Navigating High-Yield Bonds: Opportunities, Risks and Fallen Angels

Published October 3, 2024

Behnood Noei, CFA

Director, Fixed Income

Andrew Okrongly, CFA

Director, Model Portfolios

Key Takeaways

- High-yield bonds have delivered strong returns in recent years with less volatility than equities, providing an attractive risk/reward balance for investors.

- Despite tighter credit spreads, we maintain a constructive outlook for higher-quality high-yield bonds.

- In our view, these issuers still offer historically attractive yields and are better positioned to navigate refinance risk and any potential economic slowdowns.

- Investors should be cautious of strategies targeting “fallen angels,” as a potential downgrade of Boeing and other issuers may present significant concentration risk.

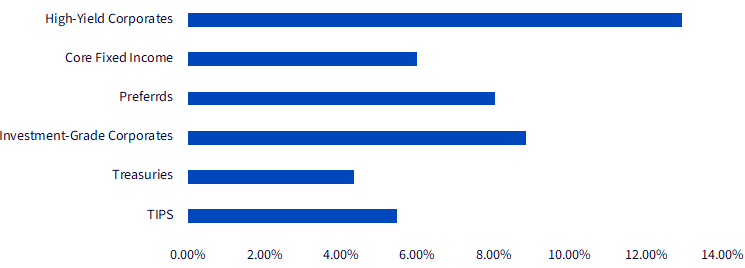

High-Yield Credit Has Delivered Strong Returns, with Less Volatility than Equities

Over the past several years, high-yield bonds have delivered impressive returns, outperforming most other sectors of the fixed income market.

Fixed Income Performance: 9/30/22–9/25/24 (Annualized)

Sources: WisdomTree, FactSet, as of 9/25/24. High-Yield Corporates represented by the Bloomberg U.S. Corporate High Yield Bond Index. Core

Fixed Income represented by the Bloomberg U.S. Aggregate Bond Index. Preferreds represented by the ICE BofA Diversified Core U.S. Preferred

Securities Index. Investment-Grade Corporates represented by the Bloomberg U.S. Corporate Bond Index. Treasuries represented by the

Bloomberg U.S. Treasury Bond Index. TIPS represented by the ICE BofA U.S. Inflation-Linked Treasury Index. You cannot invest directly in an

index. Past performance is not indicative of future returns.

This strong performance can be attributed to several key factors, including healthy investor demand, limited net new supply, robust corporate issuer fundamentals and historically low default rates.

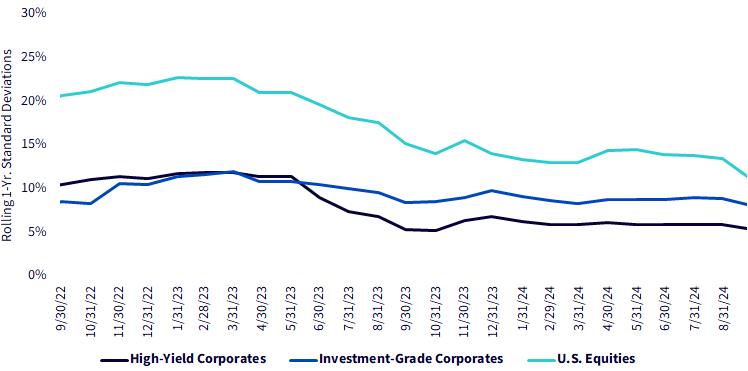

Additionally, despite broader macroeconomic uncertainties, high-yield returns and credit spreads (the excess yield offered over Treasuries) have shown remarkable resilience and relatively low volatility.

Rolling Volatility of High-Yield Credit vs. Investment-Grade, Equities

Sources: WisdomTree, FactSet, as of 9/25/24. Based on one-year rolling standard deviation of monthly returns. High-Yield Corporates

represented by the Bloomberg U.S. Corporate High Yield Index. Investment-Grade Corporates represented by the Bloomberg U.S. Corporate

Bond Index. U.S. Equities represented by the S&P 500 Index. You cannot invest directly in an index. Past performance is not indicative of

future returns.

We Remain Constructive on Higher-Quality High-Yield Credit

While the spreads on high-yield bonds have now compressed to relatively low levels, we maintain a constructive outlook on the higher-quality segment of the high-yield market. Here’s why:

By focusing on higher-quality issuers, investors can benefit from the attractive risk-adjusted returns and income offered in high yield, while also mitigating some of the risks associated with lower-rated debt.

Not All “High-Quality” Strategies Are Created Equal

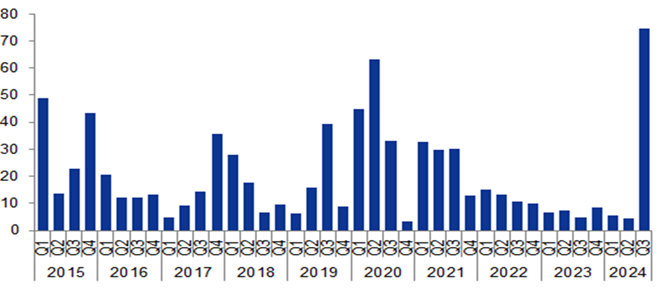

One popular way for investors to access the higher-quality portion of the high-yield universe is through “fallen angel” strategies. These strategies target bonds that were previously rated investment grade but have since been downgraded to high yield.

However, after a period of limited issuer migration, the risk of fallen angels has surged this quarter, particularly due to Boeing’s $57 billion in outstanding bonds, which are under review for possible downgrade by Moody’s.

Notional Value of BBB- Bonds on Downgrade Watch from At Least One of Three Main Rating Agencies

Source: Goldman Sachs Global Investment Research.

While fallen angels may offer enticing yields, the prospects of a Boeing downgrade could dramatically increase the issuer concentration risk in these strategies, some of which have issuer caps as high as 10%!

Given the risks associated with issuer concentration in fallen angel strategies, we suggest that investors consider a broader approach to the high-yield market. Rather than relying solely on credit rating history, we believe it’s prudent to use strategies that systematically identify fundamentally strong issuers across the market.

In summary, the high-yield bond market continues to present a compelling investment opportunity for those seeking strong returns with lower volatility than equities. With careful issuer selection and a focus on quality, investors can still find attractive opportunities in today’s market environment.

Categories

About the contributors

Behnood Noei, CFA

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.

Andrew Okrongly, CFA

Director, Model Portfolios

Andrew Okrongly joined WisdomTree in 2022 as a Director on the Model Portfolios Team. He is responsible for the design and ongoing management of model portfolios and custom solutions for portfolio managers and advisors. Andrew is also a member of the Model Portfolio Investment Committee. Prior to joining WisdomTree, Andrew was a Director on the Outsourced Chief Investment Officer (OCIO) team at Commonfund, where he was responsible for macro-economic analysis and advising institutional clients on strategic and tactical asset allocation. Andrew began his career at BlackRock where he held a variety of fixed income and multi-asset investment roles. Andrew received a BBA degree from the University of Michigan and is a holder of the Chartered Financial Analyst designation.