HEDJ

Europe Hedged Equity Fund

Published March 7, 2025

Global Head of Research

For years, the U.S. stock market has been the world’s favorite playground for investors, a place where capital flowed freely and returns piled up. But investing isn’t about nostalgia—it’s about where the next great opportunities lie. And in 2025, those opportunities are increasingly cropping up outside the U.S. European equities, particularly German stocks, are making waves, attracting fresh capital and delivering performance that challenges the old “American exceptionalism” narrative.

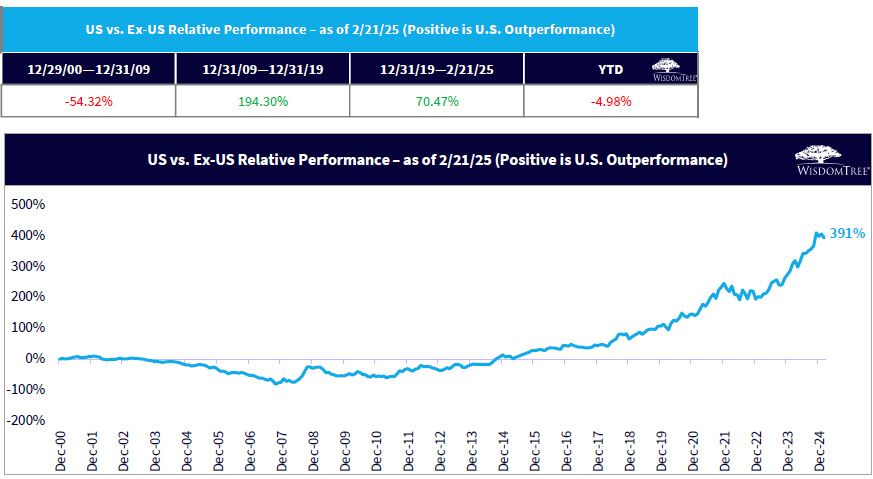

Regarding the difference between U.S. and non-U.S. equities, we can see in figure 1:

Sources: WisdomTree, MSCI, S&P. Data begins 12/29/00 to coincide with the inception of the MSCI AC World ex-US Index, the universe of non-U.S. stocks. U.S. measured by the S&P 500 Index universe. You cannot invest directly in an index. Past performance is not indicative of future returns.

There is a famous expression1:

In the short run, the market is a voting machine but in the long run, it is a weighing machine.

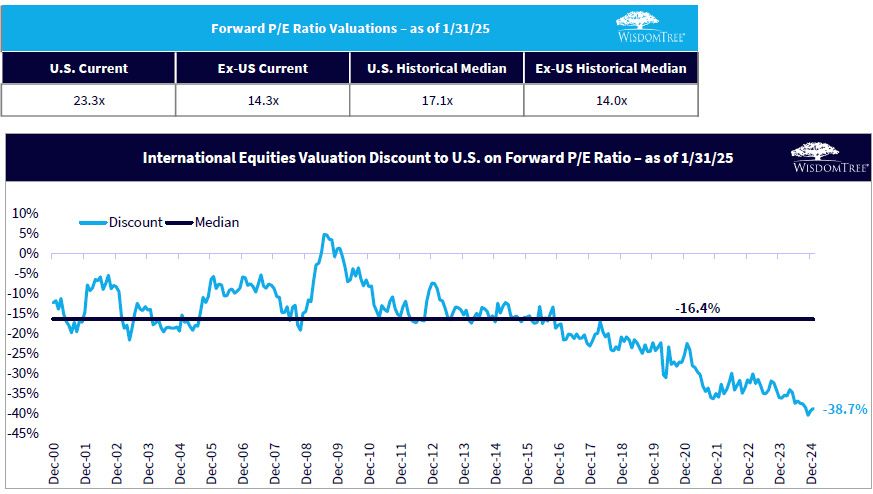

Figure 1 essentially shows us what we already know—the votes have been tallied, and the U.S. equity market has won the performance race in recent years. Figure 2, however, shows the most common detail that is conveyed when people talk about the weighing machine—valuation. Fundamentals matter. The starting valuation of an investment matters:

Sources: WisdomTree, MSCI, S&P. Data begins 12/29/00 to coincide with the inception of the MSCI AC World ex-US Index, the universe of non-U.S. stocks. U.S. measured by the S&P 500 Index universe. You cannot invest directly in an index. Past performance is not indicative of future returns.

A big regional equity market block outside of the U.S. is in Europe, and Europe has been getting a lot of attention in this first quarter of 2025.

