AIVL

U.S. AI Enhanced Value Fund

Published August 12, 2025

Global Head of Research

The U.S. economy, by nearly every recent signal, remains strikingly resilient. As the second-quarter earnings season opens, financial institutions like JPMorgan and Wells Fargo are reporting profits that outpaced expectations, propelled by healthy consumer activity and robust corporate lending.1 Labor markets remain stable, household spending is firm, and even in the face of persistent tariff uncertainty, business leaders are describing a climate where capital markets are "open for business" and confidence is returning.2 In a world where every macroeconomic wobble might have once sparked investor panic, the market today seems less rattled, perhaps too much so.

But beneath this outward strength lies a quieter caution. While consumers are spending, they're also trading down. Inventory managers remain conservative. CEOs from diverse sectors—retail, manufacturing, transport—echo the same refrain: uncertainty is rising around trade policy, Fed direction and geopolitical shocks.3 JPMorgan CEO Jamie Dimon warns of creeping market complacency, as equity investors increasingly overlook the structural risks that don't show up in quarterly earnings.4 The "soft landing" narrative dominates headlines, but it's clear that not all boats are rising equally. The winners in this environment are not always the highfliers of yesterday.

This nuanced backdrop provides fertile ground for the value equity style, an investment approach that thrives not on hype but on a disciplined attention to the fundamentals. Value investing is predicated on identifying companies whose intrinsic worth exceeds their current market price, a strategy that favors durability over directionality. In a climate where volatility is masked by index-level calm, and where dispersion across sectors is widening, value strategies offer an opportunity to lean into mispriced strength, especially among cyclical, financial and defensive sectors that benefit from normalized interest rates and resilient balance sheets.

Put differently, in an economy that's sturdy but still sorting itself out, and in markets where exuberance often overreaches, value investing is not just relevant, it may be essential. It provides a compass for navigating selective risk, avoiding inflated narratives and capturing equity exposure with a margin of safety. The question facing allocators isn't whether the market will rise; it's whether portfolios are anchored in businesses that can weather whatever comes next.

WisdomTree IsRedefining Value with Machine Intelligence

The WisdomTree U.S. AI Enhanced Value Fund (AIVL) takes a forward-looking, machine learning-driven approach that challenges conventional definitions of value. Built in partnership with Voya's Equity Machine Intelligence platform, AIVL does not rely on a fixed set of financial ratios. Instead, it leverages more than 250 features drawn from fundamental, market, sentiment and alternative datasets to dynamically interpret what constitutes value in different market regimes. The model adapts over time, learning which valuation signals are working and which are not, with the aim of generating more timely and context-sensitive portfolio positioning.

Seeing through the Model's Eyes

A key question facing any investor using a quantitatively driven strategy is this: What exactly is the model seeing that the market might be missing? AIVL doesn't rely on static valuation metrics or one-size-fits-all definitions of cheapness. Instead, it learns—adapting to shifting market regimes and updating its sense of what matters based on evolving investor behavior and factor effectiveness.

This means the portfolio isn't just a list of "low P/E" stocks; it's a living interpretation of what value means right now. At the company level, this approach yields a nuanced view of opportunity and risk. It highlights names where fundamental strength may be underappreciated or where traditional value signals are misleading.

What follows is a set of narratives, drawn directly from recent model-driven allocations, that illustrate how AIVL's process translates machine learning into real-world positioning. They come from the system noting specific details that it saw regarding the top three contributors and detractors to AIVL's performance relative to the Russell 1000 Value Index as of the second quarter of 2025.

The Contributors

UnitedHealth Group (UNH), a fixture in American health care, found itself under pressure not only from earnings misses but from regulatory scrutiny, yet what the model saw wasn't just noise. It flagged valuation metrics like the book-to-price ratio, weak free cash flow and underwhelming quality factors. Despite its size and relevance, UNH was tagged as a "stalwart in decline," suggesting that even dominant franchises can fall out of favor when fundamentals falter.

In contrast, Howmet Aerospace and Curtiss-Wright rose on very different kinds of overlooked strength. Both were industrials, both carried under-the-radar quality traits, like research and development (R&D) intensity and high buyback yield, and both executed well in structurally growing end-markets. They weren't speculative growth bets; they were engines of progress hiding in plain sight.

The Detractors

While these contributors show how value can quietly capture growth with discipline, the detractors tell another side of the coin: what happens when market sentiment, technical factors and macro overhangs overpower fundamentals. JPMorgan Chase, typically considered a bellwether of financial strength, was downgraded in the model due to weak momentum and quality signals. Even though the business remains large and profitable, the model doubted its near-term risk/reward, especially as tariffs threatened consumer sentiment. This was a case where even the giants aren't immune to macro exposure, and being big isn't enough.

Similarly, Pacific Gas & Electric Company (PG&E) was given a perfect quantitative score, fitting neatly into a classic defensive "bond proxy" framework, but the market moved away from its story despite this. Investors rotated into Utilities broadly, but PG&E's own dynamics didn't reward its high marks, a reminder that what scores well on paper doesn't always align with how capital flows in real time.

