DGRE

Emerging Markets Quality Dividend Growth Fund

Published August 20, 2024

Global Head of Research

The U.S. dollar has been strong, partially driven by the high interest rate policy of the U.S. Federal Reserve (Fed) in recent years to get inflation under control.

With the Fed poised to start lowering rates, some are speculating that the U.S. dollar may go through a period of depreciation. Who stands to benefit from such a regime change?

Emerging market equities.

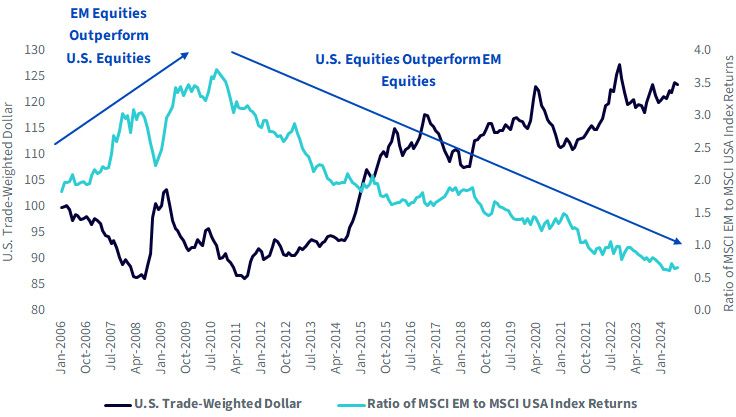

Coming out of the global financial crisis of 2008–2009, few equity markets kept up with the U.S. markets.

In figure 1, we note the ratio of cumulative performance, looking at the MSCI USA Index (U.S. equities) and the MSCI Emerging Markets Index (EM equities) as we also plot a measure of the U.S. dollar against a basket of other currencies.

Sources: MSCI, Board of Governors of the Federal Reserve System (U.S.), Nominal Broad U.S. Dollar Index [DTWEXBGS], retrieved from FRED,

Federal Reserve Bank of St. Louis for the period 1/1/06–7/1/24. You cannot directly invest in an index. Past performance is not indicative

of future results.

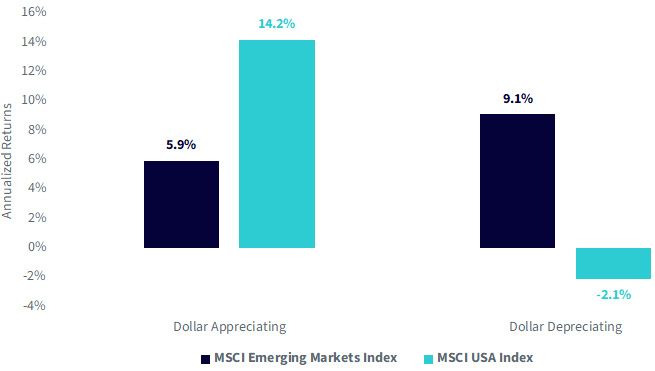

If we dig into the two distinct periods, denoted from basically the end of August 2010 to the present for “Dollar Appreciating” and from the start of the time series to August 2010 for “Dollar Depreciating,” we see figure 2:

Source: MSCI. “Dollar Appreciating” refers to the period 8/31/10–7/31/24. “Dollar Depreciating” refers to the period 12/31/05–

8/31/10. Past performance is not indicative of future results.

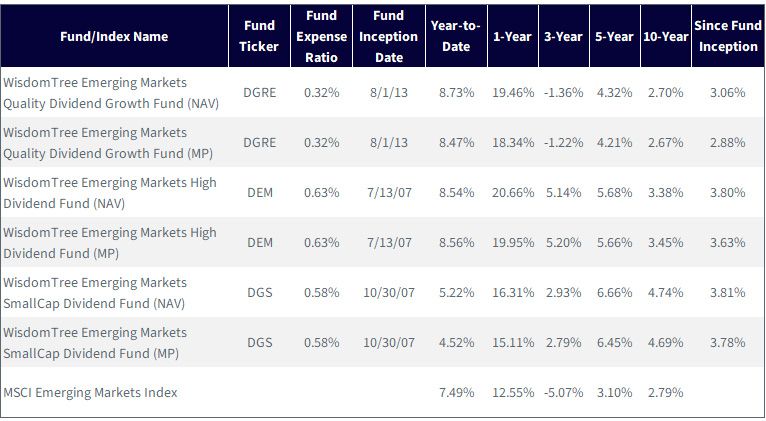

WisdomTree has a range of options for emerging market equities, a number of which have been around for longer than 10 years.

The most widely followed emerging market equity performance benchmark is the MSCI Emerging Markets Index.

