Surprisingly Positive Tariffs

Published July 28, 2025

Samuel Rines

Macro Strategist, Model Portfolios

Key Takeaways

- With August tariff extensions looming, several major companies are now guiding for reduced tariff impacts, a shift that has helped boost market sentiment this earnings season.

- Firms like Johnson & Johnson and 3M have moved from worst-case tariff scenarios to improved earnings guidance, suggesting earlier fears were overstated.

- As pricing strategies and supply chain adaptations take hold, investors should watch for potential upside surprises in companies that previously priced in heavy tariff damage.

Few Sentence Take (FaST): The August tariff extension is two weeks away. But earnings season is telling us a few important things about the current state of affairs. Many of the companies that provided guidance for tariff impacts in the past are guiding away some of the impact in the future. Markets like increased guidance.

Many people are fans of having four seasons. This author is a fan of four seasons as well—earnings seasons. The informational content is simply far too valuable to anyone who wants to know what the macro is likely to do.

First, it is worthwhile to highlight some takeaways from the previous weeks. The tariff game plan for corporate America appears to be a variation of:

- Gain clarity on the effects of tariffs across revenues and margins.

- Mitigate through supply chain actions, promotions (pricing lite) and pricing actions (explicit price increases).

- Supply chain actions are underway, but the promotional cutting and price hiking are coming.

That is useful for understanding the way some of the economic data is likely to play out over the next several months. There will be whipsaws in the data—particularly goods inflation. But that is only part of the overall equation of understanding the tariff impacts and ripples for markets.

If you have a "full price" item that is $50, you might sell it, on average, for $45 due to discounting the product by 10%. Cutting discounts from 10% to 5% leads to an average selling price that increases by 5.6%. Combining lower discounts with an increase in the "full price" sticker, and that gets to some interesting top-line characteristics, even losing a bit of volume.

That is the story to watch over the next several quarters. Some will execute. Some will not.

Then there are the companies with "too much tariff" priced in. And those are the ones to watch. Again, there is a particular cadence to the companies:

- Guided for the worst of all possible worlds

- Found out it was not quite that bad after various tariff announcements and internal adjustments.

- Are now guiding some of the impact back to the bottom line.

Johnson & Johnson is one of the better examples.

This is due to efficiency programs designed for margin improvement as well as nonrecurring one-time IP R&D charges that occurred in the second half of 2024. This expected improvement also takes into consideration the dilution from the intracellular transaction as well as what we know today about the impact of tariffs on our business. During our first quarter conference call, we anticipated an impact from tariffs in 2025 to be approximately $400 million.

Based on the current tariff landscape, we now anticipate the impact to be approximately $200 million exclusively related to our med tech business. We will look to reinvest the differential to continue to accelerate our pipeline and further power the launch of our new products, those on the market with new indications and those with near-term and painted approvals. We continue to monitor what the future years impact could be from tariffs on our business.1

That is a 50% decrease in the tariffs' impact for the company. And it is not alone.

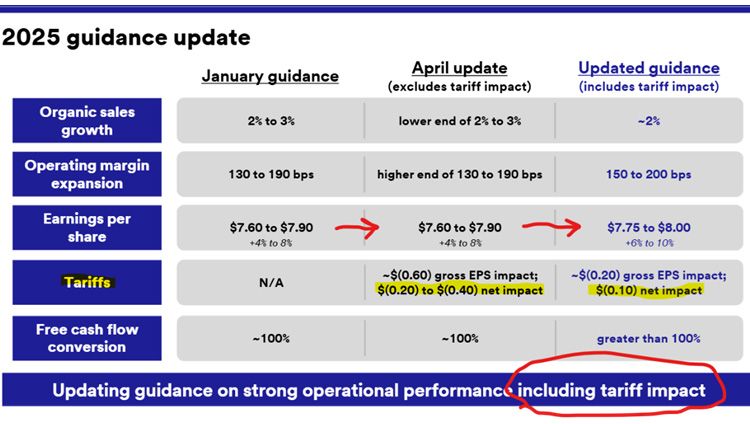

Source: 3M earnings presentation, 7/18/25 (emphasis added).

There is also 3M. Guiding down the tariff impact from $0.20 to $0.40 of net impact to $0.10 might sound trivial. But the interaction of expecting a larger impact and preparing for it led 3M to guide earnings higher than its pre-tariff (January) expectation.

This is not going to be the case for everyone. But it will be the case for many who guided to the worst of all possible worlds. For some, the dark night of earnings is over. And that could lead to some interesting dynamics through the remainder of earnings season.

A few of the companies to watch in the coming weeks for clarity are PG, DE and KMB:

So category growth, question mark in the short term. Midterm, we expect it to return to 3% to 4% growth rate. The levers for us are the same levers that we talk about in our integrated strategy. I think the tariff impacts that are visible to us right now at a gross level are in the range of $1 billion to $1.5 billion. So it's not immaterial. For us to offset those in the short term, we have to consider productivity, which we will double down on, and we have a very strong productivity plan over the next 3 years that I feel very bullish about.2

Josh Beal

Director of Investor Relations

Dave, I'll walk you through a couple of things here. I mean, I think if you think about first and foremost, the impact of tariffs, as we said, it is $500 million for the full year, incurred $100 million in the second quarter, it's about $400 million the rest of the year. The full year impact on the equipment operations for those -- for that tariff impact of 5 -- $500 million is about 1 point to 1.5 points. But again, being so back-end loaded in the back half margins, that's 2 to 2.5 points in the back half.3

As Mike indicated, in the last 20 days, we've had to reflect cost impacts of actions on 3 fronts, which also include the depth of the actions. First is the aggregate U.S. tariffs on China of 145%. This is driving about 2/3 of the $300 million gross impact that we have shared today. That's largely on finished goods, for your ask of the breakdown. The other element is U.S. reciprocal tariffs, to Mike's point about breadth and reach, and that's about 10% that have been put in place on other countries which we source from. And this is representing about 10% of the $300 million impact. And then lastly is the set of retaliatory tariffs that have been announced by other countries on the U.S., and this is representing around 25% of that $300 million.

We're working fast through actions to mitigate these costs. And frankly, the learnings that we had in the '21, '22, '23 cycle have come in pretty handy.

There are plenty of companies with a tariff overhang. For some, that hangover will be warranted. But others will emerge on the other side with better outcomes. It may be surprising to see who the winners are at the end of earnings season. With tariff impacts being mitigated and pricing plans to come, this earnings season could be surprisingly positive.

1 Source: Johnson & Johnson earnings call, 7/18/25 (emphasis added).

2 Source: Proctor & Gamble earnings call, 4/24/25 (emphasis added).

3 Source: Deere & Company earnings call, 5/15/25 (emphasis added).

4 Source: Kimberly-Clark earnings call, 4/22/25 (emphasis added).

About the contributor

Samuel Rines

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.