EPI

India Earnings Fund

Published March 14, 2025

Director, Quantitative Research

Global Chief Investment Officer

Over the past year, India has experienced a slowdown in corporate earnings growth and stock market performance, reflecting global economic headwinds, reduced government spending and softer demand across key sectors. The MSCI India Index had a muted performance over the past year, dropping 5%1 (most of which came from the depreciation of the Indian rupee versus the U.S. dollar) and declining more than 21%1 from its peak in September 2024. Corporate earnings have also grown at a more moderate pace compared to previous years. However, despite these near-term challenges, India remains one of the most compelling long-term investment opportunities globally, driven by structural reforms, strong demographics and continued economic expansion.

Despite recent earnings pressures, analysts remain optimistic about India's corporate earnings growth over the next few years:

While India has experienced a slowdown in corporate earnings and stock market performance over the past year, its long-term investment story remains intact. The country's strong economic fundamentals, resilient FDI inflows, growing consumer base and government-backed reforms make it a compelling destination for long-term investors.

As earnings growth recovers in the second half of 2025, India is poised to continue its rise as a global economic powerhouse, we believe offering one of the best investment opportunities among emerging markets. Short-term market volatility could be an opportunity for investors to enter India's powerful long-term trajectory.

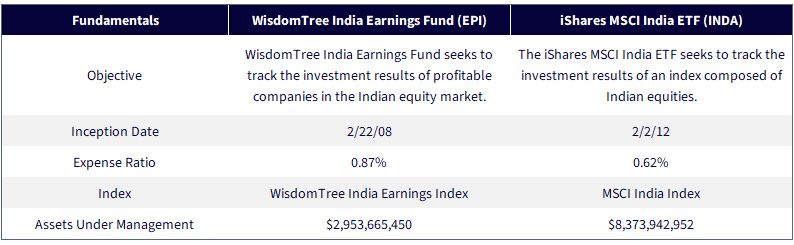

WisdomTree offers differentiated exposure to India through the WisdomTree India Earnings Fund (EPI) and WisdomTree India Hedged Equity Fund (INDH). EPI provides a broad-based, earnings-weighted exposure to tackle the comparatively expensive Indian markets, while INDH provides exposure to large-cap Indian stocks while hedging the currency exposure, thereby delivering lower volatility alongside reduced currency risk.

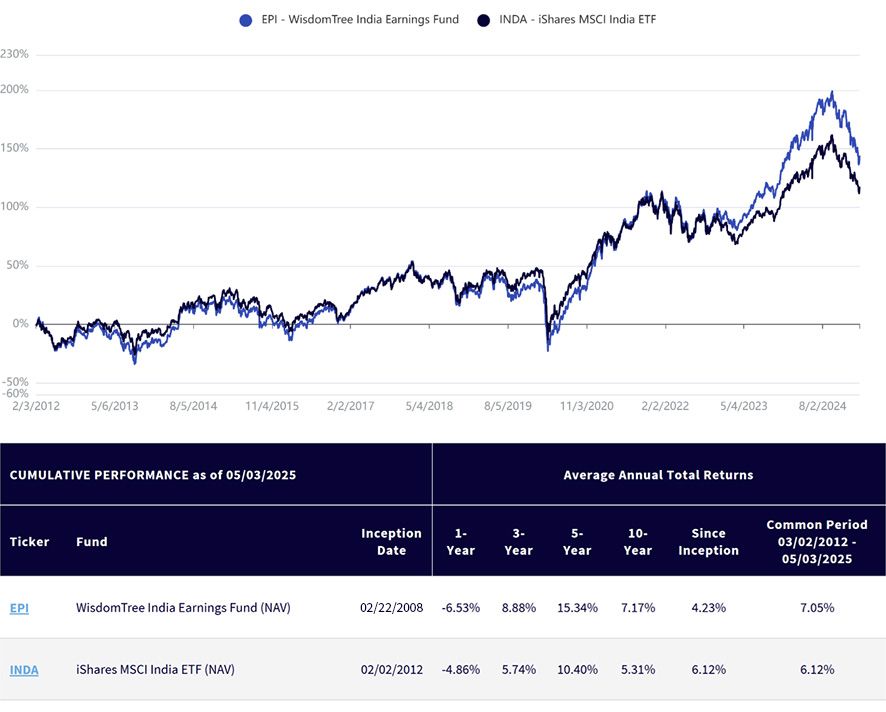

It is notable that EPI has delivered strong outperformance over the common history of the Fund versus the iShares MSCI India ETF (INDA), which continues to be the largest ETF by AUM providing exposure to Indian markets. In the last five years to March 5, 2025, EPI delivered a strong 4.96% of annualized outperformance versus INDA, as seen in figure 1.

Sources: WisdomTree, FactSet. Performance from 2/3/12 to 3/5/25—Cumulative Total Return. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment may be worth more or less than their original cost. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click EPI, or call 866.909.9473 for INDA.

Sources: WisdomTree, iShares, as of 3/10/25. Current performance may be lower or higher than quoted. Investment returns and principal value of an investment may be worth more or less than their original cost. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click EPI, or call 866.909.9473 for INDA.

1 Source: Bloomberg, up to 2/28/25.

EPI: There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region, which can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. As this Fund has a high concentration in some sectors, the Fund can be adversely affected by changes in those sectors. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

INDA: Carefully consider the Fund’s investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’s prospectus and, if available, summary prospectus, which may be obtained by calling 1-800-iShares (1-800-474-2737) or by visiting www.iShares.com or www.blackrock.com. Read the prospectus carefully before investing.

Investing involves risk, including the possible loss of principal.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic, or other developments. These risks are often heightened for investments in emerging/developing markets or in concentrations of single countries.

Diversification may not protect against market risk or loss of principal. Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Any applicable brokerage commissions will reduce returns.

Director, Quantitative Research

Ayush Babel is the Director of Quantitative Research in WisdomTree's multi-asset quantitative research and index teams. In this role, he focuses on developing innovative quantitative strategies across various asset classes while supporting WisdomTree's diverse range of products. His expertise spans factor exploration, portfolio construction and optimization, quantitative investment research, and product development.

With over a decade of experience in the financial services industry, Ayush has held investment research roles at J.P. Morgan and Franklin Templeton. At these institutions, he was responsible for developing and managing equity and fixed income smart beta products, as well as cross-asset risk premia solutions for global institutional and retail clients. His experience covers a broad spectrum of asset classes and investment styles.

Ayush holds a bachelor's in Engineering Physics and a master’s degree in Nanoscience from the Indian Institute of Technology, Bombay.

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.