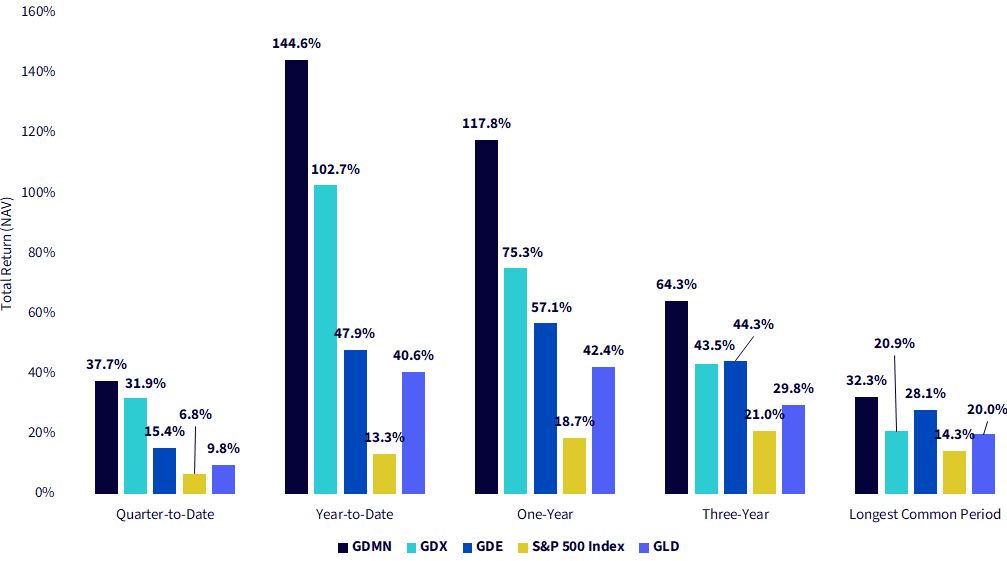

Figure 4: Gold and Equity Strategies Ride 2025's Rally

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 9/18/25, but showing returns for the period ended 9/17/25. NAV denotes total return performance at net asset value. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the relevant ticker: GDMN, GDE, GLD, GDX.

Live Performance across Horizons

- 2025 as an outlier: GDMN has surged more than 140% year-to-date, with GDX also strong, and even GDE producing standout returns. This environment is unusual, with gold strength amplifying results across exposures.

- Persistence vs. cyclicality: As the length of the performance window grows, results appear to normalize, but we note that 2025's strength is showing up across the range. For example, over the period since GDE's inception, the longest we can show across these strategies, GLD's annualized return was roughly 20% and outpaced that of the S&P 500 Index. History has shown that this has not been the case over most longer-run periods, and it puts an exclamation point on how exciting this particular period has been for gold.

- Efficient core durability: Across the longest common period, GDE and GDMN hold their ground versus GLD and GDX.

Figure 5: Performance Snapshots, from Quarter to Cycle

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 9/18/25, but showing returns for the period ended 9/17/25. Longest Common Period is from GDE inception, 3/17/22. NAV denotes total return performance at net asset value. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the relevant ticker: GDMN, GDE, GLD, GDX.

Conclusion: Beyond "Just Gold"

Gold's 2025 surge has been historic, but the real lesson isn't simply that gold can deliver powerful returns; it's how investors choose to access it. Traditional approaches like GLD (physical gold) and GDX (gold miners) remain important tools, but they force a choice: hold gold instead of equities or bet on miners instead of broader markets.

The efficient core framework changes that equation. With GDE, investors don't have to sacrifice equity exposure to add gold; both sit side-by-side in a single allocation, creating a portfolio cornerstone that adapts to multiple market environments. With GDMN, investors can express a conviction on gold by pairing price appreciation with the operating leverage of miners, again in one integrated structure. Both strategies elevate gold from a niche sleeve to a core holding with balance, efficiency and scale.

That's the story 2025 is telling us: gold is no longer confined to being an alternative on the edges of a portfolio. With efficient core solutions like GDE and GDMN, investors can capture its renewed strategic role, without the trade-offs of "either-or" positioning.

