OPPJ

Japan Opportunities Fund

Published June 2, 2025

Global Head of Research

Macro Strategist, Model Portfolios

Europe is in the early innings of a renaissance. Germany’s DAX index just hit record highs, helped by revived enthusiasm for defense and infrastructure and reduced trade tension.1 From bilateral trade breakthroughs to potential de-escalation in U.S.-EU tariff battles,2 the policy pendulum is swinging from fragmentation toward cooperation. These aren’t abstract headlines—they are real forces influencing equity risk premiums, cash flow visibility and strategic capital plans.

The most startling example of this pivot is Germany. Once the center of fiscal discipline, it is now excluding defense spending from its budget rules. Chancellor Merz put it bluntly, “In light of the threats to our freedom and peace on our continent, the same must now apply to our defense: whatever it takes.” This is the new European opportunity. Countries there are willing to do what is necessary to safeguard peace. And the knock-on effects of these investments in itself make Europe worth a second look.

Source: Rheinmetall investor presentation, as of 3/12/25. CDU is the Christian Democratic Union, CSU is the Christian Social Union, SPD is the Social Democratic Party, GDP is gross domestic product. The “debt brake” is a fiscal rule in Germany’s constitution designed to enforce budgetary discipline.

There is a joke that Europe is a museum. That may have been the case in the past. But it is dramatically shifting from a staid and relatively dull investment landscape to one of the more compelling. Yes, the various economies have been struggling in recent years. Yes, the returns versus various U.S. indexes have lagged, as seen in figure 1. But there are shifts happening that deserve a second look.

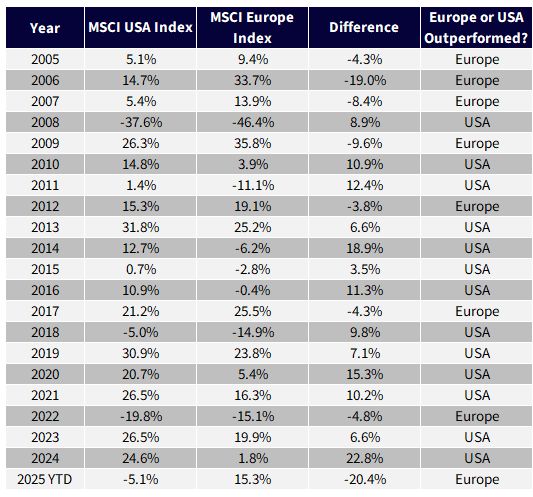

It’s amazing to see 20% outperformance for the MSCI Europe Index over the MSCI USA Index in the first four months of 2025. In figure 1, to get close to this on a full-year basis, one must look all the way back to 2006.

Source: MSCI. 2025 YTD refers to 12/31/24–4/30/25. Past performance is not indicative of future results.

