USFR

Floating Rate Treasury Fund

Published October 1, 2025

Head of Investment and Fixed Income Strategy

With the Federal Reserve (Fed) resuming its rate cut cycle, investors have been asking what fixed income strategies they should be considering in this "new" investment setting. In my opinion, there remains one approach that continues to stand out: Treasury floating rate notes (UST FRNs).

With the Fed already cutting the Fed Funds Rate at its September Federal Open Market Committee (FOMC) meeting and likely embarking on one or two more of these easing moves in the month(s) ahead, investing in FRNs may be viewed with some skepticism. Indeed, typically FRNs are associated with rising rates, not falling rates. However, as investors have been witnessing post-September FOMC, Treasury note and bond yields do not necessarily completely follow suit. In fact, they can still rise.

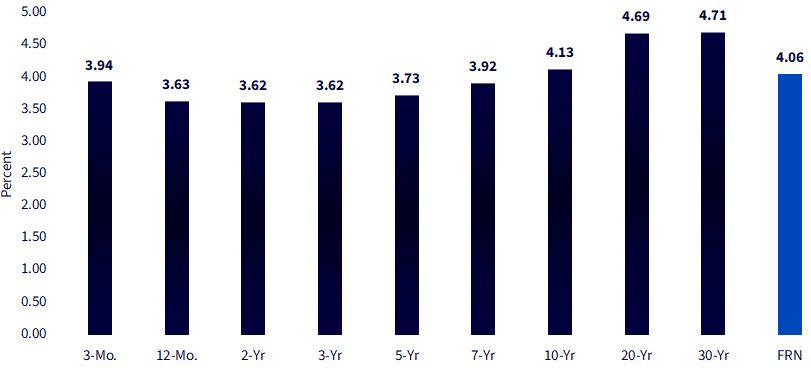

Source: Bloomberg, as of 9/29/25.

This is exactly what has transpired in the two-week period following the most recent Fed rate cut. As of this writing, the UST 2-, 5- and 10-Year yields, as an example, have seen their respective levels increase by about 20 basis points (bps) from when the actual rate cut was announced on the afternoon of September 17.

Why is this important, you may ask? Let's go back to Bonds 101: yield increases = lower prices. In other words, if you had bought one of these UST securities in the wake of the Fed's rate cut, you have now lost money. It is important to remember that these are "fixed" coupons as compared to a UST FRN, which is a floating rate.

With respect to UST FRNS, the "floating" mechanism is tied to the weekly 3-month t-bill auction, plus a spread. While the 3-mo. t-bill yield will fall along with the Fed Funds Rate, the spread over the t-bill provides a nice cushion and yield advantage.

The chart above highlights how the yield curve for UST FRNs versus most other Treasury securities is either flat or inverted. In fact, the 20- and 30-year bonds are the only two maturities with yields visibly above FRNs. In the meantime, the FRN yield is anywhere from about +15 bps to +45 bps above the two-to-seven-year sector.

How about the path ahead? At the most recent 3-mo. t-bill auction, the yield came in at 3.86%. That means the yield is already pricing in another 25-bp cut from the Fed because the "new" Fed Funds trading range would then be 3.75%–4%, with 3.86% about right in the middle of that band. Thus, the FRN yield of 4.06% represents a 20-bp positive spread to the t-bill yield, and arguably also allows for another quarter-point cut from Powell & Co.

For investors looking to take advantage of the UST FRN strategy, consider the WisdomTree Floating Rate Treasury Fund (USFR).

There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Floating Rate Treasury Fund

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.