WCBR

Cybersecurity Fund

Published September 12, 2024

Global Head of Research

Check Point Research Reports Highest Increase of Global Cyber Attacks Seen in Last Two Years—A 30% Increase in Q2 2024 Global Cyber Attacks1

Some of the notable events2:

Data breaches and ransomware attacks seem to occur with an alarmingly regular cadence.

On initial view, they don’t. The rate of breaches seems to always be going up, but cybersecurity providers have experienced a lot of share price volatility.

In our opinion, the existence of the attacks emphasizes the market need for protection as well as the market need to continue to evolve and improve that protection. The companies that can ultimately provide this will be in a position to serve a very important market demand.

One way to highlight the strength of cybersecurity businesses is to compare them to a broader set of software stocks.

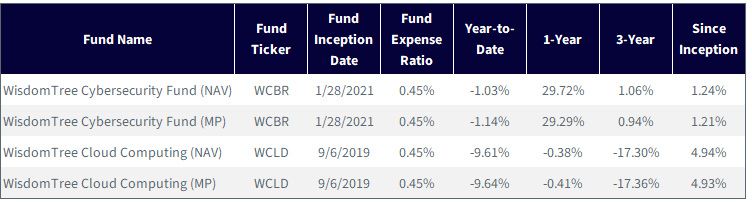

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 6/30/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment

return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or

less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent

month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: WCBR,

WCLD.

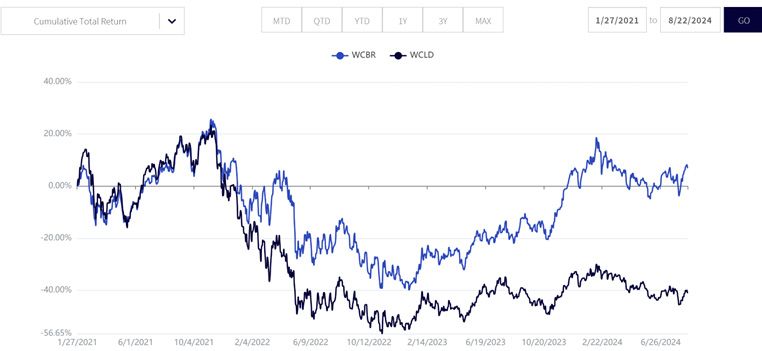

There has been a 48.2% difference in returns between WCBR and WCLD from essentially January 2021 to August 2024. Both WCBR and WCLD:

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 8/23/24. NAV denotes total return

performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment

return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less

than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-

end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: WCBR, WCLD.

Figure 3 breaks down the overall history, which we showed in figure 2, into some different sub-periods. For us, the one-year period, as of August 22, 2024, was particularly notable:

Still, to see that WCBR's return was roughly 30% higher on a one-year basis, as of August 22, 2024, when measured against WCLD—that is a huge difference and one we would not have initially expected.

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, for the period 1/27/21 to 8/22/24). NAV

denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of

future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when

redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the

performance data quoted. For the most recent month-end and standardized performance and to download the respective

Fund prospectuses, click the relevant ticker: WCBR, WCLD.

When we speak to investors, there is clear demand for cybersecurity, but many expect the companies to almost exhibit defensive share price type of behaviors because the need for the services is not really changing week by week or month by month. Yet, the volatility of share prices has been with us and doesn’t show signs of going away.

However, we are able to look at two examples of companies that exhibited massive drawdowns in 2024. First, Palo Alto Networks3:

In figure 4, we show that in about six months, Palo Alto Networks had nearly re-attained its pre-drop levels. We believe this indicates a degree of resilience, but we also recognize that it did not come without serious volatility.

Source: www.macrotrends.net. As of 8/23/24, Palo Alto Networks was a 6.16% weight in WCBR and a 1.59% weight in WCLD. Past

performance is not indicative of future results. Holdings are subject to change.

Another company, CrowdStrike, also experienced a massive drawdown in 2024, and many of us experienced the “blue screen of death” on our Windows-based computers in July 2024 as a result. This was an unfortunate mistake—mistakes do happen—and it highlighted how systems have intricate interdependencies.

Source: www.macrotrends.net. As of 8/23/24, Palo Alto Networks was a 6.16% weight in WCBR and a 1.59% weight in WCLD. Past

performance is not indicative of future results. Holdings are subject to change.

Our takeaway is that we have a megatrend, cybersecurity, that people and companies must remain attentive to. We don’t know exactly which companies or technologies will be the winners, but that is one benefit of working with experts like Team8 and having their knowledge influence the WisdomTree Team8 Cybersecurity Index every six months. So far, cybersecurity has seemed to separate itself, performance-wise, from more general software solutions, and we think that the market demand for these kinds of services could continue over the coming years.

1 Check Point Team, “Check Point Research Reports Highest Increase in Global Cyber Attacks Seen in Last Two Years—A 30% Increase in Q2 2024 Global Cyber Attacks,” blog.checkpoint.com, 7/16/24.

2 Source for bullets: Colin Kellaher, “Halliburton Hit by Cyberattack,” Wall Street Journal, 8/23/24.

3 Source: Palo Alto Networks, Inc., Q2 2024 earnings call transcript, 2/20/24.

For current holdings of, please click the respective ticker: WCBR, WCLD. Holdings are subject to risk and change.

WCBR: There are risks associated with investing, including the possible loss of principal. The Fund invests in cybersecurity companies, which generate a meaningful part of their revenue from security protocols that prevent intrusion and attacks to systems, networks, applications, computers and mobile devices. Cybersecurity companies are particularly vulnerable to rapid changes in technology, rapid obsolescence of products and services, the loss of patent, copyright and trademark protections, government regulation and competition, both domestically and internationally. Cybersecurity company stocks, especially those which are internet related, have experienced extreme price and volume fluctuations in the past that have often been unrelated to their operating performance. These companies may also be smaller and less experienced companies, with limited product or service lines, markets or financial resources and fewer experienced management or marketing personnel. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WCLD: There are risks associated with investing, including the possible loss of principal. The Fund invests in cloud computing companies, which are heavily dependent on the Internet and utilizing a distributed network of servers over the Internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the Internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.