Adding, Not Replacing: Broad Commodities in the Age of Efficient Capital

Published April 22, 2026

Global Head of Research

Key Takeaways

- As of April 2026, portfolios using WisdomTree’s Efficient Capital approach—combining the WisdomTree U.S. Efficient Core Fund (NTSX) with the WisdomTree Enhanced Commodity Strategy Fund (GCC)—have outperformed traditional 60/40 and reallocated commodity portfolios by preserving core exposures while layering in a 20% commodities sleeve.

- Despite persistent inflation uncertainty and rising stock and bond correlations, broad commodities offer a structurally low-correlated, inflation-sensitive return stream, making GCC a compelling additive diversifier rather than a funded trade-off.

- By separating capital from exposure, investors can maintain a full 60/40 equity and bond profile using NTSX while enhancing return potential through commodities and futures-based carry strategies embedded in GCC.

For decades, portfolio construction has revolved around a simple constraint: you have 100 percent of a total allocation, and every new addition requires taking a portion from somewhere else. That constraint has shaped everything, as seen in the dominance of 60/40 portfolios and the difficulty of incorporating alternatives without sacrificing expected return.

But the academic foundation for a different approach has existed for nearly 30 years.

In 1996, Cliff Asness published “Why Not 100% Equities?”,1 a paper that started with a deceptively simple observation: equities had historically outperformed bonds. But that didn’t mean 100% equities were optimal. In fact, he showed that a diversified portfolio of stocks and bonds could deliver more expected return per unit of risk than equities alone.

The key insight wasn’t just diversification, but how diversification interacts with leverage.

Looking at long-term data in this work (1926–1993), equities returned about 10.3% annually with ~20% volatility. A 60/40 portfolio delivered lower returns (~8.9%) but with dramatically lower risk (~12.9%). This is where it gets interesting: if you leveraged the 60/40 portfolio to the same risk level as equities, returns increased to ~11.1%, higher than for stocks alone.

In other words, the optimal portfolio wasn’t “all equities.” It was a diversified portfolio, scaled appropriately.

This led to a deeper principle from modern portfolio theory: the decision of what to own (the optimal mix of assets) is separate from the decision of how much risk to take.

Yet most portfolios still conflate the two.

Introducing WisdomTree’s Efficient Capital Framework

WisdomTree’s Efficient Capital framework was not introduced as a theoretical concept; it was launched into the market in 2018 with the debut of the WisdomTree U.S. Efficient Core Fund (NTSX).

NTSX represented the practical implementation of an idea that had largely lived in institutional portfolios and academic journals for decades. By combining a 90% allocation to U.S. equities with a 60% exposure to U.S. Treasury futures, the strategy delivered approximately 150% notional exposure, effectively recreating a traditional 60/40 portfolio while doing so more efficiently by using less capital for the same overall notional exposure.

The innovation wasn’t leverage for its own sake. It was about solving a structural inefficiency in portfolio construction, thereby freeing up capital without giving up core exposures.

In doing so, NTSX marked a shift from thinking in terms of capital allocation to thinking in terms of exposure construction.

Which leads to a fundamentally different question.

Not: What do we remove to add something new?

But: What can we add, once we separate capital from exposure? This is the first of three articles where we will introduce this efficient capital concept and then explore a particular option that could be added with the extra space.

Filling the Gap: Why Broad Commodities Belong in an Efficient Portfolio

A substantial body of academic and practitioner research has long established commodities as a distinct asset class, characterized by low correlations to traditional financial assets. For example, Erb and Harvey (2006) show that commodity futures historically exhibited correlations near zero with equities and bonds, while Gorton and Rouwenhorst (2006) find that diversified commodity futures delivered equity-like returns with bond-like volatility and similarly low correlation to stocks and fixed income. More recent data reinforce this point. Over long horizons, correlations between broad commodity indices and equities have typically ranged between ~0.2–0.3, while correlations with bonds have often been close to zero or even slightly negative.2

This independence is structural, not incidental. Unlike equities and bonds, which are driven by discounted cash flows and interest rates, commodity returns are tied to real-world economic forces, for example, supply and demand imbalances, geopolitical disruptions, weather patterns and industrial production cycles. As a result, commodities often respond to different macroeconomic regimes, particularly those tied to inflation or resource scarcity.