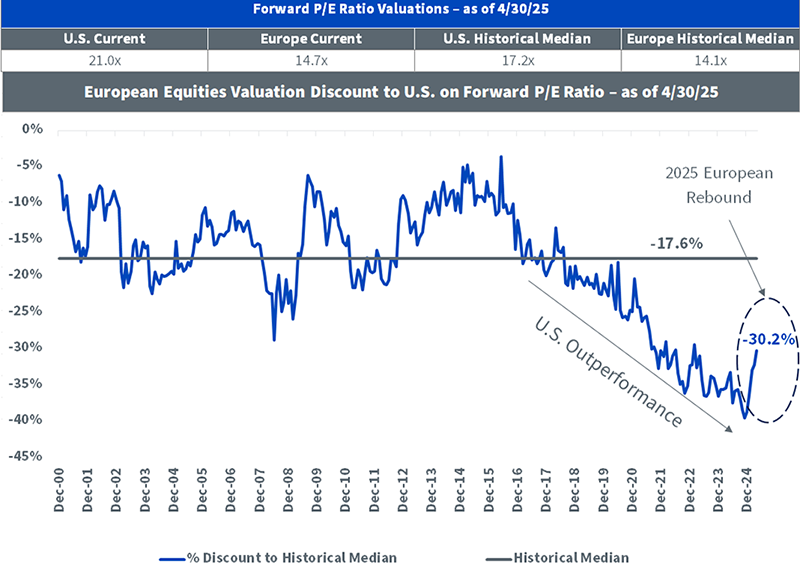

European equities now trade at a 30% valuation discount to U.S. equities, which is well below the long-run average of 18%.3 This isn’t just about being cheap. The decomposed 10-year return attribution shows a stark reality: while U.S. equities soared on the back of multiple expansion, Europe endured the opposite—valuation compression—even as it continued to pay out more of its earnings to shareholders. Picture it: European firms showed up quarter after quarter, delivering dividends and executing buybacks, but their price-to-earnings ratios fell as sentiment and global capital favored flashier growth stories elsewhere. The earnings were there. The cash distributions were real. But the market withheld recognition. That dynamic may now be reversing. With a shift in macro momentum, this mispricing becomes the foundation for a compelling, forward-looking allocation case.

Today’s macro turn, aided by fiscal tailwinds and shifting sentiment, sets the stage for reversal.

Sources: WisdomTree, FactSet. Past Performance is not indicative of future returns.

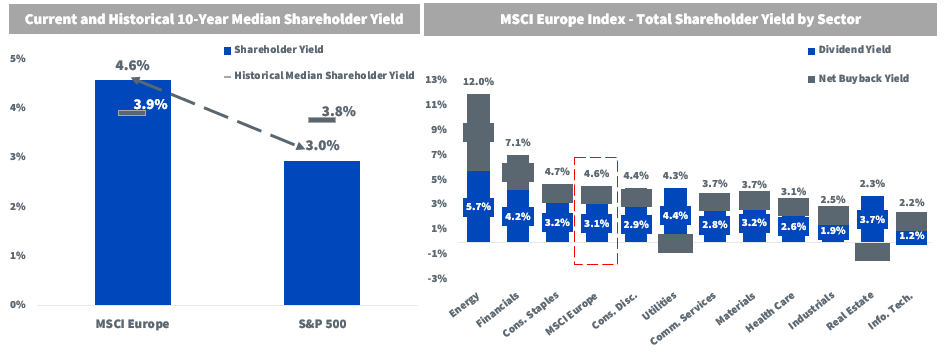

While U.S. markets popularized the concept of buybacks, the European story has quietly evolved. European firms have steadily increased their repurchases, supplementing their already strong dividend culture. As of April 2025, the MSCI Europe Index sported a 1.6% advantage in shareholder yield over the S&P 500 Index.4 It’s a signal of underappreciated corporate discipline and a potential inflection point in capital return dynamics.

Sources: WisdomTree, FactSet, MSCI, S&P, as of 4/30/25. Shareholder Yield = Dividend Yield + Net Buyback Yield. You cannot invest directly in an index.

In an investing world that’s often preoccupied with growth-at-any-price or short-term volatility spikes, shareholder yield is a reminder that the long game still counts. It combines dividends and net buybacks—two of the most tangible ways a company can reward its shareholders. In a capital allocation landscape shaped by capital discipline and margin pressure, the ability to return capital consistently signals confidence and operational strength.