Then there's Fortive, a case study in how improvement doesn't always translate into conviction. The model rated it positively for its technicals and some signs of fundamental progress, particularly linked to streamlining and a planned spin-off aimed at focusing on higher-growth areas. But the market didn't buy it, at least not yet. This kind of lag between corporate narrative and investor belief is precisely where value investors often find opportunity. It's not about betting on change blindly but recognizing when real improvement isn't priced in.

Across all these names, what stands out is the importance of staying grounded in business fundamentals—R&D, capital allocation, governance—and resisting the temptation to chase market sentiment or avoid names simply because they've been out of favor. In short, the narrative structure of this quarter reveals exactly why value still matters: it helps us listen harder when the market shrugs.

While the stories behind individual holdings reveal how AIVL's machine learning engine interprets value in real time, the more important question for investors is: Does it work? Looking beyond model intuition and stock selection narratives, we now turn to the strategy's actual track record. By comparing AIVL's returns to both its benchmark—the Russell 1000 Value Index—and the broader S&P 500, we can assess whether its adaptive, data-driven approach translates into meaningful performance over time.

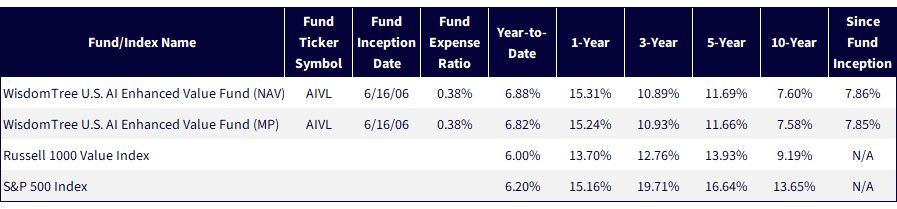

Figure 1: Standardized Performance

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/15/25, with returns as of 6/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. AIVL's objective and strategy changed effective 1/18/22. Prior to 1/18/22, AIVL performance reflects the investment objective of the Fund when it was the WisdomTree U.S. Dividend ex-Financials Fund (DTN) and tracked the performance, before fees and expenses, of the WisdomTree U.S. Dividend ex-Financials Index. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

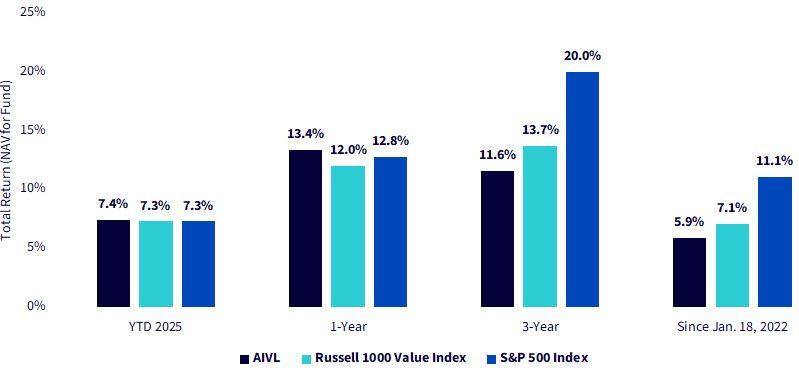

While value strategies have kept pace with the broader market in 2025—with AIVL, the Russell 1000 Value Index and the S&P 500 Index all delivering similar year-to-date returns—the longer-term picture reveals a persistent performance gap. Over the past three years and since January 18, 2022, the S&P 500 has significantly outpaced both value benchmarks. This chart tells a clear story: Value may be regaining traction in the near term, but the shadow of growth dominance still looms large across extended time horizons. The implication for investors is twofold: recognize the recent shift but also acknowledge the depth of the catch-up still required for value to reassert long-term leadership.

Figure 2: ValueHasRebounded in 2025, but a Longer-Term Gap to the S&P 500 Index Remains

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/15/25, with returns as of 7/14/25. NAV denotes total return performance at net asset value. AIVL's objective and strategy changed effective 1/18/22. Prior to 1/18/22, AIVL performance reflects the investment objective of the Fund when it was the WisdomTree U.S. Dividend ex-Financials Fund (DTN) and tracked the performance, before fees and expenses, of the WisdomTree U.S. Dividend ex-Financials Index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

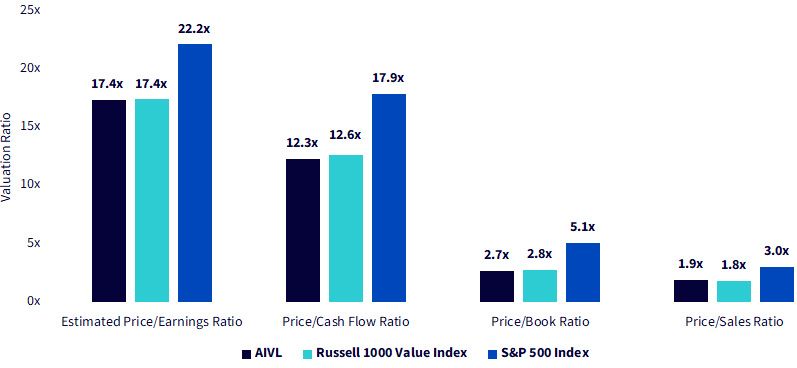

Every machine learning model needs an anchor—something to define the "center of gravity" against which patterns and anomalies are measured. For AIVL, that anchor is the Russell 1000 Value Index, a benchmark deeply rooted in conventional value definitions. What makes AIVL different, however, isn't that it swings wildly away from this foundation. In fact, as the chart shows, AIVL's valuation profile—its price-to-earnings, price-to-book, cash flow and sales ratios—sits right alongside its benchmark. There's no dramatic deviation or ultra-deep discount being chased. And that's the point: AIVL's model isn't looking for the cheapest stocks; it's looking for underpriced quality, mispriced improvement and contextual value signals that matter now, not just in theory.

