DXJ

Japan Hedged Equity Fund

Published December 2, 2025

Global Head of Research

Japanese equities have quietly staged one of the most interesting leadership shifts of 2025—and we find that most U.S. investors aren't even looking in that direction. For years, the conversation around Japan has been dominated by macro worries, currency noise and a sense that the market "just can't break out." Yet the numbers now tell a completely different story.

Throughout 2025, we have written numerous times about Warren Buffett's favorable views on five particular Japanese equity holdings in Berkshire Hathaway's portfolio.1 In early November 2025, he filed for another yen bond issuance, indicating a desire to increase his currency hedge or put more capital to work buying more Japanese stocks.2

We noticed recently that the WisdomTree Japan Hedged Equity Fund (DXJ)3 is beginning to separate itself from the iShares MSCI Japan ETF (EWJ).4 With the yen weakening and fundamentals finally showing momentum, the question isn't "Why own Japan?" anymore. It's "Why not own the version of Japan that's showing the performance acceleration?"

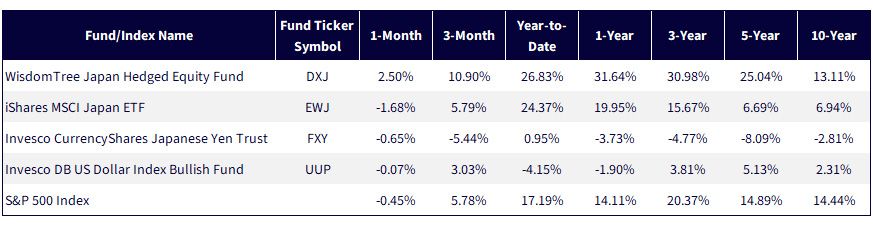

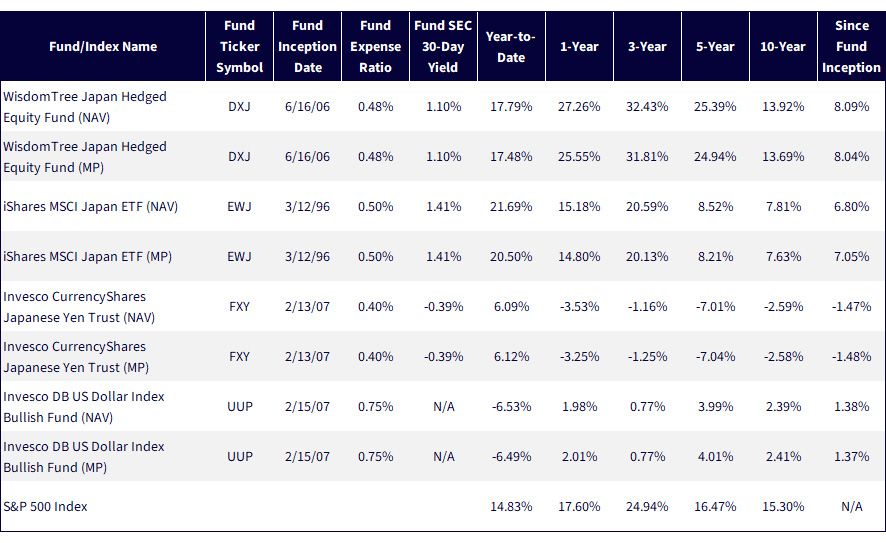

Looking at figures 1a and 1b:

Figure 1a: DXJ's Performance Has Been Accelerating

Figure 1b: Standardized Returns as of September 30, 2025

Sources: Morningstar, FactSet and WisdomTree; specifically, data is from the PATH Fund Comparison Tool, accessed as of 12/2/25, but showing returns for the period ended 12/1/25 for figure 1a and 9/30/25 for figure 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the relevant ticker: DXJ, EWJ, FXY, UUP.

