Small Caps Surge: High-Quality Opportunities for 2025

Published December 17, 2024

Equity Strategist

Key Takeaways

- U.S. small-cap equities are outperforming large caps by more than 4% in Q4 2024, driven by pro-growth sentiment following Trump’s election victory.

- The recent rebalance of the WisdomTree U.S. SmallCap Quality Dividend Growth Index (WTSDG) boosted exposure to Consumer Discretionary and Financials while trimming lower-quality sectors like Health Care.

- WTSDG’s valuation and quality metrics improved, offering nearly 14% expected earnings growth for 2025 at a forward price-to-earnings (P/E) significantly lower than the S&P 500’s.

Listen to the blog post below:

After a stellar November, the final quarter of 2024 appears decidedly risk-on for U.S. equities. Galvanized by Trump’s presidential election victory and the accompanying pro-growth, deregulatory agenda that markets anticipate, the S&P 500 is routinely notching all-time highs.

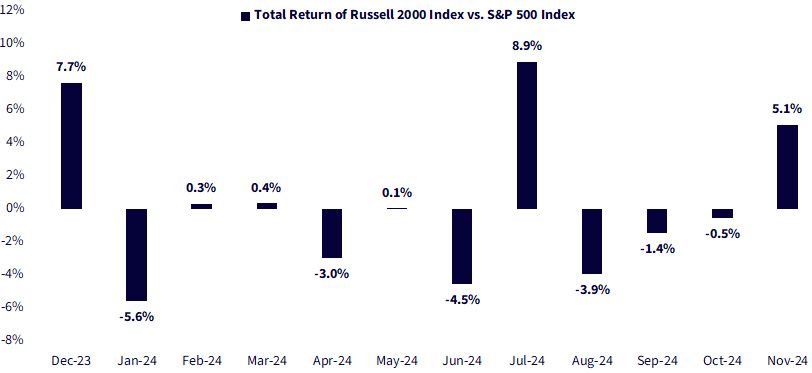

As seen in figure 1, small-cap equities have also quietly benefited, outgaining large caps by more than 5% in November alone. Heading into the final month of the year, they’re outpacing large caps by more than 4.4% since the start of Q4.

Figure 1: November’s Election Fueled an Impressive Rally in U.S. Small Caps

Sources: WisdomTree, FactSet, as of 11/30/24. Past performance is not indicative of future results. You cannot invest directly in an index.

The recent rally reaffirms our bullish outlook for small caps in 2025, and we believe they’ll be bolstered by a trio of catalysts, including:

- A rebound in earnings growth that may outpace the broader market,

- Valuation opportunities as investors grow more discerning of elevated large-cap multiples and

- Potential changes to corporate tax policy that would disproportionately benefit small caps over larger companies.

A potential fourth “shadow catalyst” exists in the rates market. In our view, declining interest rates would also be additive for small caps, provided that decreases are not provoked by material weakening. However, the interest rate environment and its implications for small caps will be challenging to accurately forecast, as markets will have to evaluate the effects of tariff policy and potential inflationary impulses.

In aggregate, we prefer high-quality small caps to implement our bullish views for 2025, on the premise that they’re positioned to benefit from continued equity strength while remaining slightly insulated from adverse economic surprises.

Rebalance Review

We recently completed our annual rebalance for the WisdomTree U.S. SmallCap Quality Dividend Growth Index (WTSDG), which applies our flagship quality methodology to the small-cap universe.

Launched in 2013, it identifies dividend-paying small caps and ranks them on quality factor components like return on equity (ROE), return on assets (ROA) and estimated earnings growth. The final stock basket consists of the top 50% of companies from the ranked universe and can be accessed via the WisdomTree U.S. SmallCap Quality Dividend Growth Fund (DGRS).

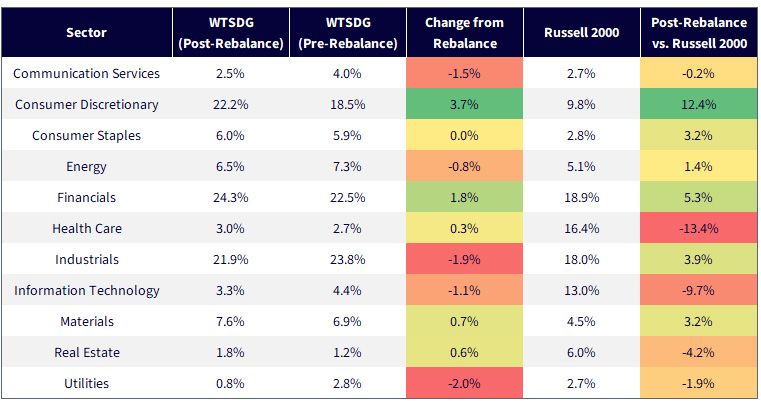

During the rebalance, WTSDG gained exposure to Consumer Discretionary and Financials, the latter sector a strong beneficiary of markets’ post-Trump victory euphoria. These pickups were primarily offset by modest reductions to Communication Services, Industrials and Information Technology, as outlined in figure 2.

Relative to the broader small-cap market, WTSDG is still heavily over-weight in Consumer Discretionary, Consumer Staples and Financials. It’s substantially under-weight in Health Care, which is often comprised of speculative biotechnology companies in the small-cap universe. WTSDG tends to avoid many of these lower-quality names due to its stringent quality framework.

Figure 2: Sectors

Sources: WisdomTree, FactSet, as of 11/30/24. Post-rebalance data for WTSDG as of 12/9/24. You cannot invest directly in an index.

