QHY

U.S. High Yield Corporate Bond Fund

Published April 11, 2025

Director, Fixed Income

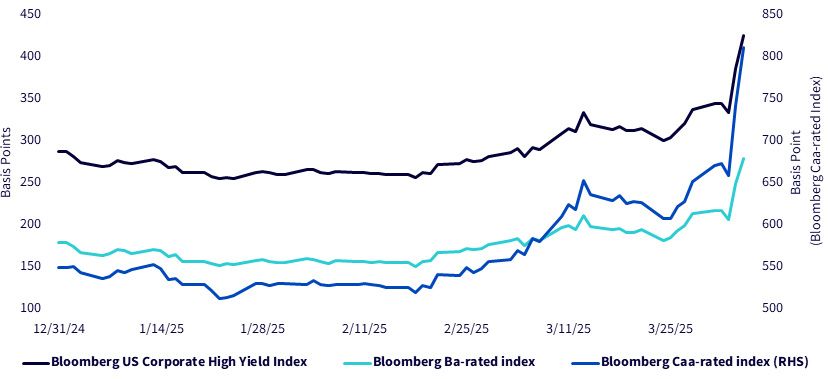

Following last week's sharp sell-off in risk assets, investors have sought refuge in safer assets such as U.S. Treasury bonds. As a naturally more volatile segment of the fixed income market, high-yield (HY) bond spreads have widened by 92 basis points relative to Treasuries since April 2, 2025, "Liberation" Day." However, the sell-off hasn't been uniform across the HY spectrum. BB-rated bonds—considered the higher-quality tier within the HY space—saw spreads widen by 73 basis points, while the more speculative CC-rated bonds experienced a significantly steeper widening of 153 basis points.

Source: Bloomberg, as of 4/7/25. The Bloomberg Caa-rated Index is plotted on a separate (right-hand side (RHS)) y-axis to reflect its wider spread range. For definitions of terms/indices in the chart above, please visit the glossary. You cannot invest directly in an index. Past performance is not indicative of future results.

For many investors, fixed income plays a supporting role in their portfolios—not as a primary driver of returns, but as a source of diversification and stability during periods of market stress. That's why maintaining a quality bias within a fixed income allocation is so important. In this piece, we'll take a closer look at the WisdomTree U.S. High Yield Corporate Bond Fund (QHY) and explore how its focus on higher-quality bonds, relative to both its peers and the broader Index, has contributed to its performance.

Higher Quality When It Matters

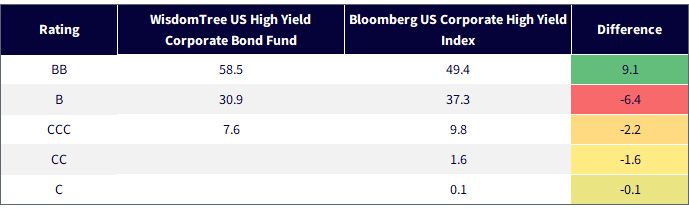

QHY has historically maintained a higher allocation to higher-quality bonds—and that's by design. Our investment approach, grounded in both fundamental and quantitative analysis, is intentionally structured to avoid lower-quality, potentially riskier issuers. As of the end of Q1, QHY held an over-weight position of approximately 9% in BB-rated bonds while remaining under-weight in lower-rated segments such as B and below.

Sources: WisdomTree, Bloomberg, as of 3/29/25.

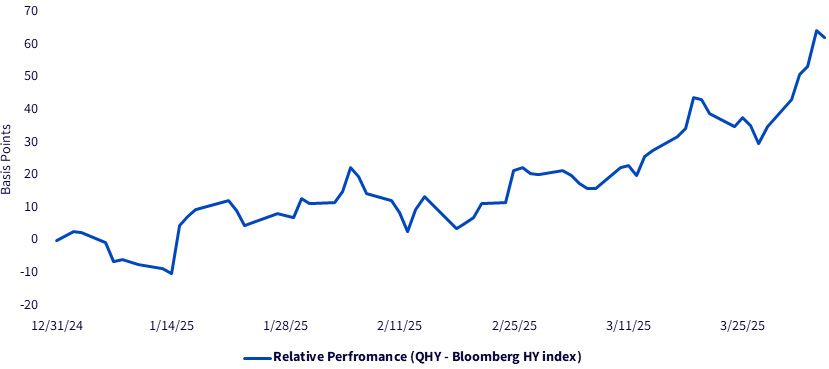

This emphasis on higher-quality bonds has been reflected in QHY's performance. Year-to-date, and since April 2, 2025, the Fund has outperformed the Bloomberg US Corporate High Yield Index by 62 and 10 basis points, respectively.

Figure 3: Relative Performance

Sources: WisdomTree, Bloomberg, as of 4/4/25. Relative performance: Comparing the performance outcome measures of one agency to the performance outcome measures of the other agencies performing the same service. You cannot directly invest in an index. Past performance is not indicative of future results.

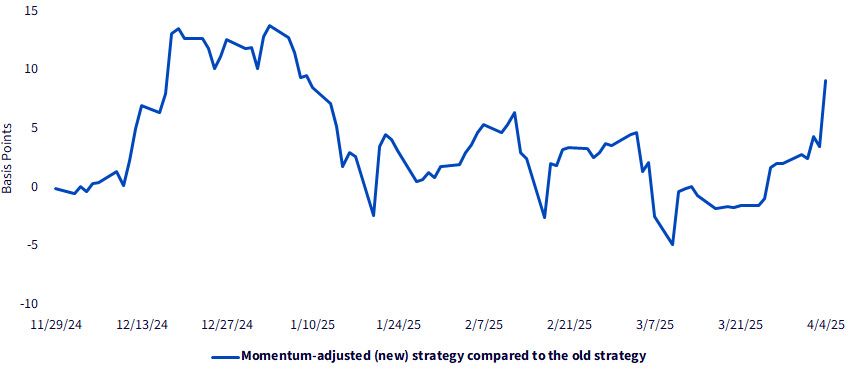

In our most recent rebalance (November 2024), we introduced equity return momentum as an additional factor to complement and enhance the long-term free cash flow signals in our model. This momentum metric evaluates a bond issuer's equity performance against other public issuers in the U.S. high-yield corporate debt universe. These momentum scores are then combined with the issuer's fundamental metrics to refine the bond selection process. The primary goal of this enhancement was to gain a timelier view of an issuer's financial health—and to further elevate the Fund's overall quality by identifying and excluding potential problem issuers before their fundamentals begin to weaken. A rough estimate suggests this change has contributed more than nine basis points in additional performance versus the previous methodology, underscoring the quality boost provided by incorporating momentum.

Source: WisdomTree, as of 4/4/25.

In times of market stress, weaker issuers tend to get hit the hardest. That's where a steady focus on quality can make a real difference. QHY has shown how a thoughtful mix of fundamental research and timely quantitative insights—like the recent addition of equity momentum—can help it steer clear of the riskiest issuers. By tilting toward higher-quality bonds, QHY has delivered a better performance through recent volatility. For investors looking to stay invested in high yield without taking on unnecessary risk, a quality-focused approach like QHY may offer a more resilient way forward.

There are risks associated with investing, including the possible loss of principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

You cannot invest directly in an index.

U.S. High Yield Corporate Bond Fund

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.