USFR

Floating Rate Treasury Fund

Published February 12, 2025

Head of Investment and Fixed Income Strategy

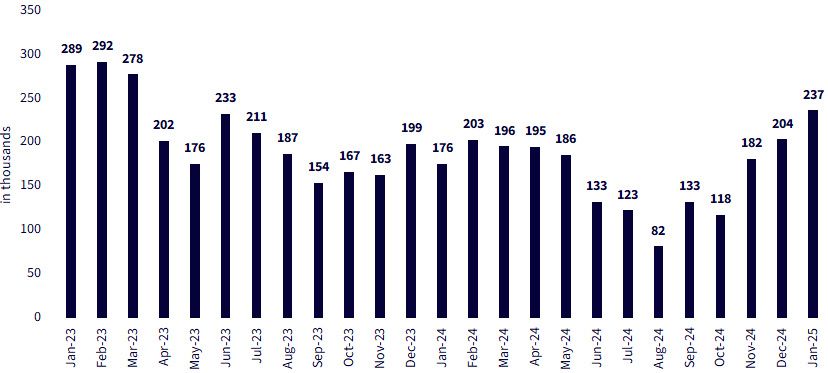

The money and bond markets received their first look at the U.S. employment situation for 2025, and on the surface, the results were somewhat of a mixed bag. Given the importance the Fed has placed on both the inflation and labor market aspects of its dual mandate, it is prudent to “check under the hood” of the data to see if anything stands out. Well, after going through this exercise with the January jobs data, one discovers that the employment data may not have been a mixed bag after all, but rather another indication that the nation’s labor market remains solid, a key factor when trying to ascertain the outlook for any potential rate cuts.

Figure 1 below represents the three-month moving average for U.S. total nonfarm payrolls. Utilizing this means of analysis helps not only to “smooth out” any outsized increases or decreases but, more importantly, can provide guidance for underlying trends.

Source: Bureau of Labor Statistics, as of 2/7/25.

Here are some highlights of what Powell & Co. are looking at now as compared to when they began cutting rates in an aggressive way back in mid-September.

The investment backdrop for fixed income highlights the value of Treasury Floating Rate Notes (FRNs) as the cornerstone of our active/passive barbell approach, where the emphasis is on income without the volatility.

Floating Rate Treasury Fund

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.