From a portfolio construction perspective, this creates the potential for a powerful diversification benefit. When traditional assets become more correlated, such as during inflation shocks or periods of macro stress—commodities have historically provided an alternative return stream driven by the real economy rather than financial conditions.

That distinction becomes especially important in inflationary environments. More recent empirical work reinforces this dynamic. Over periods of rising inflation, broad commodity indices have often shown meaningfully positive returns, while stock and bond returns have been pressured by higher discount rates and declining real valuations.3

The mechanism is intuitive: commodities are the inputs into the inflation process. Energy, metals and agricultural goods sit upstream in the global economy, meaning that increases in their prices often precede and drive broader inflation measures.

From a portfolio perspective, this creates a rare and valuable property. In environments where both stocks and bonds struggle, such as stagflationary or inflation shock regimes, commodities have historically provided a direct and economically grounded hedge, offering a return stream tied to rising prices rather than eroded by them.

But the story does not end with diversification.

Commodity returns are also shaped by futures market dynamics, particularly carry—the return associated with the structure of futures curves. Traditional commodity indices often ignore this dimension, focusing primarily on front-month exposure. Yet research and index evidence suggest that strategies optimizing across the curve to capture carry have historically enhanced returns while reducing volatility.4

This is where the WisdomTree Enhanced Commodity Strategy Fund (GCC) comes in.

GCC is designed to provide diversified exposure across commodity sectors, including energy, metals and agriculture, while actively selecting futures maturities to maximize expected carry. Rather than relying on static, production-weighted approaches,5 it incorporates both strategic allocation and tactical insights, seeking to improve the efficiency of commodity exposure.

In effect, if Efficient Capital creates space, broad commodities—implemented thoughtfully—offer a way to fill it with a return stream tied not to financial assets, but to the real economy itself.

From Trade-Off to Addition: A New Way to Add Commodities

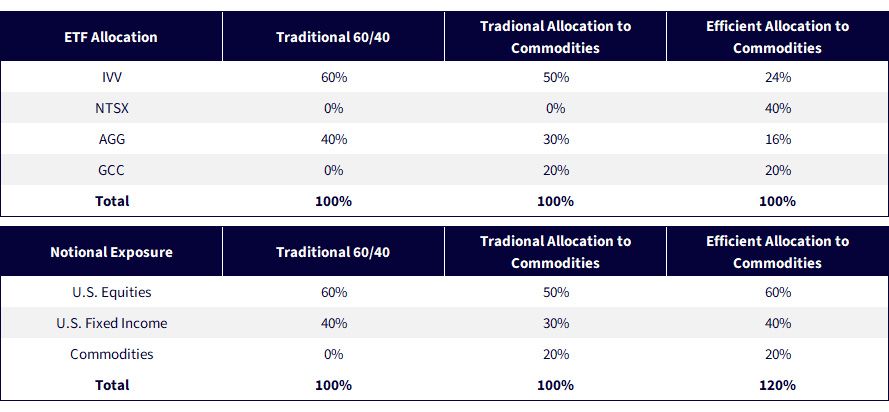

To make this more tangible, we can compare three ways of incorporating broad commodities into a portfolio, but first we have to define our different ETF building blocks.

- IVV: The iShares Core S&P 500 ETF, which is designed to track, before fees and expenses, the total return performance of the S&P 500 Index, the most widely followed and referenced benchmark for U.S. equity market performance. This strategy is among the largest by assets under management tracking this benchmark.

- AGG: The iShares Core U.S. Aggregate Bond ETF, which is designed to track, before fees and expenses, the total return performance of the Bloomberg U.S. Aggregate Bond Index. This is among the most widely followed measures of the performance of U.S. investment-grade fixed income.

- NTSX: As described previously, this strategy incorporates 90% notional exposure to U.S. equities and 60% notional exposure to U.S. fixed income futures, for a total notional exposure of 150%. It is a portfolio tool designed to help investors free up allocation space to add in other asset classes that may have different portfolio characteristics.

- GCC: As described previously, this strategy focuses on providing broad exposure to a basket of commodity futures contracts, with some exposure to Bitcoin.

In Figure 1, the starting point is the ‘traditional 60/40’, 60% equities (IVV) and 40% fixed income (AGG). This serves as a familiar baseline, with 100% total notional exposure split between stocks and bonds.

