DEW

Global High Dividend Fund

Published October 31, 2025

Associate, Investment Strategy

We conducted the annual rebalance for the WisdomTree Global Dividend Index (WTGDIV) earlier in October.

During this year's reconstitution, there were 6,377 selected companies eligible for inclusion from the U.S. and nearly 40 other developed and emerging market countries.

Constituents are weighted based on their contribution to the global Dividend Stream®, which represents the aggregate pool of dividends paid among eligible companies within eligible countries. Consistent with the 2024 rebalance, the largest dividend-payer during this year's screening was still Microsoft, which pays about $23 billion in annual dividends as of September 30 and received more than 1.4% weight in the Index.

Some of the most notable changes at the constituent level this year include:

Assessing theGlobal Dividend Stream®in 2025

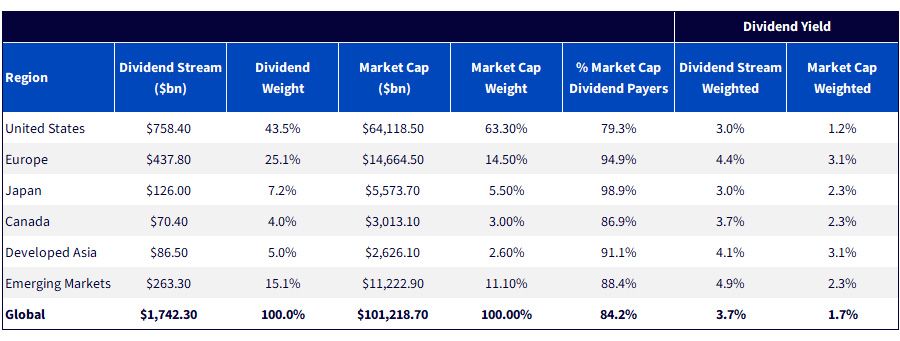

The global equity market currently pays about $1.7 trillion worth of dividends, up from roughly $1.6 trillion this time last year.

About 57% of all dividends are paid outside the U.S., which is about 20% greater than the total non-U.S. weight in market cap-weighted indexes. Conversely, the 43% dividend contribution provided by U.S. companies is much less than their 63% share of the global market capitalization. That inherently means that non-U.S. countries are over-weighted in dividend-focused indexes while U.S. exposure is meaningfully reduced. European countries, for example, contribute about one-quarter of all global dividend payments, which is 10% greater than their proportion of global market cap.

Figure 1: Global Dividend Stream® Composition

Sources: WisdomTree, MSCI, as of 9/30/25. Universe is MSCI ACWI IMI. Israel included in Europe. Developed Asia includes Singapore, Australia, Hong Kong and New Zealand. U.S. dividends are indicated. International dividends are trailing. Dividend Stream and Market Cap totals are adjusted for investability factors. You cannot invest directly in an index.

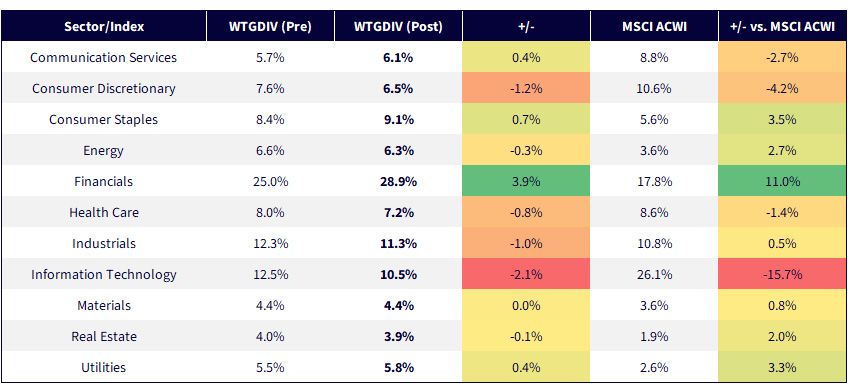

The Index's sector exposures did not vary much between its pre- and post-rebalance iterations. Amid a strong rally in global Financials in 2025, the sector was newly over-weighted by nearly 4% versus its pre-rebalance exposure, while Information Technology received the largest reduction and was under-weighted by 2.1%. The other 10 GICS® sectors experienced changes of around 1% or less.

Source: WisdomTree, as of 10/16/25. MSCI ACWI weights as of 9/30/25. You cannot invest directly in an index.

Versus the MSCI AC World Index (ACWI), however, the sector differences are more pronounced due to our dividend focus. The over-weight to Financials now exceeds 11%, while Information Technology is less than half that of global, market cap-weighted indexes.

The dividend-weighted methodology naturally introduces a tilt to traditionally cyclical and dividend-heavy sectors, which results in a 3.5% over-weight to Consumer Staples and a 3.3% over-weight to Utilities. Correspondingly, traditional Growth sectors like Communication Services and Consumer Discretionary remain under-weight by about 2.7% and 4.2% respectively.

