XSOE

Emerging Markets ex-State-Owned Enterprises Fund

Published January 9, 2026

Global Head of Research

For most U.S. investors, the concept of state ownership feels foreign, almost anachronistic. America's economic mythology rests on the idea that markets allocate capital more efficiently than governments ever could. The implicit hierarchy is clear: privately owned equals dynamic and efficient; state-owned equals bureaucratic and stagnant. But step outside the U.S., and this binary quickly blurs. Across much of the world, especially in emerging markets, the state is not merely a regulator of markets, but a participant, shareholder and sometimes the commanding force behind entire sectors.

In economies like China's, the state remains deeply embedded in the corporate landscape. State-owned enterprises (SOEs)1 dominate sectors such as energy, banking, telecommunications and infrastructure. These companies are not just profit-seeking entities; they are instruments of national policy, used to stabilize employment, secure resources and project geopolitical influence. By contrast, non-state-owned enterprises (NSOEs), often more entrepreneurial and export-oriented, compete for capital and innovation on market terms. Understanding the balance between these two corporate archetypes is increasingly vital, especially as global investors reassess where true economic dynamism resides.

The distinction between state and non-state capitalism has become a quiet but powerful driver of returns in emerging markets. Over the past decade, NSOEs have tended to deliver stronger growth, higher profitability and better capital discipline, traits that resonate with Western investors. Yet SOEs, backed by policy support and protected market share, can dominate in periods of macro volatility or strategic realignment. As the global economy fractures into regional blocs and the state reasserts itself even in advanced economies, from industrial policy to energy transition, the old boundary between public and private capital may be less absolute than it once seemed.

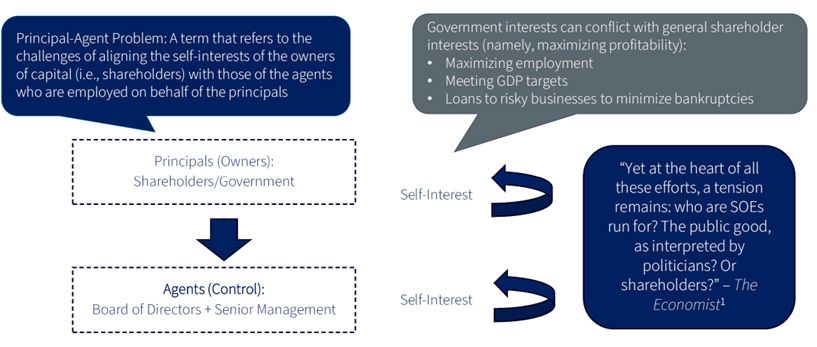

Figure 1 captures the essence of the principal–agent problem as it applies to state-owned enterprises (SOEs). In theory, the government, as the principal, owns the enterprise on behalf of its citizens, delegating control to professional managers and boards who act as agents. In practice, however, the agents' incentives often diverge from pure profit maximization. Governments may direct firms to prioritize macroeconomic or social goals, such as sustaining employment, supporting gross domestic product (GDP) targets or preventing bankruptcies, even when these conflict with shareholder value. This introduces a structural tension at the heart of SOEs: are they run for the public good, as defined by policy makers, or for shareholders, who expect returns on capital? The Economist's framing distills the paradox perfectly: state ownership transforms a simple agency problem into a multi-layered struggle between politics, economics and accountability.2

"Source: "Government-Controlled Firms: State Capitalism in the Dock," The Economist, 11/20/14. SOE refers to state-owned enterprises.

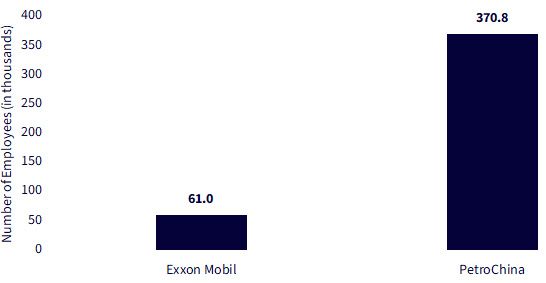

The principal–agent problem, the misalignment between owners' goals and managers' incentives, often manifests most clearly in state-owned enterprises (SOEs). PetroChina and Exxon Mobil offer a clean, real-world contrast between a state-owned and a shareholder-driven oil major.3

Figure 2 tells a striking story of scale and efficiency divergence.

State ownership often prioritizes social goals like employment stability and national development over operational efficiency, whereas Exxon Mobil's leaner structure reflects a private-sector focus on shareholder value and capital productivity.

Figure 2: PetroChina Employs Six Times More People than Exxon Mobil

Sources: Exxon Mobil Corporation, "2024 Annual Report" (Form 10-K), 4/7/25; PetroChina Company Limited, "2024 Annual Report," 4/25. Subject to change.

