DFJ

Japan SmallCap Dividend Fund

Published May 28, 2024

Head of Equity Strategy

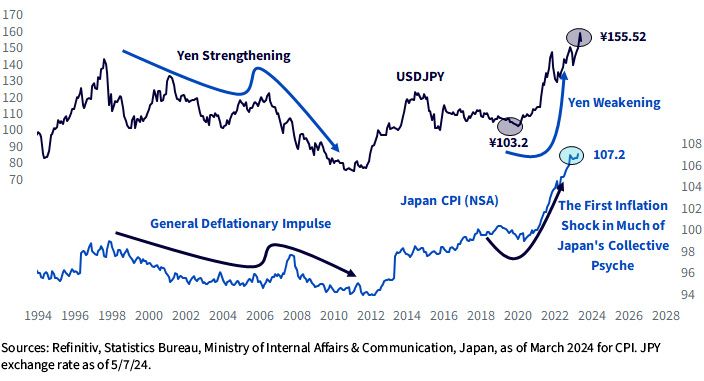

For Japanese of a certain age, the inflation shock of the Covid and post-Covid era is a bit of a wake-up call. After trending either downward or ever-so-slightly upward since the 1990s, suddenly Japan’s CPI bolted higher in just the last few years. The primary cause: a collapse in the yen from ¥103 per dollar in early 2021 to ¥155 (figure 1).

This jolt has been more than psychological.

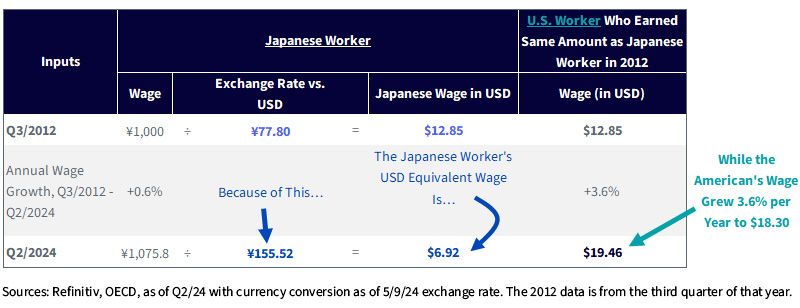

With its currency in the basement, the other side of the inflation coin is Japan’s sudden competitiveness on the wage front. In late 2012, when the yen was so strong that a dollar only fetched ¥77.8, a Japanese worker who earned ¥1,000 could convert that wage to $12.85. Fast forward to the present. In the last dozen or so years, the average Japanese worker’s wage only grew at a 0.6% yearly rate, according to the OECD. But when you convert today’s ¥1,075.8 wage to USD, that is $6.92.

In contrast, an American who earned $12.85 back then has seen annual income growth of 3.6%. Compounded to the present, the American worker is up to $19.46. That is about triple the Japanese worker’s compensation in USD terms (figure 2).

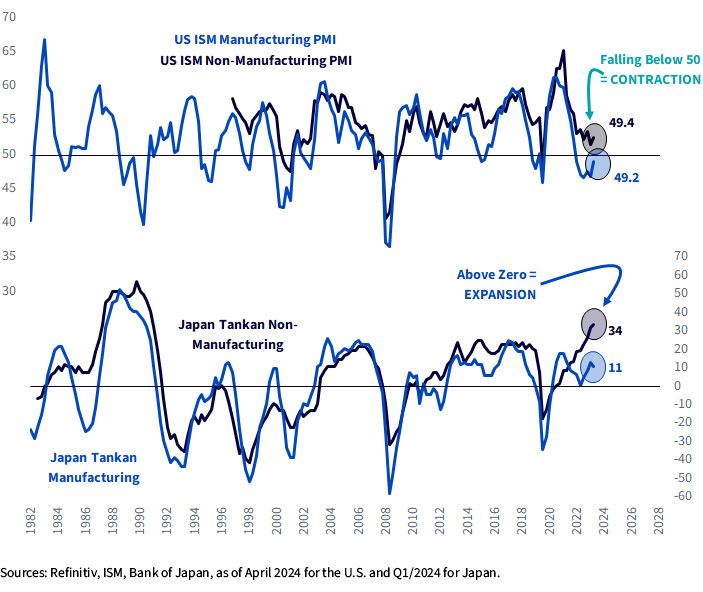

In the U.S., both the manufacturing and services gauges for the ISM PMI have broken below 50, the line of demarcation1 between expansion and contraction (figure 3). Japan’s Tankan survey is in the opposite camp: both gauges are above the zero line on that diffusion index. In the case of services, the 34 it registered in the latest survey is the highest in three decades.

It’s little wonder why this is the case: wages are paid in cheap yen while foreign revenues are collected in stronger currencies such as the dollar.

I’ve written extensively about the country’s expansion of the NISA retirement system, the country’s defined contribution program. The bullish event was the tripling in the annual maximum contribution amount that went into effect for 2024. Depending on the exchange rate at any given time, the contribution limit, in USD terms, leaped from $7,500-$8,000 per year to $22,500-$24,000.