Where you do see a real gap is against the S&P 500 Index, where valuations are meaningfully higher across every metric. This is where AIVL's positioning becomes even more compelling: It's not taking excessive risk to differentiate from its benchmark, but it's also delivering access to a part of the market that trades at a tangible discount to the broader equity universe. In other words, AIVL isn't just mimicking traditional value—it's quietly navigating a middle path: strategically aligned with value benchmarks but driven by adaptive intelligence that knows when, and how, to depart from convention.

Figure 3: Valuation Comparison: AIVL vs. Value and Broad Market Benchmarks

Sources: WisdomTree, FactSet, with data as of 6/30/25. Subject to change.

Small Deviations, Big Signals: What Sector Tilts Reveal about AIVL

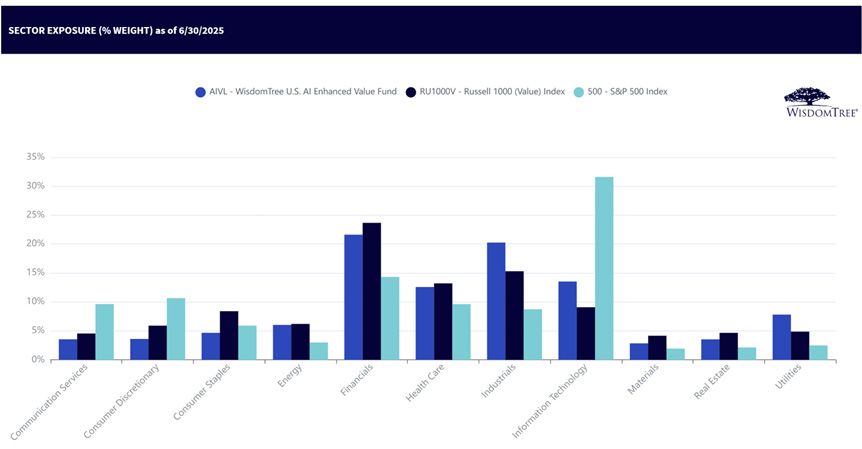

At first glance, AIVL's sector exposures appear closely aligned with its benchmark, the Russell 1000 Value Index—a natural expectation for a strategy grounded in the value style. But the real insight lies not in broad similarity but in subtle divergences. These small differences are where the machine learning model's preferences come to life. For example, AIVL leans more heavily into Industrials and Information Technology, reinforcing the model's tilt toward cash-generative, capital-efficient businesses that often screen well on dynamic quality metrics relative to the Russell 1000 Value Index. Meanwhile, a slightly lighter stance in real estate, while a slightly heavier stance in Utilities (against the Russell 1000 Value Index), may reflect a more selective, nuanced view on these rate-sensitive sectors.

What's equally telling is how both AIVL and the Russell 1000 Value Index benchmark differ from the S&P 500 Index, particularly in Information Technology, Communication Services and Consumer Discretionary, areas where traditional valuation signals often get overwhelmed by growth narratives. AIVL doesn't chase those exposures, but when it does own names in those sectors, it's because the data is flashing something specific: a temporary mispricing, a turnaround in fundamentals or a dislocation that others might miss. In this way, even modest sector differences aren't noise; they're evidence of the model's selective conviction, revealing where the strategy believes today's value is misperceived.

Figure 4: Staying True to Value—with a Machine-Learned Edge

Sources: WisdomTree, FactSet, with data as of 6/30/25. Subject to change.

In an environment where traditional signals are distorted by macro noise, sentiment swings and regime shifts, investors need more than static valuation screens; they need context-aware insight. AIVL offers a differentiated path forward: one that honors the core principles of value investing while evolving their implementation through machine learning. By dynamically reinterpreting which valuation signals matter, when and why, the strategy avoids stale definitions and embraces the complexity of modern markets. Whether through its positioning in overlooked Industrials, its cautious view on mega-cap complacency or its disciplined exposure to valuation without chasing deep discounts, AIVL is a timely expression of what value can look like when it learns.

1 Source: A. Saeedy, "JPMorgan earnings show economy and Wall Street are still chugging along," The Wall Street Journal, 7/15/25.

2 Source: The Transcript, "Open windows," Substack, 7/14/25.

3 Source: The Transcript, 7/14/25.

4 Source: The Transcript, 7/14/25.

For current holdings of AIVL, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on a quantitative model, and the model may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. AI Enhanced Value Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.