QHY

U.S. High Yield Corporate Bond Fund

Published June 24, 2025

Director, Fixed Income

When markets feel shaky, investors naturally look for strategies built on stability and quality. Building on our last post, "Built for the Tough Times: QHY's Edge in Today's High-Yield Market," we're excited to share an update on the WisdomTree U.S. High Yield Corporate Bond Fund (QHY). In the sections that follow, we'll remind the readers of the enhancements we've made, explain why they matter and show how they've helped us deliver stronger results.

In the wake of COVID-19, many weaker companies stayed afloat thanks to support from the Federal Reserve and other central banks. To keep pace with changing market dynamics and fine-tune our risk/return profile, we added equity return momentum to our tool kit alongside our long-term free cash flow signals. Rolled out in our November 2024 rebalance, this new layer gives us a more timely read on an issuer's financial health—helping us spot and sideline potential troublemakers before their fundamental weaknesses even register.

Momentum has long been a go-to tool in equity markets for spotting turning points and riding out volatility. We zeroed in on equity momentum, rather than debt momentum, because it cuts through the noise and gives us a clearer read on how the market feels about a company. In our backtests from 2016 through mid-2024, the issuers in the top momentum quintile (and especially those in the top 10%) consistently exhibited strong risk-adjusted results, proving that momentum can be a powerful complement to our fundamentals.

We balance momentum's benefits against turnover by zeroing in on the most extreme signals—only issuers in the top or bottom 10% of equity momentum ratings make the cut. That way, momentum serves as a powerful reality check on our fundamentals:

One of the most important tweaks we made was knowing when to dial back the momentum signal. By tracking 12-month momentum, we stay grounded in longer-term trends and avoid overreacting to every short-lived swing.

Our blend of deep fundamental research and well-timed momentum signals is proving its worth. Since our November 2024 rebalance, the enhanced high-yield strategy, the "Current Strategy," has outperformed the previous version by 37 basis points.

Source: WisdomTree, as of 05/30/25. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

A couple of factors have underpinned the strategy's improved results:

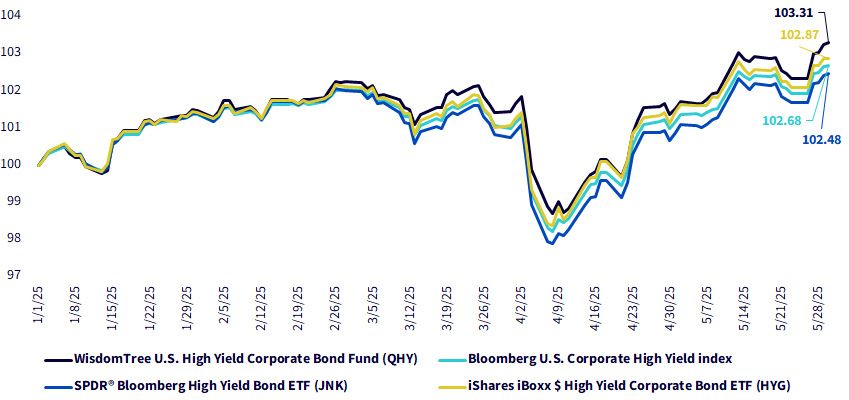

Our improved strategy hasn't just outpaced the previous approach; it's also held its own against peers and the broader market. Year-to-date, the Fund has beaten the Bloomberg U.S. Corporate High Yield Index by 63 basis points. We believe our emphasis on higher-quality bonds as well as more timely signals, both versus peers and the broader index, have been a major driver of the outperformance.

Source: Bloomberg, WisdomTree, as of 05/30/25. The funds were chosen for comparison due to their similar investment objectives. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the respective ticker: QHY, JNK, HYG.

When markets become stressful, it's the weaker issuers that usually suffer the most. By keeping quality at the forefront, and layering in timely equity momentum signals, we've been able to steer through recent ups and downs with greater confidence. Shifting toward higher-quality issuers and using momentum as an early warning system has helped QHY deliver stronger risk-adjusted returns.

For investors who want exposure to high yield without reaching for riskier credits, a disciplined, quality-first approach like QHY can offer a steadier path. We believe the recent changes to the strategy will leave us better positioned for whatever lies ahead. And ready to pursue strong, risk-adjusted performance in any market environment.

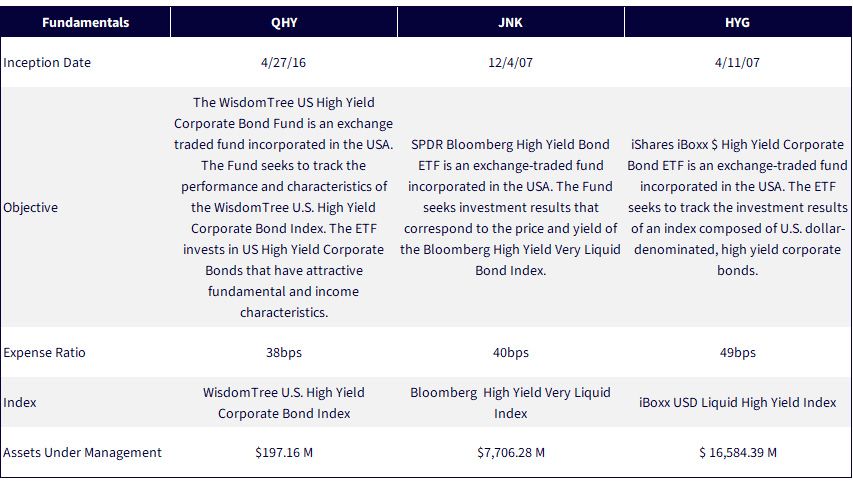

Sources: WisdomTree, State Street, iShares, as of 6/20/25.

For current holdings, click the respective ticker: QHY, JNK, HYG. Holdings are subject to risk and change.

QHY: There are risks associated with investing, including the possible loss of principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Please read the Fund's prospectus for specific details regarding the Fund’s risk profile.

JNK: The Fund is classified as “diversified” under the Investment Company Act of 1940, as amended (the “1940 Act”); however, the Fund may become “non-diversified,” as defined under the 1940 Act, solely as a result of tracking the Index (e.g., changes in weightings

of one or more component securities). When the Fund is non-diversified, it may invest a relatively high percentage of its assets in a

limited number of issuers.

Passively managed funds invest by sampling the index, holding a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. This may cause the fund to experience tracking errors relative to performance of the index. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETFs net asset value. Brokerage commissions and ETF expenses will reduce returns.

HYG: Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Diversification may not protect against market risk or loss of principal. Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the fund. Any applicable brokerage commissions will reduce returns

U.S. High Yield Corporate Bond Fund

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.