As we imagined would happen, a large amount of NISA contributions have been going into Japanese stocks, seemingly on account of many Japanese coming to realize that 0% yields on bonds are no longer going to cut it amid the country’s sudden flirtation with structural inflation.

The Japan Times reported on May 5:

Nearly 50% of investments made through the new Nippon Individual Savings Account, or NISA, program went to Japanese stocks from January through March, a survey has shown…

"The amount bought via NISA was more than three times the year-before level," Daiwa Securities Managing Executive Director Kotaro Yoshida said, explaining moves by NISA account holders at the company…

Stocks with stable and high dividends were especially popular.

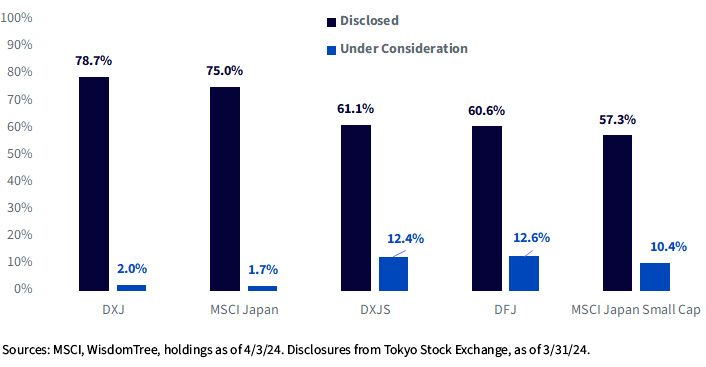

The confidence to purchase Japanese equities has been helped by the Name and Shame List initiative of the Tokyo Stock Exchange (TSE), which is strong-arming companies into a shareholder-friendly corporate governance regime.

Under a push called “Management That IS Conscious of Cost of Capital and Stock Price,” they told all listed companies that they needed to put together proposals for getting their price-to-book ratios and profitability metrics higher. Those who didn’t propose a corporate governance game plan would be shamed by having their name on the notorious list.

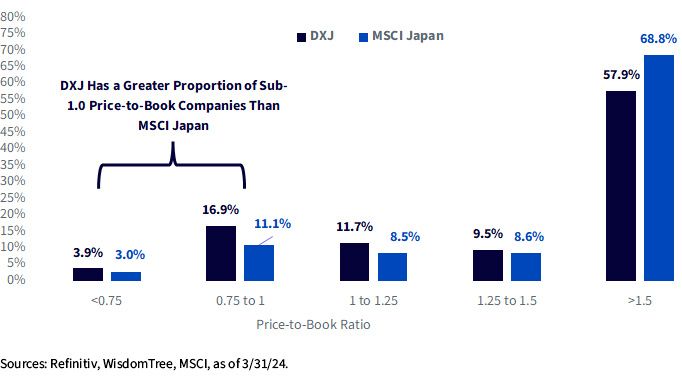

It worked. Most companies have complied (figure 4). We tabulate that 78.7% of the market capitalization of DXJ, the WisdomTree Japan Hedged Equity Fund, created a proposal. In our two small-cap mandates, DFJ and DXJS, 60%-61% of the market cap has developed a profitability strategy that is to the stock exchange’s satisfaction.

For definitions of terms in the chart above, please visit the glossary.

Because the TSE is so focused on sub-1.0 price-to-book ratios, there is something that is promising for DXJ at the moment: nobody wants to be the executive who presides over a lowly equity valuation. In terms of a catalyst for DXJ, about 20% of its exposure is in stocks whose price-to-book ratio is below 1.0, ostensibly because most of them have not (yet) complied with the demands of the TSE. As they do—so the theory goes—then perhaps those firms’ valuations could rerate upward.

We have three long-only Japan Funds. They are:

1 Demarcation = the marking of the limits or boundaries of something

DXJ/DXJS/DFJ: There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. This may result in greater share price volatility. Funds focusing their investments on smaller companies or certain sectors increase their vulnerability to any single economic or regulatory development. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DXJ/DXJS: Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations, and derivative investments, which can be volatile and may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

Head of Equity Strategy

Jeff Weniger, CFA, has been with WisdomTree since 2017 and serves as the Head of Equities. He shapes the firm’s market outlook through a combination of macroeconomic and fundamental analysis. With more than two decades in investment strategy, Jeff is known for his work on market cycles and valuations. Before joining WisdomTree, Jeff was with BMO Private Bank and BMO Global Asset Management for 11 years. At BMO, he sat on the firm’s Asset Allocation Committee and co-managed ETF model portfolios across the U.S. and Canada. In 2013, at age 32, he became the youngest member of BMO’s Global Investment Forum. When he left BMO to come to WisdomTree, his final role was Director, Senior Strategist in the Office of the CIO in 2017.

Jeff is a frequent television guest on networks such as CNBC, Bloomberg, and Schwab, with regular print appearances in The Wall Street Journal, Barron’s and Reuters. He also appears weekly on the Behind the Markets podcast and is a regular on SiriusXM’s The Business Briefing. On X, Jeff has developed one of the larger followings in financial media. He earned a B.S. in Finance from the University of Florida and an MBA from the University of Notre Dame. He has held the CFA charter since 2006.