From there is the ‘traditional allocation to commodities’ approach, which introduces commodities by reallocating capital: 50% equities, 30% bonds and 20% broad commodities (GCC). This maintains 100% total exposure but requires reducing core equity and bond allocations to make room for the diversifier, in this case, broad commodities.

The ‘Efficient Allocation to Commodities’ takes a different path.

Overall, the idea is to keep the 60% U.S. equities and 40% U.S. fixed income parts of the allocation intact, but to then add commodities over the top. Figure 1 shows how placing:

Leads to notional exposures of 60% U.S. equities, 40% U.S. fixed income and 20% broad commodities.

This is the key distinction. The investor keeps the original allocation and adds a potential diversifier over the top.

Figure 1: Adding Commodities Without Giving Up Core Exposure

Source: WisdomTree. The rationale for this allocation between the different ETFs is based on the concept of keeping to 60% exposure to U.S. equities and 40% exposure to U.S. fixed income.

From Theory to Results: Efficient Capital in Action

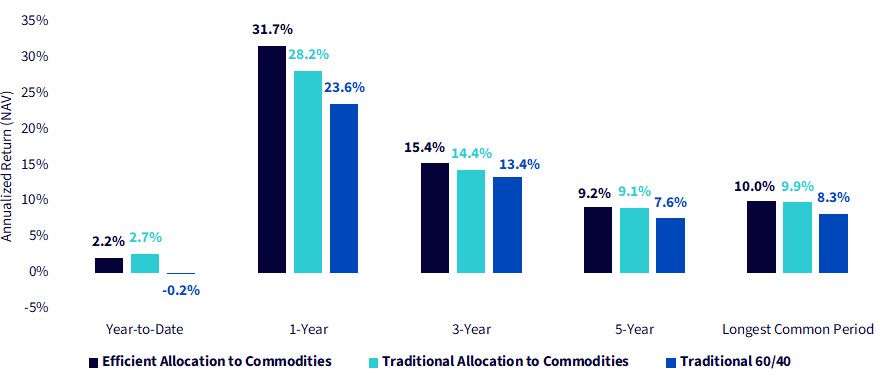

With the allocations established, the next question is straightforward: has this more efficient approach to incorporating commodities improved outcomes?

Looking at realized performance, the Efficient Allocation to Commodities has consistently outperformed both the Traditional Allocation to Commodities and the Traditional 60/40. In Figure 2a, we see:

- Both the Efficient and Traditional allocations to commodities, meaning commodities were added, outperformed the Traditional 60/40 over each period shown.

- In periods of 1-year and longer, the Efficient Allocation to Commodities outperformed the Traditional Allocation to commodities, although in some periods it was quite close.

Importantly, this outperformance reflects more than just commodity exposure. By maintaining core equity and bond allocations while layering in commodities, the Efficient Core approach allows multiple return streams to contribute simultaneously.

The takeaway is consistent: diversification works best when it is additive, not subtractive.