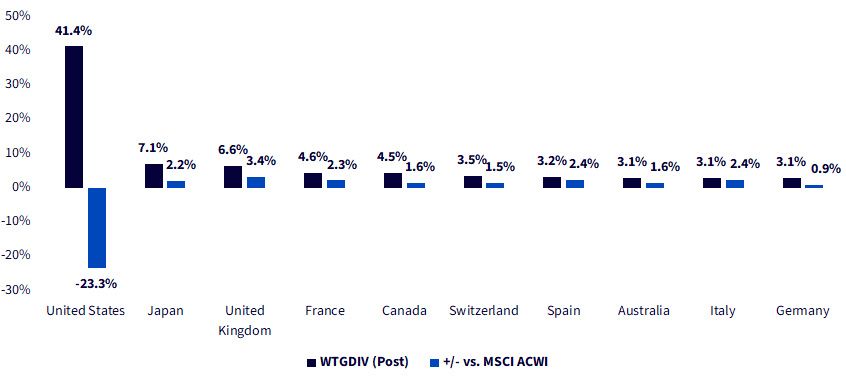

From a country standpoint, there was virtually no change between the pre- and post-rebalance geographic exposures. The only country with a change of more than 1% was Japan, which was under-weighted by about 1.7%.

Relative to the MSCI ACWI, however, we see some consistent themes when differentiating between dividend- and market cap-weighted global indexes. Naturally, the WisdomTree Global Dividend Index is heavily under-weight the United States versus the MSCI ACWI since many of the largest companies that comprise the latter do not pay a large enough dividend to merit comparable exposure in a dividend-weighted index. As a result, the disconnect between dividend-weighted allocations and exposures dictated by market capitalization remains apparent.

The magnitude of the U.S. under-weight results in corresponding over-weights to almost all other countries. Japan and many of the other European countries shown below are good examples, since the non-U.S. region has a greater preference for dividend payments. Nearly 100% of the Japanese and European equity market cap pays a dividend, highlighting its popularity as a method of delivering value to shareholders.

Sources: WisdomTree, MSCI, as of 10/16/25. MSCI ACWI weights as of 9/30/25. You cannot invest directly in an index.

Changes to the WisdomTree Global High Dividend Index (WTGDHY)

One of the subsets of WTGDIV is the WisdomTree Global High Dividend Index, which selects the top 30% of companies by dividend yield from the global dividend-paying equity universe. It applies an adjustment factor so that the weights of each region (i.e., the U.S., developed and emerging markets) in our stock basket are equal to the regional weights by float-adjusted market capitalization of the entire global equity market, rather than exclusively dividend-payers.

As the name suggests, the Index targets the segment of the global equity market that has the highest dividend yield after eliminating what we deem to be the riskiest companies via CRS parameters. A higher-yielding equity basket could be advantageous in today's market environment, where global rates may continue to fall, as the dividend yield potential may help supplement diminished cash flows from traditional income-producing investments. Meanwhile, investors maintain potential equity upside if equity markets continue higher, as well.

Post-rebalance, the Index offers a dividend yield of more than 4.4%, while the yield on the MSCI ACWI is about 1.6%, as of September 30. The potential 280-bp yield advantage may be an attractive consideration for income-oriented investors.

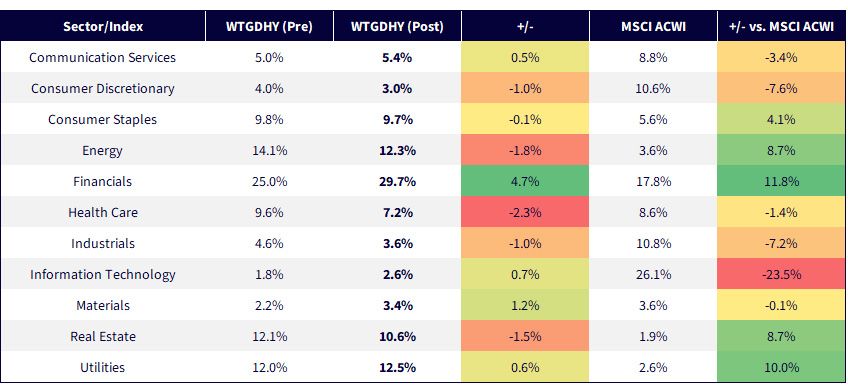

Since it's essentially "region" neutral, the sector composition is a greater consideration as the rebalance tends to have more pronounced effects.

Relative to its pre-rebalance iteration, the reconstituted Index features a near-5% over-weight to Financials, which follows the sector's rally in 2025 and matches the trend observed in the broader Global Dividend Index (WTGDIV). Most of that pickup was funded by under-weights to Health Care, Energy and Real Estate. The remaining changes were around 1% or less in either direction.

Unsurprisingly, we see greater tilts versus the MSCI ACWI. Information Technology is once again a significant, double-digit under-weight and comparatively nonexistent versus MSCI ACWI. Greater Financials and Energy exposure offsets some of that gap, while other Value-oriented sectors, like Real Estate and Utilities, steer the Index further away from Growth heavyweights like Communication Services and Consumer Discretionary.

Source: WisdomTree, as of 10/16/25. MSCI ACWI Index weights as of 9/30/25. You cannot invest directly in an index.

For investors considering a high-dividend yield global equity solution, the WisdomTree Global High Dividend Fund (DEW) seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Global High Dividend Index.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

Global High Dividend Fund

Associate, Investment Strategy

Brian Manby joined WisdomTree in October 2018 as an Investment Strategy Analyst. He is responsible for assisting in the creation and analysis of WisdomTree’s model portfolios, as well as helping support the firm’s research efforts. Prior to joining WisdomTree, he worked for FactSet Research Systems, Inc. as a Senior Consultant, where he assisted clients in the creation, maintenance and support of FactSet products in the investment management workflow. Brian received a B.A. as a dual major in Economics and Political Science from the University of Connecticut in 2016. He is holder of the Chartered Financial Analyst designation.