Conclusion: It Could Be a Great Time to Look at Japan

Japanese equities remain a psychological anomaly in global investing. The same advisors who eagerly buy every dip in U.S. large caps suddenly turn cautious, contemplative, even philosophical when Japan enters the conversation. In our experience, investors approach Japan as though it requires a dissertation to justify. The irony is that the case for Japan today is simpler than ever: corporate governance improving, currency weakness acting as a tailwind—not a risk—and performance numbers that stand shoulder-to-shoulder with America's market darlings. In a market where it seems like every other headline about U.S. equities discusses some form of AI or valuation risk, Japanese equities are showing performance and offering a way to navigate around these issues.

Sources: WisdomTree, iShares, Invesco, as of 11/17/25.

1 Source: W. E. Buffett, "Letter to shareholders" [annual letter], Berkshire Hathaway Inc., 2/22/25.

2 Source: "Berkshire Hathaway plans yen bond amid global debt binge," Bloomberg News, 11/6/25.

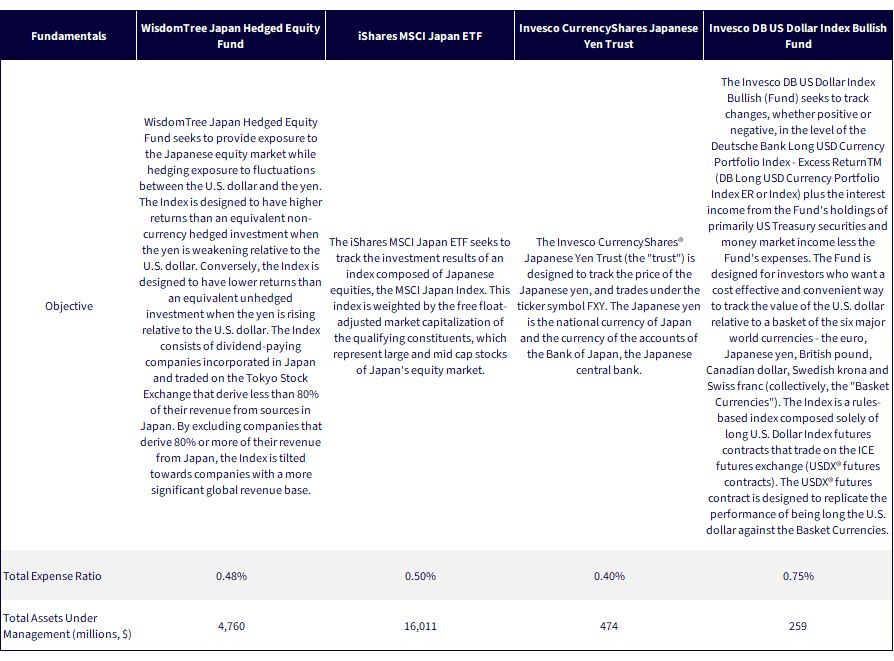

3 DXJ is designed to track the total return performance, before fees and expenses, of the WisdomTree Japan Hedged Equity Index. This Index neutralizes any performance of the yen vs. U.S. dollar exchange rate, and it focuses the equity exposure on dividend-paying, export-oriented stocks of Japan. Constituents are weighted on the basis of cash dividends paid.

4 EWJ is designed to track the total return performance, before fees and expenses, of the MSCI Japan Index. This is one of the most widely followed equity performance benchmarks for Japanese equities, with constituents representing large- and mid-cap stocks of Japan, weighted by free float-adjusted market capitalization.

5 FXY represents an ETF, the most widely followed investment vehicle in the U.S., which seeks to track the performance of the Japanese yen versus the U.S. dollar.

6 UUP represents an ETF, the most widely followed investment vehicle in the U.S., which seeks to track the performance of the U.S. dollar against a basket of other currencies.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

DXJ: There are risks associated with investing, including possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

EWJ: There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The Fund's return may not match the return of the Underlying Index. The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the Fund. Investments focused in a particular sector, such as technology, are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

FXY: There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The Fund's return may not match the return of the Underlying Index. The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the Fund. Investments focused in a particular sector, such as technology, are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

UUP: There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The Fund's return may not match the return of the Underlying Index. The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the Fund. Investments focused in a particular sector, such as technology, are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

Japan Hedged Equity Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.