Figure 2a: Adding Commodities Without Sacrificing Returns: The Evidence

Figure 2b: Standardized Returns

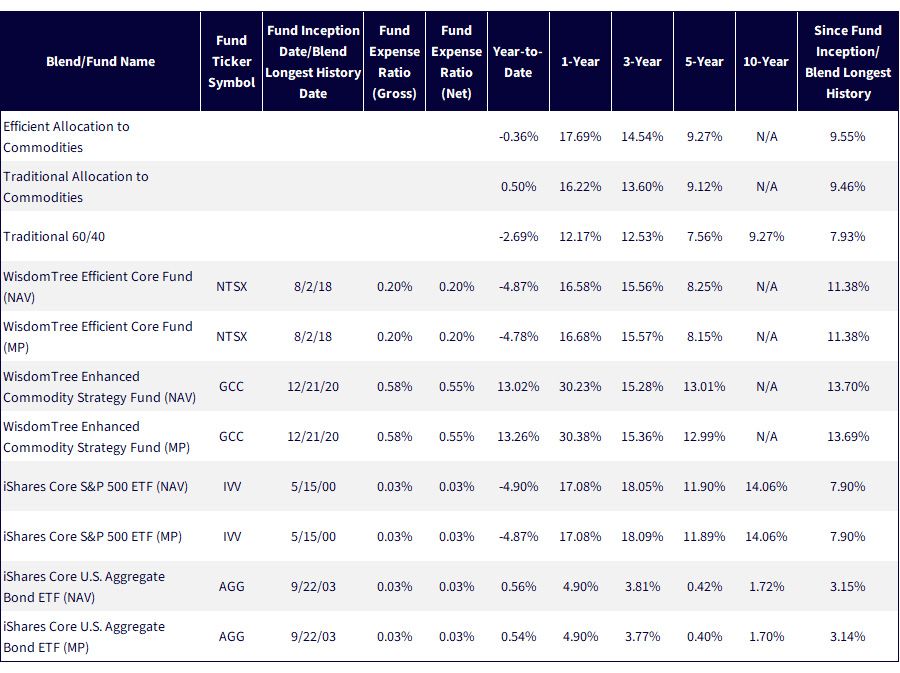

Sources: Morningstar, FactSet and WisdomTree, specifically, data are from the PATH Fund Comparison Tool, accessed as of April 10, 2026, but showing returns for the period ended April 8, 2026 for Figure 2a and March 31, 2026 for 2b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: NTSX, GCC, IVV, AGG.

Conclusion: What If a Broad Commodities Allocation Didn’t Require a Trade-Off?

Broad commodities have long been recognized for their diversification benefits, yet in practice, they are often underutilized. The reason is familiar: adding commodities has traditionally required reducing exposure to equities or fixed income, creating the same trade-off that has limited allocations to gold and other alternatives.

Efficient Capital changes that equation.

By separating exposure from capital, investors can incorporate commodities without sacrificing core portfolio building blocks. Instead of asking whether commodities deserve a place, the question becomes how to integrate them more effectively. Strategies like GCC, when paired with an efficient core, allow investors to access a diversified set of real-asset exposures, including energy, metals, and agriculture, alongside traditional assets.

In a world shaped by inflation uncertainty, geopolitical fragmentation and shifting supply chains, that matters.

The goal is no longer just diversification for its own sake—it is building portfolios that can evolve with the real economy.

That is where commodities, thoughtfully implemented, can play a critical role.

Figure 3: Additional Information

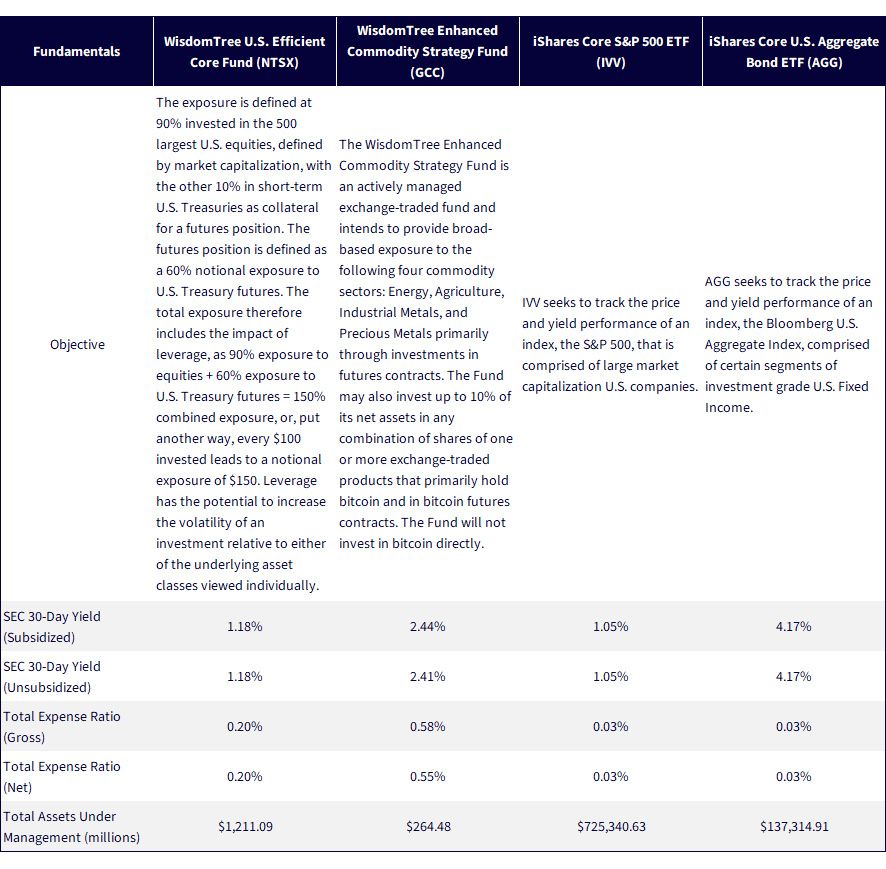

Sources: Respect fund webpages for each respective ETF sponsor. Assets under management data is as of April 1, 2026. Subject to change.