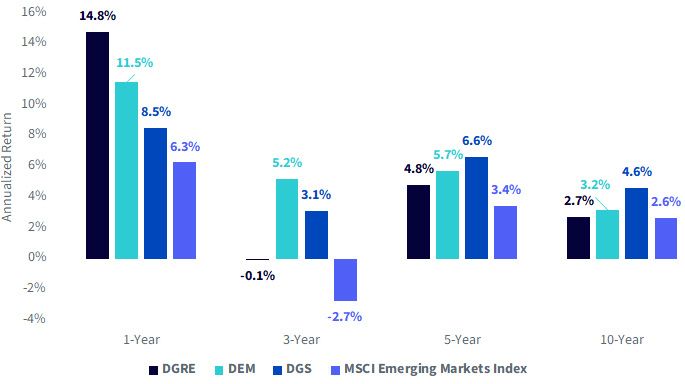

If we look at DGRE, DEM and DGS relative to the MSCI Emerging Markets Index on a performance basis, we see different things over different periods:

Sources: WisdomTree, MSCI. Fund data specifically from the Fund Comparison Tool in the PATH suite of tools, as of 6/30/24. Performance is

historical and does not guarantee future results. Current performance may be lower or higher than quoted. Investment returns and

principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their

original cost. For the most recent month-end performance, click the relevant ticker: DGRE, DEM and DGS. WisdomTree shares are

bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Total returns are calculated using the daily 4:00 p.m.

EST net asset value (NAV). Market price returns reflect the midpoint of the bid/ask spread as of the close of trading on the exchange where Fund

shares are listed. Market price returns do not represent the returns you would receive if you traded shares at other times.

Sources: WisdomTree, MSCI. Fund data specifically from the Fund Comparison Tool in the PATH suite of tools, for the period

7/31/14–7/31/24. Performance is historical and does not guarantee future results. Current performance may be lower or

higher than quoted. Investment returns and principal value of an investment will fluctuate so that an investor’s shares,

when redeemed, may be worth more or less than their original cost. For the most recent month-end performance, click

the relevant ticker: DGRE, DEM and DGS. WisdomTree shares are bought and sold at market price (not NAV) and are not

individually redeemed from the Fund. Total returns are calculated using the daily 4:00 p.m. EST net asset value (NAV). Market price

returns reflect the midpoint of the bid/ask spread as of the close of trading on the exchange where Fund shares are listed. Market

price returns do not represent the returns you would receive if you traded shares at other times.

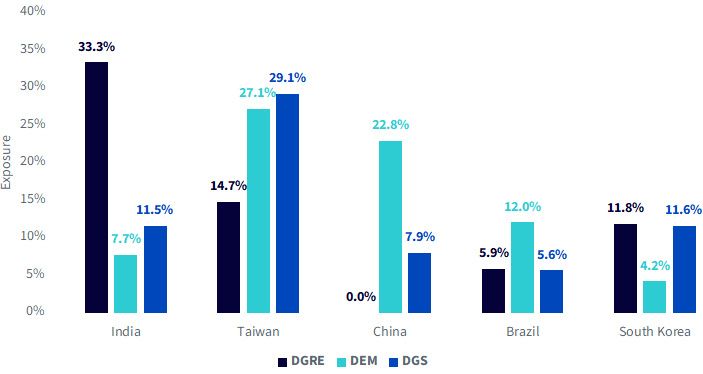

When people talk about real estate, all of us know the mantra—location, location, location. In emerging market equity investments, the same mantra applies.

The world has been very excited about the stability of India, in that the country has elected the same leader through three elections. Even if no government is perfect, sometimes stability and the capability to actually implement policy over a longer time is more important than any one leader being perfect. Business and investment can follow as long as people know what is going on. As we look to figure 4:

Source: WisdomTree, specifically the PATH fund comparison tool, with data as of 6/30/24. Holdings subject to change.

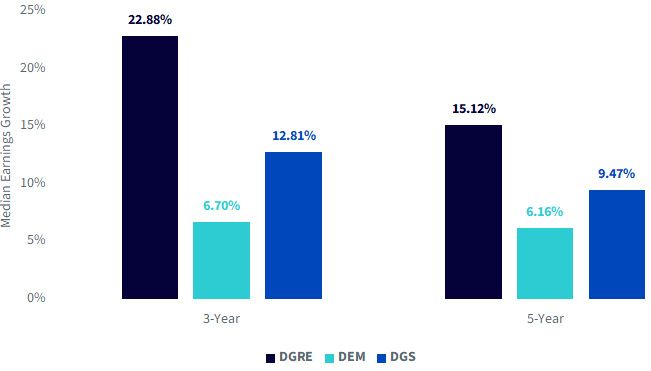

One of the trade-offs that investors often have to make is as follows:

Historically, DEM's strategy of following the highest-yielding dividend payers has been more defensive in consistently finding the lowest valuations but also finding the lowest earnings growth.

DGRE is meant to be a contrasting style of investment, finding companies with stronger earnings growth over time.

DGS is a bit different, being more of a broad-market small-cap strategy exposed to hundreds of underlying stocks. Emerging market companies pay dividends very early in their respective life cycles.

We see a version of this story playing out in figure 5.

Source: WisdomTree, specifically the PATH fund comparison tool, with data as of 6/30/24. Past performance is not

indicative of future results.

What are emerging markets? What are developed markets? The real answer these days is that it depends on who you ask. It is more important than ever to look under the hood and think about which countries might be poised to provide strong, pro-business conditions.

1 Apple, Amazon, Meta Platforms, Alphabet, Tesla, Microsoft and Nvidia.

2 Source: Christopher Woods, “Classifying South Korea as a Developed Market,” FTSE Russell, 1/13. https://research.ftserussell.com/products/downloads/FTSE_South_Korea_Whitepaper_Jan2013.pdf

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing on a single sector and/or smaller companies generally experience greater price volatility. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as adverse governmental regulation, intervention and political developments. Due to the investment strategy of these Funds, they may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.