High-Quality Small Caps Remain Cheap and Offer Fundamental Improvements

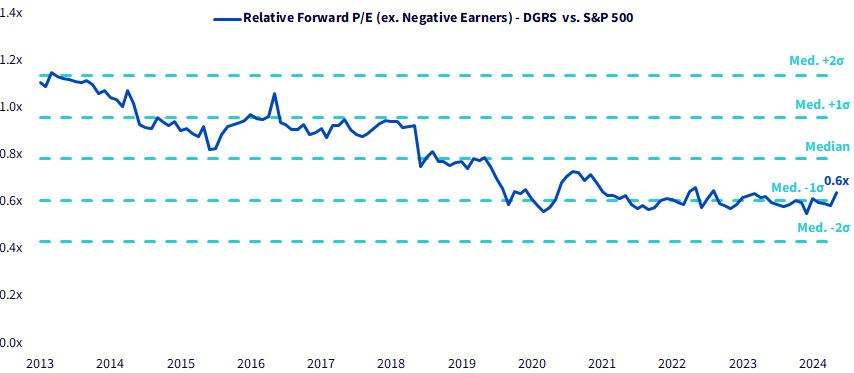

DGRS's prevailing valuations coincide with the opportunity within the broader small-cap universe. Excluding unprofitable companies, its forward price-to-earnings multiple is roughly two-thirds that of the S&P 500, which is a full standard deviation below its median relative multiple since inception, as seen in figure 3.

Figure 3: Small-Cap Value Neglect Presents a Valuation Opportunity against Elevated Large-Cap Multiples

Sources: WisdomTree, FactSet, as of 11/30/24. You cannot invest directly in an index.

We think these multiples are not only more palatable for valuation-sensitive investors but may offer an attractive entry point for robust earnings growth.

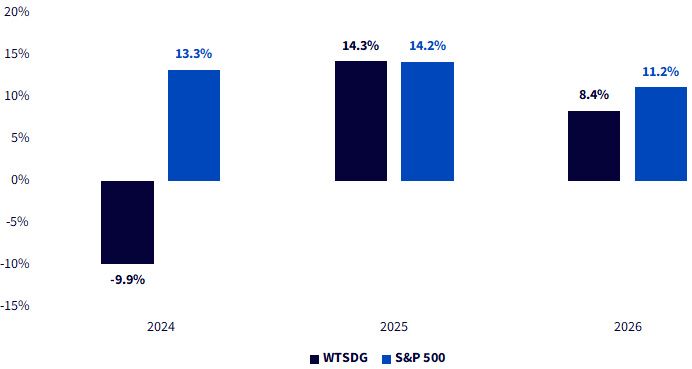

As shown in figure 4 below, as of December 9, the aggregate operating earnings for WTSDG after its rebalance are expected to grow by nearly 14% in 2025, which is in line with the expectation for the S&P 500. But, at a forward P/E multiple that is almost nine points lower than the S&P 500’s, WTSDG provides a more affordable avenue for comparable earnings growth.

Figure 4: Estimated Operating Earnings Growth

Sources: WisdomTree, FactSet, as of 12/9/24. Operating earnings are earnings before interest and taxes (EBIT). You cannot invest directly in an index.

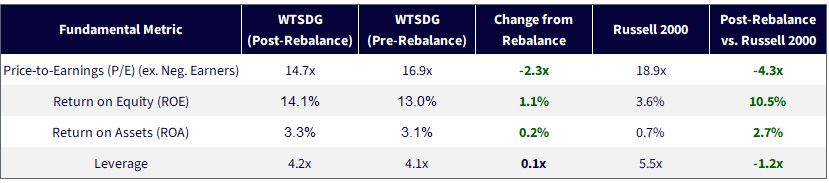

More importantly, the quality profile of WTSDG—the very ethos of the strategy—improved during the rebalance. ROE and ROA, two important measures that demonstrate the ability to generate profits with efficient capital usage, grew by 1.1% and 20 basis points, respectively. Meanwhile, its trailing P/E (excluding unprofitable companies) fell by more than two points, signaling that improved quality can coexist with reduced multiples, especially in the small-cap equity market.

The fundamental comparison versus the Russell 2000 illustrates this well, as the quality profile of the flagship small Index pales in comparison to that of WTSDG, where there’s a double-digit pickup in ROE and nearly 3% more in ROA, coinciding with reduced leverage multiples.

Figure 5: Fundamentals

Sources: WisdomTree, FactSet, as of 11/30/24. Post-rebalance data for WTSDG as of 12/9/24. You cannot invest directly in an index.

Heading into 2025, U.S. small caps are one of WisdomTree’s preferred asset classes, and we think high-quality allocations are a deserving vehicle. They may provide relief from elevated large-cap multiples while also potentially boosting earnings growth and quality measures that may be lacking in the space. Especially after its recent rebalance, WTSDG may continue to be a bedrock small-cap allocation in WisdomTree’s Model Portfolios.

About the contributor

Equity Strategist

Brian Manby is an Equity Strategist at WisdomTree and part of the Investment Strategy team.

He is responsible for developing and communicating equity market insights, investment themes, and portfolio strategies that support the firm’s ETF and investment solutions platform. He evaluates sectors, valuations, fundamentals and equity styles to identify investment opportunities and provide actionable perspectives to clients and advisors. He also helps investors understand how WisdomTree’s equity strategies can be used to achieve long-term investment objectives in evolving market environments.

Brian joined WisdomTree in October 2018 as an Investment Strategy Analyst after a few years as a Consultant for FactSet Research Systems, Inc. He earned a B.A. in Economics and Political Science from the University of Connecticut in 2016 and has been a Chartered Financial Analyst since 2022.