- Source: Asness, C. S. (1996). Why not 100% equities? The Journal of Portfolio Management, 22(2), 29–40.

- Sources: Erb, C. B., & Harvey, C. R. (2006). The strategic and tactical value of commodity futures. Financial Analysts Journal, 62(2), 69–97; Gorton, G., & Rouwenhorst, K. G. (2006). Facts and fantasies about commodity futures. Financial Analysts Journal, 62(2), 47–68.

- Sources: Su, Y., & Zeng, Y. (2022). Which asset classes provide inflation hedges? National Bureau of Economic Research; Boons, M., Duarte, F., de Roon, F., & Szymanowska, M. (2025). Time-varying inflation risk and commodity returns. Review of Financial Studies, 39(3), 702–757.

- Sources: Fuertes, A. M., Miffre, J., & Rallis, G. (2010). Tactical allocation in commodity futures markets: Combining momentum and term structure signals. Journal of Banking & Finance, 34(10), 2530–2548; Basu, D., & Miffre, J. (2013). Capturing the risk premium of commodity futures: The role of hedging pressure. Journal of Banking & Finance, 37(7), 2652–2664; Till, H. (2015). What is the “carry” in commodity futures returns? Journal of Investing, 24(1), 105–112.

- Source: Bloomberg Index Services Limited. (2025). Bloomberg Commodity Index methodology. Bloomberg.

Source: Asness, C. S. (1996). Why not 100% equities? The Journal of Portfolio Management, 22(2), 29–40.

Sources: Erb, C. B., & Harvey, C. R. (2006). The strategic and tactical value of commodity futures. Financial Analysts Journal, 62(2), 69–97; Gorton, G., & Rouwenhorst, K. G. (2006). Facts and fantasies about commodity futures. Financial Analysts Journal, 62(2), 47–68.

Sources: Su, Y., & Zeng, Y. (2022). Which asset classes provide inflation hedges? National Bureau of Economic Research; Boons, M., Duarte, F., de Roon, F., & Szymanowska, M. (2025). Time-varying inflation risk and commodity returns. Review of Financial Studies, 39(3), 702–757.

Sources: Fuertes, A. M., Miffre, J., & Rallis, G. (2010). Tactical allocation in commodity futures markets: Combining momentum and term structure signals. Journal of Banking & Finance, 34(10), 2530–2548; Basu, D., & Miffre, J. (2013). Capturing the risk premium of commodity futures: The role of hedging pressure. Journal of Banking & Finance, 37(7), 2652–2664; Till, H. (2015). What is the “carry” in commodity futures returns? Journal of Investing, 24(1), 105–112.

Source: Bloomberg Index Services Limited. (2025). Bloomberg Commodity Index methodology. Bloomberg.

Important Risks Related to this Article

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

There are risks associated with investing, including possible loss of principal.

GCC: An investment in this Fund is speculative, involves a substantial degree of risk, and should not constitute an investor's entire portfolio. One of the risks associated with the Fund is the complexity of the different factors which contribute to the Fund's performance. These factors include use of commodity futures contracts. In addition, bitcoin exchange-traded products (ETPs) and bitcoin futures are relatively new and the markets may be less developed. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. As a result, the markets for bitcoin futures and bitcoin ETPs may be less developed, and at times, potentially less liquid and more volatile, than more established commodity futures and ETP markets. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. In addition, derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. The value of the shares of the Fund relate directly to the value of the futures contracts and other assets held by the Fund and any fluctuation in the value of these assets could adversely affect an investment in the Fund's shares. Because of the frequency with which the Fund expects to roll futures contracts, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”) and the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. The Fund will not invest in bitcoin directly.

NTSX: While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended. The Fund invests in derivatives to gain exposure to U.S. Treasuries. The return on a derivative instrument may not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage and derivatives can be volatile and may be less liquid than other securities. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money. Interest rate risk is the risk that fixed income securities, and financial instruments related to fixed income securities, will decline in value because of an increase in interest rates and changes to other factors, such as perception of an issuer’s creditworthiness.

Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For additional fund disclosures, please click the respective ticker: IVV, AGG.

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.