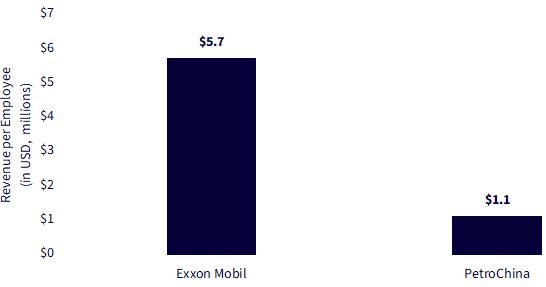

Productivity: A Study in Incentives

Figure 3 highlights revenue per employee, a strong proxy for productivity and managerial discipline.

Figure 3: Exxon Mobil Generated Five Times More Revenue per Worker than PetroChina

Sources: Exxon Mobil Corporation, "2024 Annual Report" (Form 10-K), 4/7/25;PetroChina Company Limited,"2024 Annual Report," 4/25. Subject to change.

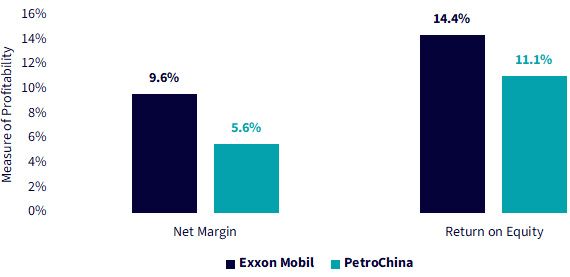

The profitability chart cements the pattern:

These differences may look modest, but they compound dramatically over time. Exxon's shareholder accountability drives capital discipline and cost control, while PetroChina's governance, anchored in state ownership, tends to blur accountability and dilute incentives to optimize capital efficiency.

Figure 4: Profitability Gaps between Market-Driven and State-Directed Models

Sources: Exxon Mobil Corporation, "2024 Annual Report" (Form 10-K), 4/7/25;PetroChina Company Limited,2024 Annual Report, 4/25. Subject to change.

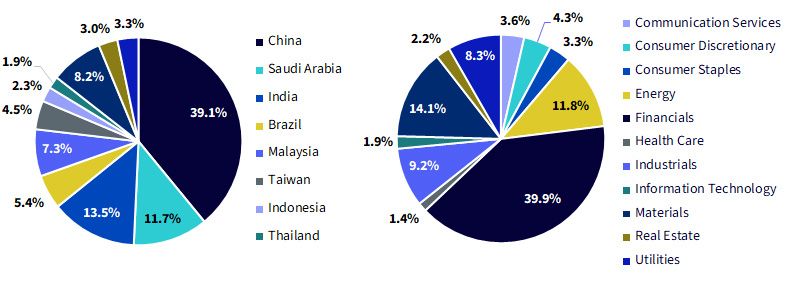

In 2025, state-owned enterprises remain concentrated in a few large markets and policy-sensitive sectors. As shown in figure 5, China, Saudi Arabia and India account for the bulk of state-linked equity capitalization, underscoring how national policy priorities shape corporate scale in emerging markets. On the right, the sectoral mix reveals a heavy tilt toward energy, financials and industrials, areas where governments view strategic control as essential. Together, these distributions highlight that the state's corporate footprint remains focused on power, capital and infrastructure, the commanding heights of the emerging-market economy.

Figure 5: Where the State Still Dominates: Geography and Sector Concentration of Emerging-Market SOEs (2025)

Sources: WisdomTree, FactSet, Standard & Poor's, with data as of 9/30/25, the WisdomTree Emerging Markets ex-State-Owned Enterprises Index screening date. Initial companies are those that pass minimum listing, market cap and liquidity requirements for inclusion. You cannot invest directly in an index. Weights subject to change.

The WisdomTree Emerging Markets ex-State-Owned Enterprises Fund (XSOE)4 was built around a simple but powerful premise: ownership matters. In many emerging markets, governments retain material stakes, often more than 20%, in large, listed companies, shaping priorities toward political or strategic goals such as employment, subsidies or national control rather than shareholder value.

The result is not simply a cleaner index; it's a structural refinement of EM beta: the same countries but with stronger governance, better capital efficiency and fewer policy distortions. Over time, this focus on incentive alignment aims to improve return on equity and margin sustainability, giving investors a purer expression of capitalism in markets where state involvement often dilutes it.