European stocks have long been priced at a discount, and while some of that gap has narrowed, the valuation discrepancy is still striking. The MSCI EMU Index of large- and mid-cap European stocks trades at just 14 times forward earnings, compared to 22 times for the S&P 500.2

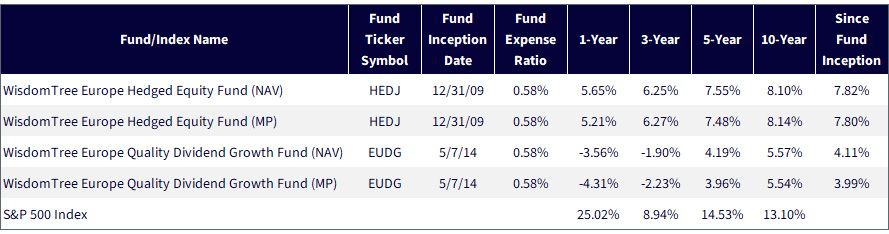

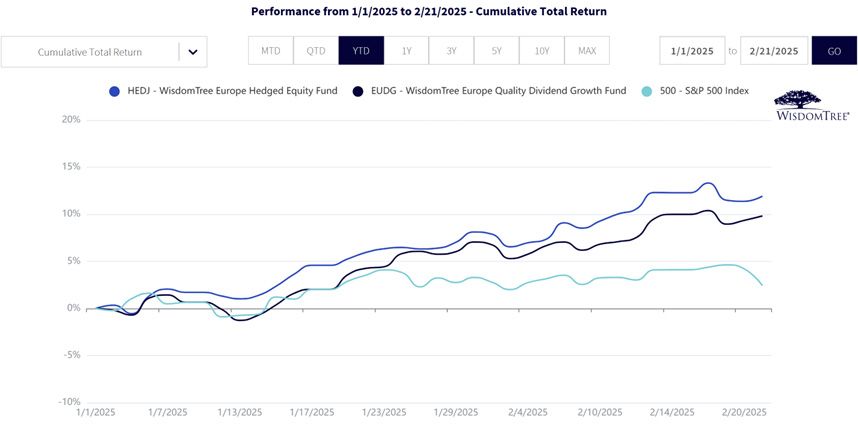

In figure 3b, we can see how some of WisdomTree’s Funds, that focus on European equity exposure, have returned 10% (or more) to start 2025, while the S&P 500 Index benchmark of U.S. equity performance has returned less than 5%. True, it’s a short period, but this is how changes in trends begin.

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/24/25, with returns as of 12/31/24. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance click the relevant ticker: HEDJ, EUDG.

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/24/25, with returns from 1/1/25–2/21/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: HEDJ, EUDG.

Market sentiment is a fickle thing. For years, fund managers shied away from European equities, citing slow growth and structural inefficiencies. But in mid-2024, the tide started turning. Overweight positions in European stocks are at their highest level in years.3

BNP Paribas has emerged as a standout performer, attracting investors with its valuation advantage over U.S. banking giants like JPMorgan Chase.4 The shift isn't just about cheap stocks—it's about investors rediscovering markets that offer solid fundamentals at a reasonable price.

Germany’s DAX Index isn’t just beating the S&P 500—it’s crushing it. In 2025, it has gained six times as much as its American counterpart.5 That kind of outperformance doesn’t happen by accident. Strong corporate earnings, a stable political environment and global demand for German exports are fueling the rally.

Germany’s latest election reshuffled the deck in ways that investors like. The newly elected government is prioritizing infrastructure spending, tax reforms and regulatory easing—pro-growth policies that markets are responding to in real time.6

Monetary policy is also helping. The European Central Bank (ECB) has signaled further rate cuts, giving markets another leg up.7 Defense stocks, in particular, are seeing a surge. Rheinmetall, a leading military equipment manufacturer, is soaring as Europe boosts its defense spending amid rising geopolitical tensions.8

Markets evolve. Narratives change. Investors who cling too tightly to yesterday’s winners risk missing tomorrow’s opportunities.

As U.S. stock valuations flirt with unsustainable levels, international markets—particularly in Europe—offer compelling alternatives. The value rotation isn’t just theoretical; it’s already happening.

Germany, in particular, stands out. With political and economic shifts working in its favor, the DAX is positioned to keep outperforming.12

The U.S. stock market still holds powerful structural advantages, but investors are starting to weigh them against mounting risks. The message is clear: global diversification isn’t just smart—it’s necessary.

1 Benjamin Graham and David L. Dodd, Security Analysis, 6th ed., 2008.

2 Source: Randall W. Forsyth, "European Stocks Are Still on Sale. Where to Shop Now," Barron's, 2/21/25

3 Source: Forsyth, 2/21/25.

4 Source: Forsyth, 2/21/25.

5 Source: Brian Swint, "Why Germany's Election Means Its Stocks Will Keep Beating the S&P 500," Barron's, 2/24/25.

6 Source: Swint, 2/24/25.

7 Source: Swint, 2/24/25.

8 Source: Swint, 2/24/25.

9 Source: Dambisa Moyo, "U.S. Stocks Have Trounced Other Markets. Here Are 3 Risks to American Exceptionalism," Barron's, 2/21/25.

10 Source: Moyo, 2/21/25.

11 Source: Moyo, 2/21/25.

12 Source: Swint, 2/21/25.

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Dividends are not guaranteed and a company currently paying dividends may cease paying dividends at any time. As these Funds can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

HEDJ: Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs.

EUDG: This Fund focuses its investments in Europe, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.