Navigating Earnings Season: The Death of Price over Volume

Published July 18, 2024

Samuel Rines

Macro Strategist, Model Portfolios

Key Takeaways

- Companies have shifted from prioritizing price increases over maintaining sales volume to focusing on regaining lost volumes through marketing efforts.

- This shift has led to increased marketing spend, benefiting large platforms with significant consumer reach, known as "The Mad Metas."

- Companies are investing in AI capabilities, with future trends potentially including the "Big Data Bid" for better AI inputs and the rise of "Kiosk Kings" to improve margins and address labor shortages.

Welcome to the second installment of our new blog series, “Navigating Earnings Season.” In this series, I dive into the world of earnings reports from major companies, spanning giants like JP Morgan and Pepsi, as well as niche players in various sectors. As the earnings season unfolds, these corporate outlooks offer real-world insights that often contrast sharply with the uncertainty emanating from the Federal Open Market Committee (FOMC).

Not long ago, price over volume—PoV—was rampant. Every earnings season was a sort of race for pricing power and a lack of care for losing volume. And it spanned everything from toilet paper and soft drinks to potato chips and candy. The commentaries on earnings calls were nearly identical, “We raised prices by x, and only lost y in volume.” Critically, price increases were radically outpacing the losses in volumes. Simply, it was good for business. After all, the revenue equation for the cohort is straight-forward: price multiplied by volume = revenue.

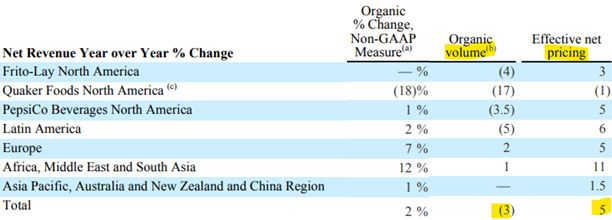

Source: PepsiCo (emphasis added).

That calculus no longer applies. The pricing power of the post-Covid, post-Ukraine era is gone. Volumes matter again.

The evolution of PoV should not be dismissed. While PoV was powerful and felt widely by U.S. consumers, the other side of PoV is not so easily spotted. But the consequences could be as meaningful. Prices are not going to “go back” to where they were in the pre-Covid era. That is important. The “P” in PoV is going to be stable. The revenue equation is now reliant on the “V.” Getting to a positive “V” requires effort in the form of marketing dollars.

Source: Pepsi.

And that makes for some oddities moving forward. There was a brief period when it looked as though winners would be the those that aggressively raised prices themselves. The argument was along the lines of “They raised prices, those prices will hold, volumes will slowly come back, input costs will normalize, margins will expand, and that will flow to the bottom line.” Call it Price and Margin. That is not wrong. But it is not the entire story either.

Source: Pepsi (emphasis added).

As it turns out, the winners from the death of PoV are a much larger swath of companies. The extra dollars from the period of extraordinary pricing power are now required to earn back those lost volumes. Volumes do not magically reappear. It takes “brand investment” which is earnings call speak for “marketing spend.”

The real evolution of PoV was not Price and Margin (PAM). It was Price and Marketing. That leads to an entirely different set of winners—The Mad Metas. The giant platforms with reach and influence around consumers. Those are the beneficiaries of the race to find volumes.

Taking a step back, The Mad Metas did not do well during the PoV era. There was no competition for volumes, and therefore little need to invest in their brand. Raising prices and sacrificing volumes is not something to plaster across social media. But, as PoV began to fade, their time arrived.

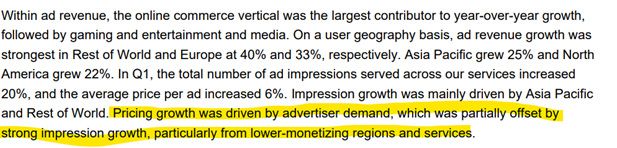

Source: Meta Platforms (emphasis added).

The question that matters is “What comes next?” The Mad Metas are already pouring money into building out their AI capabilities. That is already here. Could it be the “Big Data Bid” as companies search for ever better inputs for their AI programs? Or the “Kiosk Kings” as labor becomes expensive or unavailable and kiosks improve margins while alleviating chokepoints? Who knows. But the evolution of PoV to PAM to The Mad Metas is not something to be ignored.

Categories

About the contributor

Samuel Rines

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.