AGGY

Yield Enhanced U.S. Aggregate Bond Fund

Published October 2, 2024

Head of Investment and Fixed Income Strategy

With the first highly anticipated Federal Reserve rate cut now in the books, I wanted to continue our Money in Motion theme for fixed income investors. As we have witnessed since the September FOMC meeting a couple of weeks ago, the money and bond markets have been consistently “in Motion.” As a result, I wanted to provide an updated hypothetical barbell strategy for this new landscape.

With the Fed “recalibrating” monetary policy toward rate cuts, the uncertainty going forward will now come from the timing and magnitude of this easing. So, how can investors prepare their bond portfolios for this looming uncertainty, which, by the way, will more than likely carry into 2025? The barbell solution underscores the beauty of this strategy due to its adaptability to changing rate environments along the yield curve.

The barbell approach that I’m going to discuss here allows investors the flexibility to add duration while still taking advantage of the income available in the ultra-short/short portion of the inverted yield curve. The adding duration aspect is designed to not only lock in yield outside of shorter-dated maturities, but also offers the ability to take part in a bond market rally if the economy were to falter and rates were to decline even further from current readings. As I have blogged about recently, although one Treasury yield curve (2s/10s) has now “un-inverted,” the other closely watched measure (3-Mo./10-Yr.) remains solidly in negative territory. Against this backdrop, the ultra-short/short portion of the inverted yield curve still offers value from an income perspective.

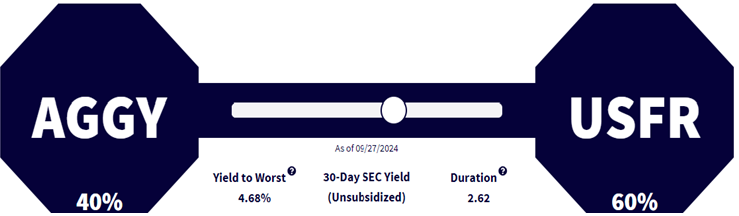

Source: WisdomTree, as of 9/27/24.

Beginning in April and throughout the summer months, I discussed the WisdomTree in-house barbell, which uses our Floating Rate Treasury Fund (USFR) for the ultra-short/short position and our Yield Enhanced U.S. Aggregate Bond Fund (AGGY) for the duration counterweight. This example implemented a 70%/30% USFR/AGGY allocation, and while the premise behind this positioning hasn’t shifted a great deal, it’s always a prudent idea to mark to market.

The updated USFR/AGGY barbell has shifted to more of a 60% USFR/40% AGGY blend.

As you can see, this updated allocation provides a yield-to-worst of 4.68% while bringing duration to just a little above 2½ years (2.62). To sum up, this hypothetical barbell potentially offers a yield advantage of 51 bps versus the benchmark Agg, but with only a little more than one-third of the duration risk, as of this writing.

The investment landscape for fixed income promises to be a fluid one in the months ahead, especially as Fed rate cuts play out. Thus, the barbell allocation shifts presented here are not meant to be static in nature, but more of a dynamic process. By toggling the weights on either end of the barbell, this strategy offers a user-friendly solution for investors to adapt their bond portfolios to potential changes that may be needed.

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

USFR: Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs.

AGGY: Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. Investing in mortgage- and asset-backed securities involves interest rate, credit, valuation, extension and liquidity risks and the risk that payments on the underlying assets are delayed, prepaid, subordinated or defaulted on. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs.

Performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted.

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.