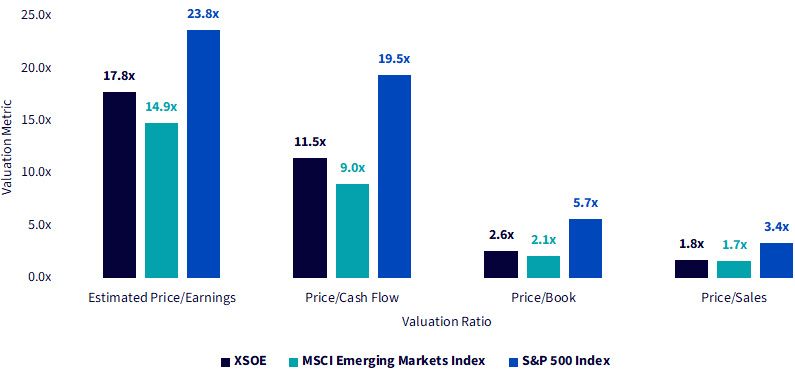

Repricing Governance: Why XSOE Trades with Stronger Fundamentals than EM

When investors think about equity benchmarks, the S&P 500 Index, with its exposure to U.S. equities, tends to define the high-quality, growth-oriented standard. Yet, what's striking in the data is how XSOE narrows the traditional gap between developed and emerging markets. In figure 6, we see XSOE trades at a discount to the S&P 500, 17.8x earnings vs. 23.8x, and 11.5x cash flow vs. 19.5x, but modestly richer than the broad MSCI Emerging Markets Index benchmark. That premium is rational: by excluding state-owned firms, XSOE skews toward more capital-efficient, shareholder-aligned businesses, the same qualities investors pay up for in developed markets.

Figure 6: How XSOE Sits between EM and the U.S. Equity Markets on Valuation

Sources: WisdomTree, FactSet, with data accessed through the Fund Compare tool within WisdomTree's PATH suite of tools. Data is as of 9/30/25. Subject to change.

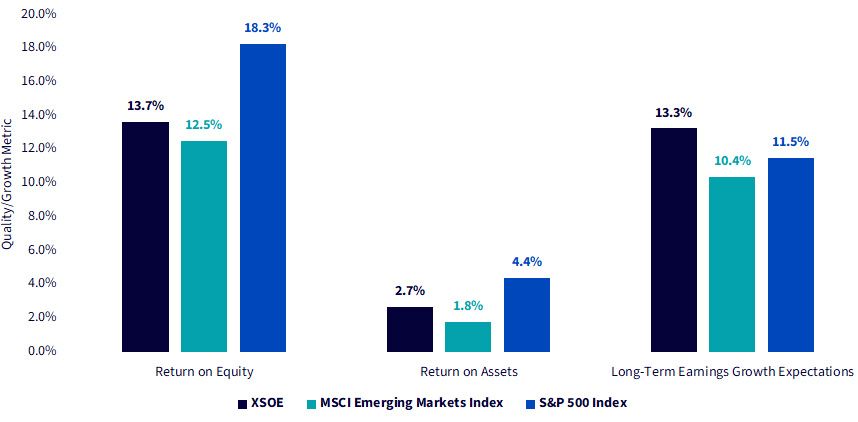

The payoff shows up in figure 7, where we see the quality and growth metrics. Return on equity sits at 13.7%, above the 12.5% of MSCI EM and closer to the S&P's 18.3%, while long-term earnings growth expectations reach 13.3%, well above both comparators. These companies are smaller on average but far more disciplined in capital use, generating higher profitability from each dollar of equity and reinvesting at stronger rates of return.

Figure 7: Governance as a Driver of Growth

Sources: WisdomTree, FactSet, with data accessed through the Fund Compare tool within WisdomTree's PATH suite of tools. Data is as of 9/30/25. Subject to change.

Conclusion: The Future of EM Investing Belongs to Entrepreneurs, Not Bureaucrats

In the end, the ex-state-owned approach is about more than just filtering a dataset; it's about redefining what it means to invest in emerging markets. Traditional EM exposure often ties investors to the ambitions of governments; XSOE ties them to the ambitions of entrepreneurs. It channels capital toward companies competing on innovation, efficiency and global relevance rather than policy mandate or political favor. This is ideally where growth compounds cleanly, where governance, profitability and market incentives align. In a world where emerging markets are no longer just catch-up stories but laboratories of technological and business model evolution, the ex-SOE framework separates the engines of progress from the machinery of policy.

1 In this article, we define state-owned enterprises as those companies with greater than 20% ownership by a state-entity.

2 Source: "Government-Controlled Firms: State Capitalism in the Dock," The Economist, 11/20/14.

3 Data points regarding Exxon Mobil and PetroChina are sourced from Exxon Mobil Corporation, "2024 Annual Report" (Form 10-K), 4/7/25;PetroChina Company Limited,"2024 Annual Report," 4/25. Subject to change.

4 XSOE is designed to track the total return performance, before fees and expenses, of the WisdomTree Emerging Markets ex-State-Owned Enterprises Index.

Important Risks Related to this Article

Emerging Markets ex-State-Owned Enterprises Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.