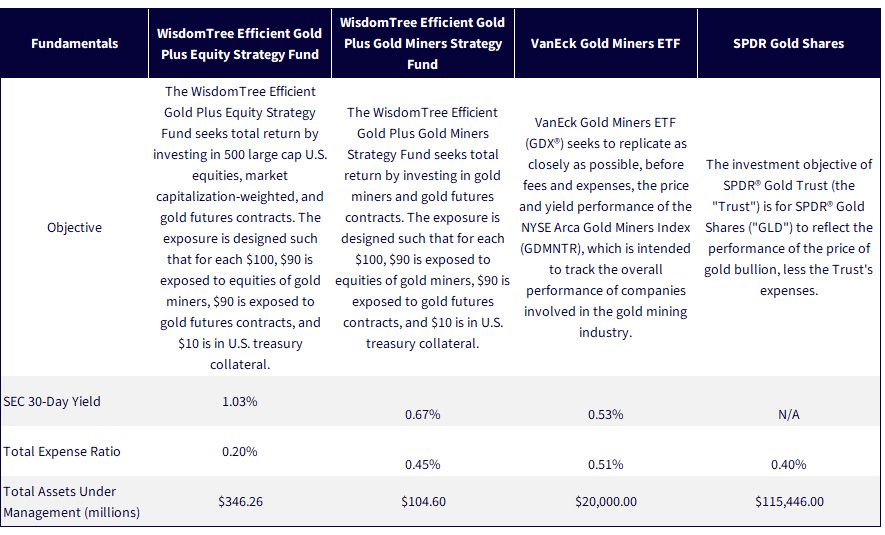

Figure 6: Additional Information

Sources: Specific Fund sponsor websites, with Assets Under Management data current as of 9/17/25.

1 Hegemony = leadership or dominance, especially by one country or social group over others.

2 Unless otherwise noted, the sources for any discussion of reserve composition related to gold would be: Sources: World Gold Council (2025). Central banks' gold as percentage of total international reserves, extracted from IMF International Financial Statistics (IFS). Retrieved from World Gold Council Goldhub data portal; International Monetary Fund (2025). International Financial Statistics (IFS) and Currency Composition of Official Foreign Exchange Reserves (COFER), via Central Banking’s “Appendix 3: Reserve statistics.” Central Banking. Retrieved from Appendix 3: Reserve statistics. (Central Banking, 2025).

3 The Bretton Woods system was the international monetary order established in 1944 at a conference in Bretton Woods, New Hampshire. Its design aimed to bring post–World War II economic stability, rebuild global trade, and prevent the competitive currency devaluations that had destabilized the 1930s.

4 The 1979 oil price shock was the second major oil crisis of the 1970s, following the first in 1973. It was triggered primarily by the Iranian Revolution, which disrupted global oil production and raised fears of prolonged shortages.

5 The Fed raised the Federal Funds Rate to unprecedented levels, peaking around 20% in June 1981.

Important Risks Related to this Article

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ, and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund-to-fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

Material must be preceded or accompanied by a prospectus. Click the respective ticker to view the fund prospectus: GDMN, GDE, GLD, GDX.

GDMN: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“gold miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of gold miners, the Fund may be susceptible to financial, economic, political or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic or regulatory conditions affecting that country or region, or emerging markets generally. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDE: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDX: An investment in the Fund may be subject to risks that include, but are not limited to, risks related to investments in gold and silver mining companies, special risk considerations of investing in Australian and Canadian issuers, foreign securities, emerging market issuers, foreign currency, depositary receipts, small- and medium-capitalization companies, equity securities, market, operational, index tracking, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, Fund shares trading, premium/discount risk and liquidity of Fund shares, non-diversified and index-related concentration risks, all of which may adversely affect the Fund. Emerging market issuers and foreign securities may be subject to securities markets, political and economic, investment and repatriation restrictions, different rules and regulations, less publicly available financial information, foreign currency and exchange rates, operational and settlement, and corporate and securities laws risks. Small- and medium-capitalization companies may be subject to elevated risks.

GLD: Investing involves risk, and you could lose money on an investment in GLD.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Commodities and commodity-index-linked securities may be affected by changes in overall market movements, changes in interest rates and other factors such as weather, disease, embargoes or political and regulatory developments, as well as the trading activity of speculators and arbitrageurs in the underlying commodities.

Frequent trading of ETFs could significantly increase commissions and other costs, such that they may offset any savings from low fees or costs.

Diversification does not ensure a profit or guarantee against loss.

GLD has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents GLD has filed with the SEC for more complete information about GLD and this offering. Please see the GLD prospectus for a detailed discussion of the risks of investing in GLD shares. You may get these documents for free by visiting EDGAR on the SEC website at sec.gov or by visiting spdrgoldshares.com. Alternatively, GLD or any authorized participant will arrange to send you the prospectus if you request it by calling 866.320.4053.

The Marketing Agent for GLD, State Street Global Advisors Funds Distributors, LLC, is not affiliated with Foreside Fund Services, LLC, or WisdomTree, Inc.

Categories

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.