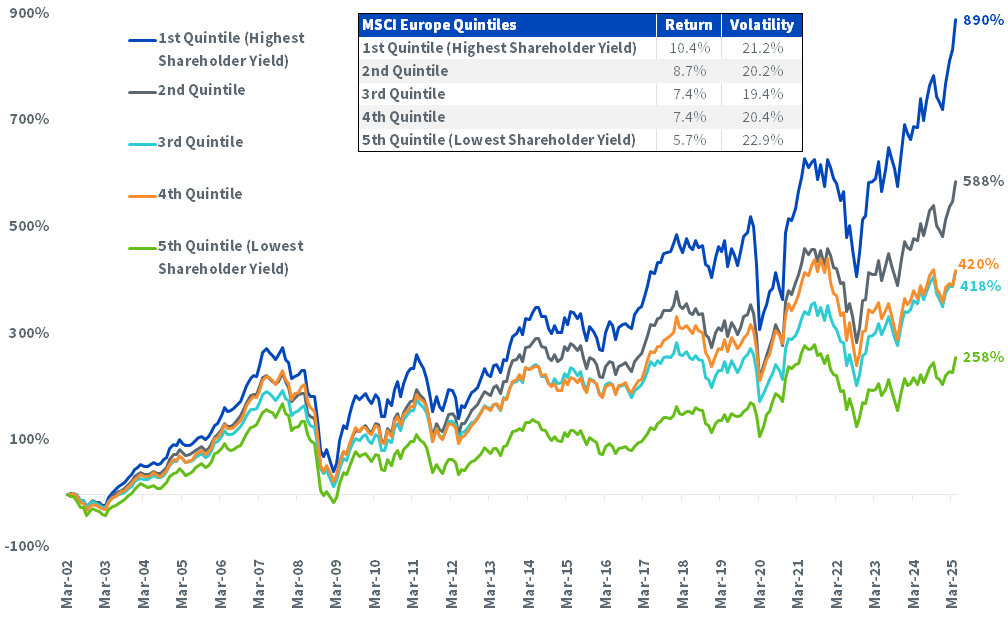

Over the past two decades, companies in Europe with high shareholder yields have consistently outperformed those with low yields—by more than 450 basis points annualized.5 This isn't a niche anomaly. It’s a persistent, sector-neutral factor that rewards firms with disciplined capital return behavior and penalizes diluters and value traps. By integrating buyback data into the yield equation, we modernize what used to be an overly dividend-centric lens.

Sources: WisdomTree, FactSet, MSCI. Past performance is not indicative of future returns.

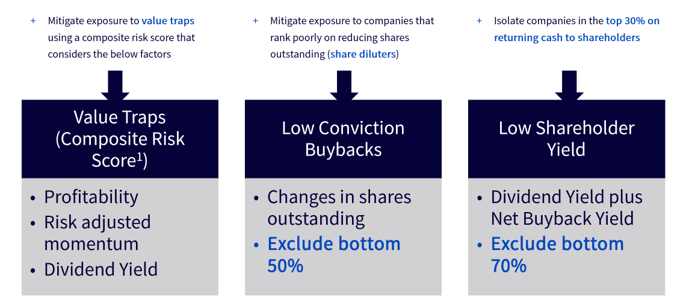

Before we ever get to the highest yielding companies, we start with a crucial three-layer filter. First, we remove value traps using a composite risk score grounded in quality and momentum. Second, we exclude companies with low conviction in repurchase behavior—those that don't consistently reduce share count. Third, we focus only on the top 30% in total shareholder yield, combining dividends and buybacks. The illustration below breaks down this methodology.

Source: WisdomTree.

The WisdomTree European Opportunities Fund (OPPE) reflects a synthesis of two powerful forces: the discipline of shareholder yield and the dynamism of thematic allocation. Roughly two-thirds of the portfolio is dedicated to high shareholder yield; the rest targets companies aligned with long-term themes like defense realignment, digital infrastructure and reshoring. It’s a fundamentally weighted, dynamically hedged approach engineered to make the most of Europe’s moment.

Europe has long been the value sleeve in a global portfolio. Rightfully so. There were cutting-edge, fast-growing technology firms for investors to seek out. But today, shareholder yield and defense-centered stimulus reframe the narrative—a powerful combination of discipline, reflecting capital stewardship, and fiscal tailwinds to rejuvenate growth. These policy shifts result in a more resilient, more rewarding picture for European equities. The last decade was not lost. But it was certainly squandered. Now it isn’t just diversification. It’s directional conviction with a long runway.

1E. Herbert & I. Smith, “German Stocks Hit Record High as Trade Optimism Buoys Markets,” Financial Times, 5/9/25.

2Source: K. Mackrael, “EU Targets American Aircraft, Car Parts for Possible Tariffs if Talks Fail,” The Wall Street Journal, 5/8/25.

3Sources: WisdomTree, FactSet. Past performance is not indicative of future returns.

4Sources: WisdomTree, FactSet, MSCI, S&P, as of 4/30/25. Shareholder Yield = Dividend Yield + Net Buyback Yield. You cannot invest directly in an index.

5Sources: WisdomTree, FactSet, MSCI. Past performance is not indicative of future returns.

Prior to June 02, 2025, the Fund was known as the WisdomTree Europe Hedged SmallCap Equity Fund (EUSC). On that date the fund’s investment policy changed.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in Europe, thereby the impact of events and developments associated with the region can adversely affect performance. The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. The securities of small-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than larger-capitalization stocks or the stock market as a whole. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. Derivatives used by the Fund may not perform as intended. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.